How High Could Energy Prices Go? The 2026 Strait of Hormuz Crisis and the Anatomy of a Global Energy Emergency

Executive Summary

Iran's Hormuz Gambit Has Exposed the Deepest Vulnerability in the Global Energy System

The closure of the Strait of Hormuz on February 28, 2026, following joint United States-Israeli strikes on Iran, has precipitated what the International Energy Agency (IEA) has called the greatest global energy security threat in recorded history — more consequential than the twin oil shocks of the 1970s combined.

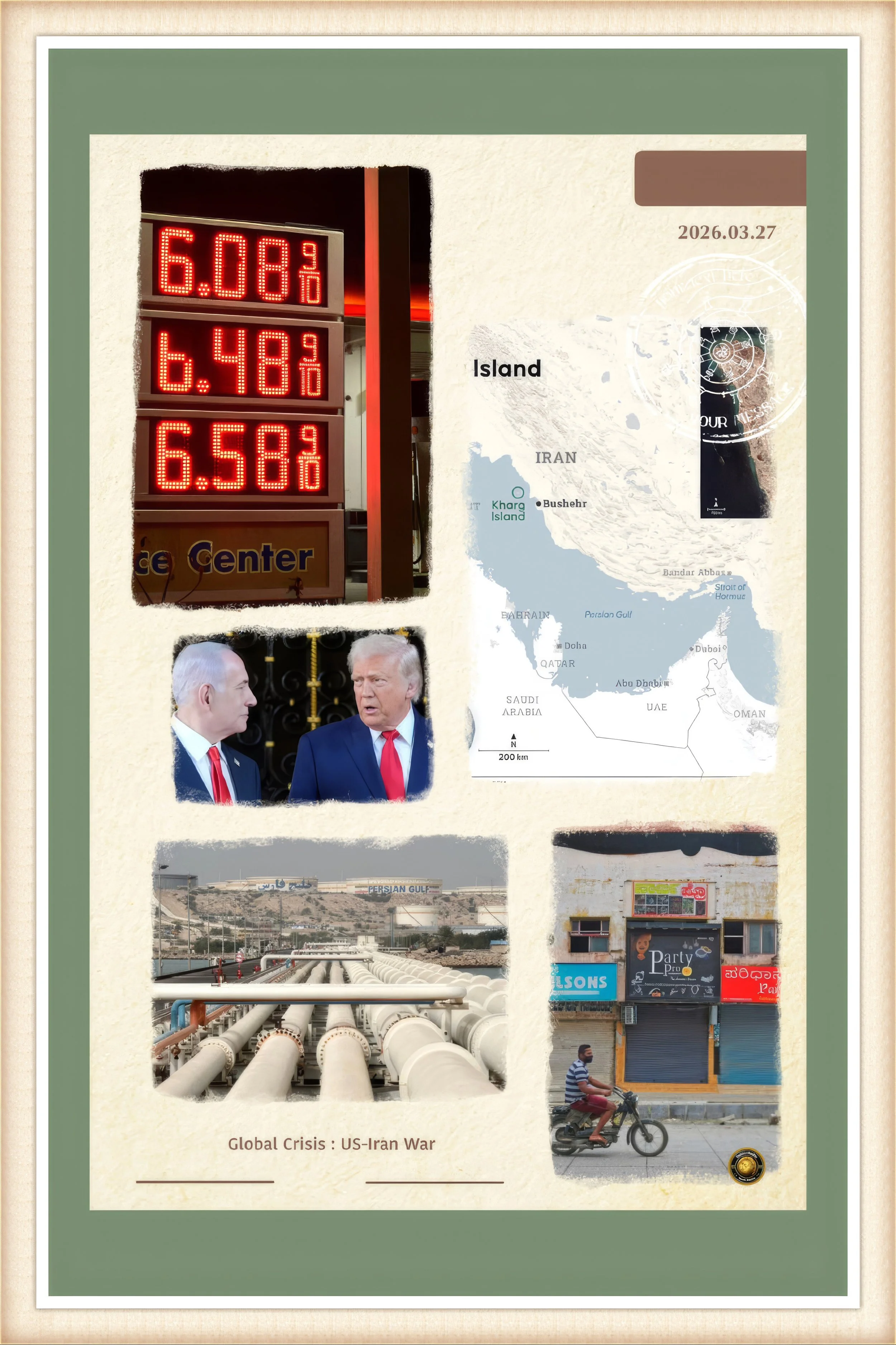

Brent crude surged past $114 per barrel within weeks of the conflict's outbreak, before settling near $100 as diplomatic signals flickered and then dimmed.

Iran's retaliatory campaign has struck at the very arteries of global energy supply — choking the Strait, targeting Qatar's Ras Laffan liquefied natural gas (LNG) complex, and menacing Saudi Arabian infrastructure — in a coordinated strategy designed to impose maximum economic pain on the Western coalition and its Gulf allies.

The consequences are reverberating across the Global South with devastating immediacy: Pakistan has closed schools for two weeks and shifted universities online, while Laos has reduced its school week from five days to three.

Meanwhile, advanced economies in Europe are contending with fuel prices at pumps exceeding $2.32 per liter and the onset of social unrest. Energy infrastructure repair costs across the Middle East are now projected to exceed $25 billion.

FAF article examines how the crisis unfolded, what structural consequences it is already generating, and what its longer-term implications may be for the global energy order, the clean energy transition, and the geopolitical balance of power.

Introduction: The Chokepoint That Moved the World

The Energy Crisis Explained: Why Pakistan's Children Are Staying Home Because of a War in Iran

Few geographical features have occupied as central a place in the calculus of global power as the Strait of Hormuz.

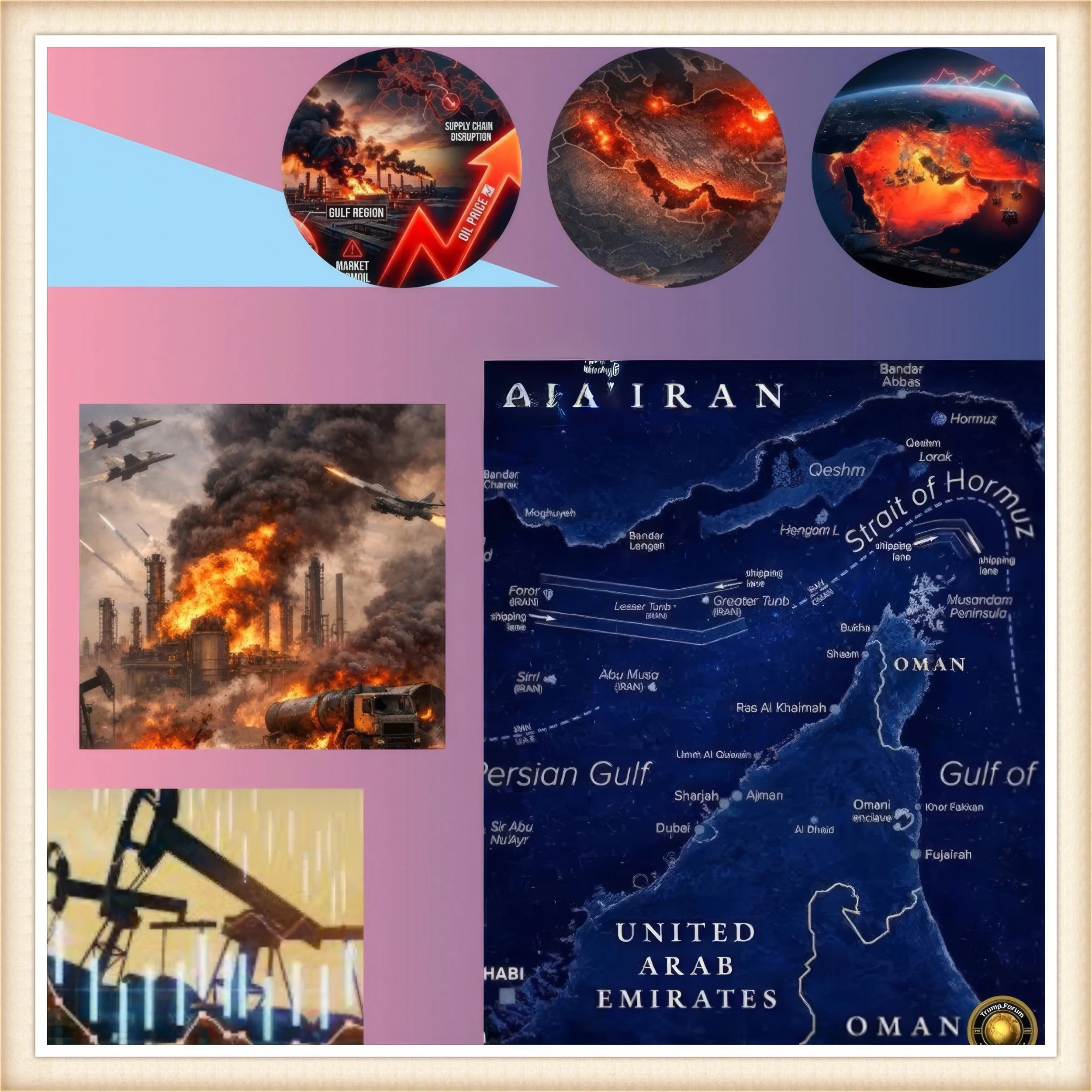

At its narrowest, the waterway is approximately 20.5 mile wide and yet channels approximately 20% of the world's daily crude oil and liquefied natural gas flows.

In 2025, this amounted to roughly 20 million barrels of oil and oil products per day — a volume so enormous that its interruption does not merely perturb energy markets but ruptures the metabolic foundations of the global economy.

When, on February 28th, 2026, the Islamic Revolutionary Guard Corps (IRGC) broadcast a chilling message on VHF radio ordering every vessel in the vicinity to halt its passage, the world's most critical energy chokepoint was, in effect, declared closed.

The causes of the crisis stretch back through decades of accumulated strategic tension.

The United States and Israel launched coordinated airstrikes on Iran on that date, strikes that included the killing of Supreme Leader Ali Khamenei.

Iran's response was swift, layered, and ruthless: retaliatory missile and drone attacks on US military installations, Israeli territory, and neighboring Gulf states, combined with an IRGC campaign of systematic vessel attacks — 21 confirmed strikes on merchant ships as of March 12th, 2026 — that effectively terminated commercial transit through the strait.

Tanker traffic dropped by approximately 70% within days, then plunged toward zero. More than 150 vessels anchored outside the strait to avoid Iranian aggression.

The energy shock that followed was immediate, structural, and, analysts now warn, potentially permanent in its long-term consequences even if a ceasefire were secured tomorrow.

Jason Bordoff, founding director of the Center on Global Energy Policy at Columbia University and a former senior director on energy and climate in the National Security Council under President Barack Obama, has described the conflict's impact as having "wide-ranging, long-lasting impacts on energy and climate policy."

FAF analysis traces those impacts — backward into the historical record for context, forward into the scenarios that now confront policymakers, and outward across the geopolitical landscape to identify the stakeholders that stand to gain and those that face existential loss.

History and Current Status: The Long Road to the Hormuz Crisis

The Biggest Energy Crisis in History: Simple Answers to the Questions Everyone Is Asking

To understand the 2026 crisis, one must situate it within the longer arc of petro-geopolitics stretching back to the first great oil shock of 1973, when Arab members of the Organization of Petroleum Exporting Countries (OPEC) embargoed oil exports to the United States and other Western nations in retaliation for American support of Israel during the Yom Kippur War.

That embargo — which lasted approximately two months — triggered a quadrupling of oil prices and plunged Western economies into recession, exposing with brutal clarity the degree to which industrial modernity had been built atop a foundation of Middle Eastern hydrocarbons.

The second oil shock of 1979, precipitated by the Iranian Revolution and the subsequent Iran-Iraq War, reinforced this structural vulnerability, with oil prices again spiking and inflation surging across the industrialized world.

The IEA was itself born directly from these crises, established in 1974 under the auspices of the Organisation for Economic Co-operation and Development (OECD) precisely to coordinate emergency responses to supply disruptions through strategic petroleum reserves (SPR) and demand-side management.

For the next four decades, the IEA oversaw a global energy governance architecture premised on the assumption that the Hormuz Strait would remain, in practice, open — a vulnerability acknowledged but never fully remedied.

Iran had long understood that the Strait constituted its most powerful card in any confrontation with the West.

Threats to close Hormuz surfaced repeatedly during the nuclear negotiations of the 2010s, during the maximum pressure campaign of the Trump administration's first term, and again during the naval incidents of 2019.

Each episode rattled energy markets; none triggered an actual closure.

The 2026 crisis is categorically different. For the first time in the history of the post-war energy order, the strait has been not merely threatened but operationally closed, not through a single dramatic act, but through a sustained campaign of maritime violence that has made commercial transit economically and physically untenable.

As of late March 2026, Iran has conducted 21 confirmed attacks on merchant vessels. Shipping firms have suspended operations in the area. Tanker traffic has fallen from the pre-crisis rate of approximately 20 million barrels per day to near zero.

The IEA announced on March 11th, 2026, the largest coordinated release of strategic petroleum reserves in its history — 400 million barrels across its 32 member countries, with the United States contributing 172 million barrels from its Strategic Petroleum Reserve (SPR).

IEA Executive Director Fatih Birol acknowledged that this historic release could theoretically compensate for approximately 20 to 45 days of Hormuz disruption, but warned explicitly that markets would not recover swiftly even after the conflict ended. "It will take some time to return to the normal conditions we experienced before the onset of the war," he stated.

Key Developments: Infrastructure Under Attack, Markets in Freefall

Why the 2026 Strait of Hormuz Crisis Is Bigger Than Both 1970s Oil Shocks Combined

The most consequential dimension of Iran's retaliatory strategy — beyond the strait closure itself — has been its targeting of regional energy infrastructure.

Qatar, the world's largest LNG exporter, has been among the most severely affected. Iranian drones and missiles struck the Ras Laffan Industrial City, home to Qatar's major LNG terminals, in a series of attacks that began in the earliest days of the conflict.

Qatar's state-owned QatarEnergy triggered force majeure clauses — contractual provisions allowing parties to suspend obligations in response to extraordinary circumstances — a development with enormous implications for the global gas market.

The Pearl GTL plant, the world's largest gas-to-liquids facility operated by Shell, sustained damage during the first assault on Ras Laffan, with the attack affecting approximately 17% of Qatar's LNG capacity. Repair timelines are now estimated at between three and five years.

A planned expansion of Ras Laffan's LNG facilities — designed to add 6 additional LNG trains by 2027 — is now expected to face significant delays.

Israel's strikes on Iran's Asaluyeh complex — which processes gas from the offshore South Pars field, shared with Qatar — damaged 4 processing facilities, further reducing regional supply.

Saudi Arabia's energy infrastructure has not been immune. Reports from mid-March 2026 indicated a drone struck facilities at Yanbu, while a ballistic missile aimed at the port was intercepted.

The East-West pipeline connecting Saudi Arabia's eastern oil fields to the Red Sea port of Yanbu has thus far remained operational, but the margin of safety is narrowing daily.

On the pricing front, Brent crude surged to $114 per barrel in the early days of the crisis before settling near $100 following President Trump's announcement of what he characterized as productive diplomatic discussions with Iran — discussions Iran publicly denied.

Analysts at Rystad Energy warned that Brent could reach $135 per barrel if current conditions persist for four months.

Morgan Stanley raised its 2027 Brent forecast to $80 per barrel, reflecting what analysts described as a "lasting repricing of geopolitical risk" after the Hormuz disruption left the market structurally tighter than previously assumed. Goldman Sachs projected that Brent may spike to $110 in the March–April 2026 period.

Middle East energy infrastructure repair costs are now projected to exceed $25 billion, according to financial analysts.

Total energy market losses, including disrupted LNG contracts, oil cargo rerouting costs, and insurance surcharges, are likely to far exceed this figure when indirect costs are incorporated into the calculus.

Latest Facts and Concerns: The World That Woke Up Without Energy

How the World Ran Short of Energy and Why Ordinary People Are Paying the Price

The human costs of the energy shock are already manifesting in starkly unequal ways across the global income spectrum.

Pakistan — one of the world's most energy-import-dependent nations — moved with extraordinary speed: Prime Minister Shehbaz Sharif announced on March 9th, 2026, that 50% of public-sector employees would shift to remote work, that schools across the country would close for two weeks beginning March 16th, and that universities would migrate to online platforms to reduce both electricity consumption on campuses and the fuel required for student and staff transportation.

"The entire region is currently in a state of war," Sharif declared in a televised national address.

Bangladesh closed universities for similar reasons.

In Laos, the government announced on March 19, 2026, a nationwide reduction of the school week from five days to three days across all public and private institutions, citing fuel cost pressures so severe that household transportation to school had become economically untenable.

The Lao government extended the academic calendar to ensure curriculum completion, while the Ministry of Technology and Communications was tasked with verifying whether internet infrastructure could support a shift to online learning in an economy where digital connectivity remains severely limited.

In Europe, the picture is more economically contained but politically explosive.

Gas prices at pumps in Germany and several neighboring nations have exceeded $2.32 per liter, fueling social unrest and placing energy-intensive industrial sectors under existential strain.

European governments have scrambled to implement comprehensive energy subsidy programs, a macroeconomic response that itself poses serious challenges to already-strained fiscal positions in the aftermath of years of post-pandemic spending.

Iran's closure is not, critically, absolute in its geographic application.

Intelligence and market analysis published in mid-March 2026 revealed that Iran is selectively permitting Indian- and Chinese-flagged tankers to transit the strait, while specifically targeting vessels affiliated with Western carriers and flag states.

This selective Hormuz arrangement has profound strategic implications: it effectively prevents India and China from joining any Western-led counter-Iran coalition, creates an economic incentive for both Asian giants to oppose escalatory US military responses, and supplies Iran with a revenue stream — payment for facilitated passage, likely settled in Chinese yuan or Indian rupees — at the very moment Western sanctions are attempting to strangle Iranian finances.

Cause-and-Effect Analysis: The Architecture of Cascading Consequences

The 2026 Energy Emergency: What Every Family Needs to Know About Oil and War

The causal chain that runs from the US-Israeli strikes of February 28th through to the global energy emergency of March 2026 is neither simple nor linear.

It is, rather, a cascade of interlocking effects that each amplify the next in ways that even sophisticated energy models failed to fully anticipate.

The immediate trigger was, of course, the military strikes themselves and the killing of Khamenei — an act that crossed a threshold that Iranian strategic doctrine had long designated as warranting maximum retaliation.

Iran's response was calibrated to inflict the maximum sustainable economic damage on the adversarial coalition without necessarily inviting a ground invasion: closing the strait, striking Gulf energy infrastructure, and conducting the selective-transit arrangement to drive a wedge between the Western coalition and its Asian counterparts.

The first-order effects were the predictable surge in oil prices and the suspension of LNG exports from Qatar.

But the second-order effects have been more structurally significant.

The $25 billion-plus in infrastructure damage to Middle Eastern energy facilities represents not merely a short-term supply disruption but a medium-term reduction in regional production capacity that will persist for years regardless of when the conflict ends. Qatar's Ras Laffan complex alone faces a 3-to-5-year recovery timeline.

The planned expansion of LNG capacity that was to add 6 trains by 2027 — a development that global gas importers, particularly in Europe and Asia, had factored into their long-term energy security planning — now faces indefinite delay.

The third-order effects extend further still. Shipping insurance premiums have surged to levels that make many cargo routes economically unviable even for vessels not directly threatened.

The rerouting of tankers away from Hormuz — where such rerouting is even possible — adds thousands of kilometers to voyages that previously ran through the strait, dramatically increasing transportation costs and transit times.

Some grades of Middle Eastern crude have no viable alternative route at all, meaning supply shortfalls for specific refineries in Asia and Europe are structural rather than merely logistical.

The fourth-order effects are now cascading through sovereign fiscal positions.

Countries like Pakistan, which spend a disproportionate share of national income on imported energy, face not merely higher fuel bills but a balance-of-payments crisis that could require emergency IMF intervention.

The forced closure of schools and universities — an education disruption that will compound over time into human capital losses — is already occurring.

The economic costs of the crisis fall most heavily on those nations with the least capacity to absorb them: the Global South, where imported energy constitutes a higher fraction of household income, government budgets, and industrial production costs.

The financial dimension is equally alarming.

The energy shock is feeding directly into global inflation, tightening monetary conditions, and weighing on asset prices across emerging markets.

The credendo analysis published in March 2026 warned of "a marked deterioration in global economic activity, weighing on inflation and global financial conditions."

Central banks in inflation-targeting economies face an agonizing dilemma: tighten monetary policy to combat energy-driven inflation at the cost of suppressing already-fragile growth, or ease conditions to support economic activity at the risk of allowing inflationary expectations to become entrenched.

The Geopolitical Landscape: Winners, Losers, and the New Energy Order

From the Persian Gulf to Your Petrol Station: How the Hormuz Crisis Hits Everyone's Wallet

The 2026 Hormuz crisis is not merely an energy emergency — it is a geopolitical inflection point that is reshaping the alignments and strategic calculations of the major powers in real time.

The concept of winners and losers in a conflict of this magnitude is necessarily crude and provisional, but the outlines of the emerging distribution of costs and benefits are already discernible.

China occupies a paradoxical position.

As the world's largest oil importer, it might be expected to figure prominently among the crisis's victims.

But China's decade-long investment in three distinct buffers — the world's largest strategic and commercial crude stockpiles, a massive renewable energy capacity, and a shift toward electric vehicles that has structurally reduced its per-unit-of-GDP oil demand — has given it a degree of resilience that most of its Asian counterparts lack.

OCBC analysts noted in early March 2026 that China is "less affected by prolonged closure of the Strait of Hormuz" than many of its regional peers.

Moreover, Iran's selective transit arrangement means that Chinese-flagged tankers continue to move through the strait at a time when Western-affiliated vessels cannot, giving Beijing privileged access to discounted Middle Eastern crude.

As Jason Bordoff observed in a March 2026 interview with POLITICO, the Iran war could, "contrary to conventional wisdom, actually strengthen China's energy dominance in the long run."

India presents a more complex case. Like China, India benefits from selective Hormuz access — Iranian passage facilitation has allowed Indian-flagged vessels to continue transiting the strait.

But India's economy is more exposed to oil price inflation than China's — it imports approximately 85% of its crude requirements — and the rupee has faced significant pressure as the current account deficit widens in response to higher energy costs.

The strategic advantage of Hormuz access must be weighed against the macroeconomic headwinds of $100-plus oil and the diplomatic tightrope that New Delhi is walking between its quasi-alliance with Washington and its energy relationship with Tehran.

Russia, despite being a party to neither the war nor its immediate geography, stands among the conflict's most significant strategic beneficiaries.

As the second or third largest oil producer globally, Russia gains from every dollar of price appreciation in Brent crude, partially offsetting the impact of Western sanctions imposed in the aftermath of the Ukraine invasion.

Every week that Hormuz remains closed strengthens Moscow's fiscal position and reduces the pressure on Putin's wartime economy.

For the European Union, the crisis represents a return of the energy security nightmare that the Russian invasion of Ukraine inaugurated in 2022.

Europe had spent the intervening 4 years diversifying away from Russian gas, building LNG import terminals, and securing supply contracts from Qatar — precisely the supplier that is now under Iranian attack.

Germany, the EU's industrial core, faces particular vulnerability: already struggling with high energy costs that have contributed to industrial contraction, German manufacturers are confronting a second energy shock before fully recovering from the first.

The Energy Transition Dimension: Accelerant or Anchor?

One of the most contested analytical questions arising from the 2026 crisis is whether it will ultimately accelerate or retard the global transition to clean energy. The answer is not simple, and expert opinion is sharply divided along structural lines.

The accelerationist case rests on the argument that price shocks expose the "insurance value" of clean energy with unparalleled clarity.

Unlike fossil fuels — which are subject to geopolitical disruption, maritime chokepoints, and production cartel manipulation — wind and solar have no fuel price risk.

Their costs are predominantly upfront capital investments; once built, they generate electricity at near-zero marginal cost regardless of what transpires in the Persian Gulf.

More than 90% of new renewable power projects worldwide in 2024 were already cheaper than fossil-fuel alternatives, according to the IEA.

The Iran war makes the economic case for accelerating this transition viscerally obvious to governments and households alike.

The deceleration case is more structural and perhaps more sobering. Modern clean energy systems are not merely generators of electricity — they are mineral-intensive, grid-intensive, and finance-intensive infrastructure projects.

Lithium, cobalt, copper, and nickel — the critical minerals that underpin batteries, wind turbines, and solar panels — face their own supply chain vulnerabilities, many of which are concentrated in geopolitically unstable regions.

Moreover, the fiscal cost of energy subsidies in crisis conditions — the billions being deployed across Europe and the Global South to shield households from the immediate price shock — crowds out the longer-term public investment required to accelerate renewable deployment.

Jason Bordoff has framed this tension with characteristic precision, noting that the war could have "wide-ranging, long-lasting impacts on energy and climate policy" and that the dual pressures of energy security and clean energy transition may either reinforce or contradict each other depending on the policy frameworks that governments adopt in response to the crisis.

The nations best positioned to use the crisis as a clean energy accelerant are those that have already built significant renewable buffers — notably China, which has simultaneously benefited from privileged Hormuz access and possesses the largest installed renewable energy base in the world.

The nations most likely to see the crisis drive fossil fuel entrenchment are those that must first solve the immediate problem of fuel supply before they can afford to think about the longer-term architecture of their energy systems.

Future Steps: Scenarios and Strategic Options

How the Iran War Is Forcing the World to Choose Between Fossil Fuels and Energy Independence

The crisis landscape presents policymakers with an array of scenarios ranging from swift diplomatic resolution to protracted conflict, and the strategic options available differ markedly depending on which trajectory materializes.

In the optimistic scenario, US-Iran negotiations — reportedly progressing, though Iran has publicly denied Trump's characterization of their progress — produce a ceasefire arrangement that gradually allows Hormuz transit to resume.

Even in this scenario, the IEA has warned that recovery will not be swift. Qatar's LNG infrastructure faces a three to five year repair timeline, meaning the global LNG market will remain structurally tight well into the late 2020s regardless of diplomatic outcomes.

Strategic petroleum reserve releases can bridge the immediate supply gap — the IEA's 400 million barrels covers approximately 20 to 45 days of Hormuz closure — but they cannot compensate for multi-year infrastructure damage.

In the pessimistic scenario, the conflict extends for months or more, oil prices approach the $135 per barrel threshold identified by Rystad Energy's analysts, and the global economic consequences extend from supply disruption into a full-scale recession.

This scenario would likely trigger emergency OPEC production increases — assuming that Saudi Arabian and UAE infrastructure remains operational — but these increases would at best partially compensate for Hormuz-routed volumes and could not prevent severe economic dislocation across energy-import-dependent economies.

A third scenario — call it the structural realignment scenario — may in some ways be the most consequential regardless of how quickly the military conflict is resolved.

The Hormuz crisis has demonstrated with empirical finality that the global energy system's dependence on a single maritime chokepoint constitutes an unacceptable systemic risk.

The response to this realization will shape the energy investment landscape for the next decade.

Countries will invest more heavily in domestic energy production, in alternative energy routes, in strategic storage capacity, and in renewable energy that is structurally immune to maritime disruption.

The IEA's $25 billion infrastructure repair estimate for the immediate damage will be dwarfed by the investment in energy system resilience that the crisis catalyzes.

The selective Hormuz arrangement that Iran has deployed — allowing Indian and Chinese vessels to pass while targeting Western-affiliated shipping — also raises a profound question about the future of the rules-based international maritime order.

If the precedent stands, it suggests that state-sanctioned economic warfare conducted through the selective application of maritime violence may become a tool that other state and non-state stakeholders incorporate into their strategic arsenals.

The Houthis in Yemen demonstrated in 2024 and 2025 that non-state groups could impose significant costs on global shipping through Red Sea interdiction.

The IRGC has now demonstrated that a state-level campaign can effectively close the world's most critical energy chokepoint. The deterrence implications for future crises are sobering.

The Role of Strategic Stakeholders: Columbia and the Policy Response

The academic and policy community's response to the crisis has been rapid and substantive.

Jason Bordoff's Center on Global Energy Policy at Columbia University convened its experts — including Anne-Sophie Corbeau, Richard Nephew, and others — in the immediate aftermath of the February 28th strikes, producing analyses of the conflict's energy implications that have informed media coverage and policy deliberations across Washington, Brussels, and beyond.

Bordoff, who served in the Obama National Security Council as a senior director on energy and climate change, brings both scholarly rigor and practitioner experience to his analysis — a combination that makes his assessments particularly valuable in a crisis where the technical and geopolitical dimensions are inseparably intertwined.

The policy choices made in the coming weeks and months will determine not merely the pace of recovery but the structural architecture of the global energy system for the next generation.

Nations that use the crisis to accelerate domestic renewable deployment, invest in energy storage, build new supply chain resilience, and pursue diversified energy diplomacy will emerge from the crisis stronger.

Those that respond purely defensively — drawing down reserves, subsidizing fossil fuels, and deferring structural reform — will find themselves no better prepared for the next disruption when it comes, as it inevitably will.

Conclusion: A Crisis That Will Not Resolve Itself

How the World's Most Dangerous Waterway Became the Fault Line of Global Energy Security in 2026

The 2026 Strait of Hormuz crisis is not merely the largest supply disruption since the 1970s — it is, as the IEA's Fatih Birol has stated unambiguously, the greatest global energy security threat in history.

Its consequences are already cascading through global supply chains, fiscal positions, educational systems, and household budgets in ways that will compound over months and years.

Brent crude trading near $100 per barrel with credible scenarios of $135 and beyond, Qatar's LNG infrastructure facing a three to five year recovery window, and more than 150 vessels anchored outside the world's most critical energy chokepoint — these are not temporary market anomalies.

They are the symptoms of a structural vulnerability in the global energy architecture that was visible for decades and never adequately addressed.

The Strait of Hormuz was always a chokepoint. The 2026 crisis has exposed, with devastating clarity, the price of allowing that vulnerability to persist.

Whether the world uses this crisis to finally build the resilient, diversified, and increasingly clean energy system that energy security demands — or whether it retreats into the comfortable illusions of cheap oil and open sea lanes — will define the energy landscape of the 2030s and beyond.