Anatomy of an Oil Shock: How One Slim Waterway, Strait of Hormuz, Brought the Global Energy System to Its Knees

Executive Summary

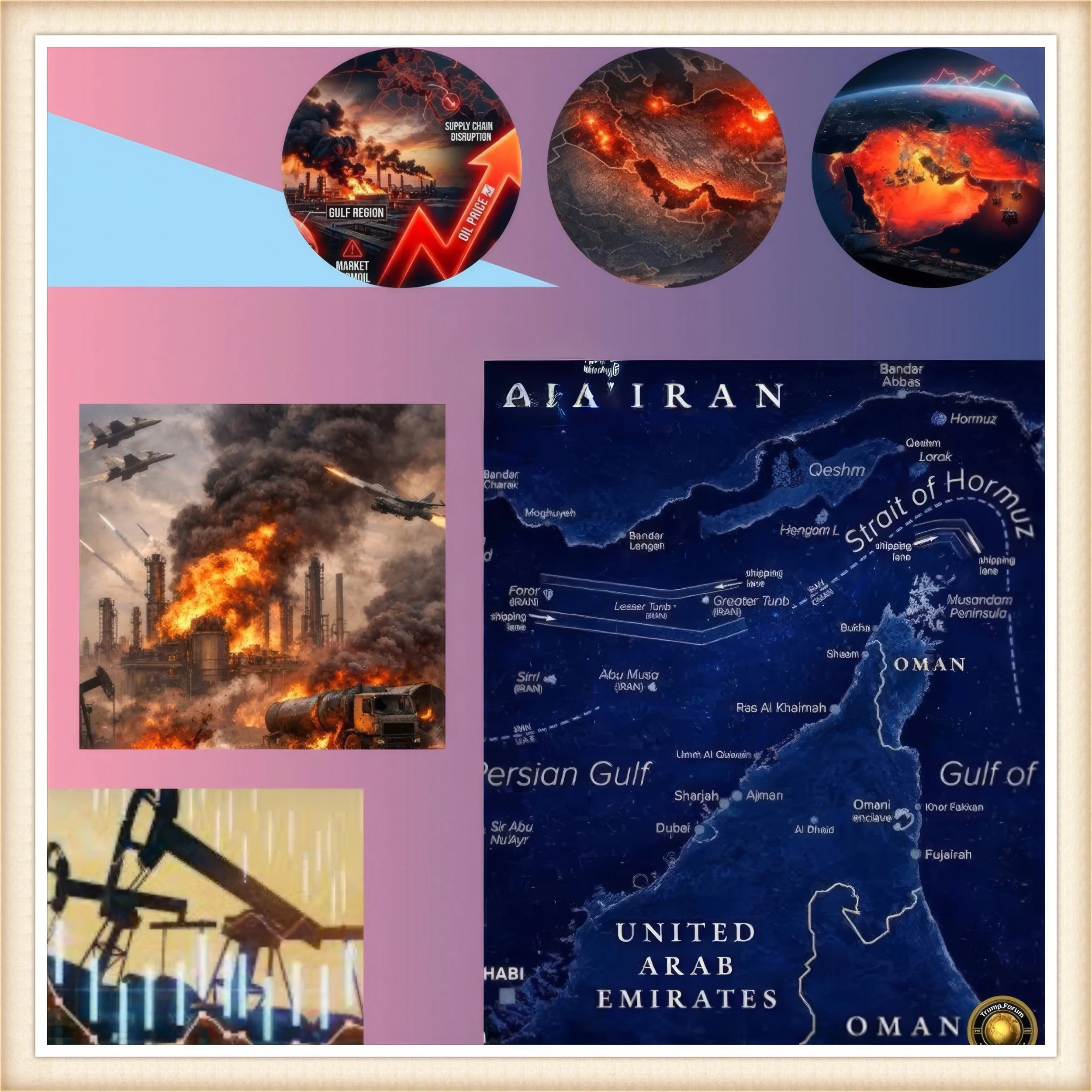

The closure of the Strait of Hormuz in late February and early March of 2026, precipitated by the third major Gulf conflict and operationalised through Iranian Revolutionary Guard Corps drone swarms, sea mines, and explicit declarations of a maritime no-go zone, has produced the most severe oil supply disruption in recorded modern history.

Approximately 20% of globally traded crude oil, along with critical volumes of liquefied natural gas, jet fuel, and liquefied petroleum gas, transited this 33-kilometre-wide passage between Iran and Oman until shipping traffic effectively collapsed following joint United States and Israeli military operations against Iranian territory, including strikes that eliminated Supreme Leader Ali Khamenei.

Crude oil prices surged past $100 per barrel for the first time in years, briefly touching $120, driven by a combination of physical supply loss, insurance market withdrawal, and acute fear premium.

OPEC+ announced a marginal production increase of 206,000 barrels per day effective April 2026, but the measure has been rendered largely symbolic as most Gulf producers — including Saudi Arabia, the UAE, Iraq, and Kuwait — have been forced to curtail output by an estimated 6.2 to 6.9 million barrels per day due to storage saturation and export route denial.

The crisis has exposed structural vulnerabilities that decades of energy transition policy have not yet resolved: the world remains irrevocably tethered to fossil fuel arteries whose geography concentrates both risk and consequence.

FAF article examines the historical antecedents of oil shocks, the precise mechanisms through which the 2026 crisis unfolded, its cascading macroeconomic effects, and the strategic recalibrations now demanded of governments, markets, and energy institutions.

Introduction

When Geography Becomes Destiny

In the calculus of strategic risk, no single waterway carries as much civilisational weight as the Strait of Hormuz.

Measuring barely 20 miles at its narrowest point and flanked on the north by Iran and on the south by the Sultanate of Oman, the strait functions as the jugular vein of the modern hydrocarbon economy.

For decades, energy analysts and geopolitical strategists treated the closure of Hormuz as a theoretical extreme — a thought experiment reserved for scenario planning exercises and congressional hearings. As of late February 2026, that thought experiment became operational reality.

The immediate trigger was Operation Epic Fury, a joint US-Israeli military campaign against Iran that, in its most consequential single action, resulted in the killing of Supreme Leader Ali Khamenei.

Iran's retaliatory posture, executed principally through the Islamic Revolutionary Guard Corps, involved missile and drone strikes against US military installations, Israeli territory, and neighboring Gulf states, as well as the deployment of sea mines and drone swarms across the strait itself.

Within hours of these declarations, commercial shipping operators, major oil companies, and marine insurers began withdrawing from the waterway.

By 2nd March 2026, at least 150 tankers were anchored in open Gulf waters, unable or unwilling to proceed.

The IRGC issued explicit threats that any vessel attempting passage would be "set ablaze." Commercial traffic, which had already been elevated in anticipation of conflict, collapsed by more than 80%.

This is not merely a crisis of commodity pricing. It is a crisis of systemic confidence — in the durability of the rules-based maritime order, in the adequacy of strategic petroleum reserves, in the feasibility of energy transition timelines, and in the assumption that geopolitical brinkmanship would, in the end, stop short of severing the arteries of global commerce.

The Hormuz crisis of 2026 demands analysis across multiple registers: historical, economic, strategic, and structural.

A Long History of Energy as a Weapon

The weaponisation of oil supply is not a twenty-first century innovation. It is, in fact, one of the defining instruments of the 20th century statecraft, deployed with devastating effect on at least three occasions before the current crisis.

Each historical episode illuminates both the mechanism and the limits of oil shock as a coercive instrument, and each offers partial but instructive analogies for the situation unfolding in 2026.

The first great modern oil shock erupted in October 1973, when Arab members of the Organisation of Petroleum Exporting Countries — responding to American logistical and diplomatic support for Israel during the Yom Kippur War — imposed an embargo on exports to the United States, the Netherlands, and several Western allies.

The volume of oil actually withheld was relatively modest in absolute terms, amounting to approximately 5% of global supply.

Yet prices quadrupled within months, long queues formed at petrol stations across the United States and Western Europe, and the Nixon administration found itself simultaneously managing a constitutional crisis and an energy emergency.

The shock illustrated a foundational principle: in tight, psychologically sensitive commodity markets, fear and uncertainty amplify physical scarcity by orders of magnitude.

The real damage was not done by barrels withheld but by the collapse of confidence that markets would receive adequate supply.

The second great shock came in 1979, triggered by the Iranian Revolution and the fall of the Shah.

Iranian production, then among the highest in the world, fell precipitously as the revolutionary government consolidated power. Global oil prices roughly doubled again.

A third shock arrived within months when Iraq invaded Iran, launching the first Gulf War and damaging production infrastructure in both countries.

For the remainder of the 1980s, the Strait of Hormuz itself became a landscape of the Tanker War, during which both sides attacked shipping in the Gulf and Iranian forces periodically threatened closure.

The United States deployed naval escorts — Operation Earnest Will — to protect Kuwaiti tankers, establishing a precedent of military involvement in Hormuz navigation that has echoed across every subsequent Gulf crisis.

Critically, the strait was never fully closed during that conflict. Threats materialised into significant disruption but not total interdiction.

The third foundational episode was the Gulf War of 1990 to 1991, triggered by Iraq's invasion of Kuwait.

Oil prices initially spiked dramatically before a coordinated international response, led by the US-assembled coalition, rapidly stabilized markets through a release of strategic reserves and the swift military campaign that restored Kuwaiti sovereignty.

The 2003 invasion of Iraq produced more sustained but less acute price elevation, as markets absorbed the uncertainty over a longer period.

Throughout all these episodes, the actual closure of Hormuz — the full, enforced interdiction of tanker traffic — remained an event that was threatened, prepared for, gamed out, but never fully executed.

That changed in 2026.

What was previously the nightmare scenario has become operational fact.

The 2026 Crisis: How It Unfolded

The immediate geopolitical context of the 2026 crisis was shaped by an extended confrontation between the United States and Iran that had already produced one prior military episode — a 12-day exchange in mid-2025 — before the more decisive Operation Epic Fury escalated matters beyond any prior threshold.

Iranian crude exports had actually surged to multi-year highs in the weeks preceding the operation, as Tehran anticipated disruption and attempted to pre-position revenue.

Those barrels had largely cleared into global storage by late February, meaning the supply buffer available to markets was considerably thinner than it might have appeared.

The killing of Khamenei and the destruction of Iranian energy infrastructure by US and Israeli air power transformed Iran's calculus from coercive posturing to what the IRGC apparently regarded as existential defence.

Mining the strait and declaring it closed was not, in this reading, a tactical decision so much as a strategic one: since Iran could not match the US-Israeli coalition in conventional military terms, it chose to inflict maximum economic pain on the global system underwriting that coalition's power.

The logic was precise — elevated energy costs would undermine US consumer confidence, complicate the domestic economic narrative of the Trump administration, and create friction within the coalition by threatening the economic stability of Gulf allies and Asian partners alike.

Within the first ten days of the closure, the physical consequences were stark.

Approximately 13 million barrels per day, representing roughly 31% of all maritime oil transport according to industry data, had regularly transited the strait.

Its effective closure removed not only Iranian supply — already partially sanctioned — but the export capacity of Saudi Arabia, Iraq, the UAE, Kuwait, and Bahrain.

An estimated 6.2 to 6.9 million barrels per day of regional production was effectively landlocked as storage facilities filled beyond operational capacity and producers were forced to curtail output.

Qatar, which had proactively suspended LNG production as a precautionary measure, added a gas dimension to what was already a multi-commodity shock.

Marine insurance rates, already at a six-year peak before hostilities began, became effectively prohibitive for Gulf transits. Major oil companies and commercial operators withdrew from the strait.

At least five tankers sustained direct damage; two seafarers were killed.

The IRGC's declaration that vessels would be "set ablaze" was not merely rhetorical — it was substantiated by attacks on ships attempting passage.

The Oil Price Shock: Numbers and Psychology

The price response was immediate and severe.

Brent crude, already elevated in anticipation of conflict, surged by more than 10% in the first days following Operation Epic Fury.

Within a week it had risen by 18 to 20%, crossing $100 per barrel and briefly touching $120 before settling near $104 amid reports of partial diplomatic contacts and US naval deployments.

Analysts at leading energy research firms projected prices could reach $150 per barrel if the closure proved sustained, a level that would represent a demand-destruction threshold — the point at which prices become self-defeating by collapsing economic activity and therefore consumption.

The price surge carried an embedded paradox.

OPEC+, meeting in its previously scheduled session, approved a production increase of 206,000 barrels per day effective April 2026.

The decision was technically consistent with the alliance's gradual unwinding of prior production cuts.

But it was rendered strategically meaningless: most of the spare capacity behind that decision resided in Gulf states whose export routes ran directly through the strait now closed. OPEC+ had announced more oil without any mechanism to deliver it to markets.

Analysts described spare capacity as "landlocked" — present on paper, inaccessible in practice.

The alliance holds an estimated 3.5 million barrels per day in spare capacity, but the geography of that capacity mirrors the geography of the crisis.

The fear premium embedded in prices was not irrational.

Markets were pricing not merely the current physical supply loss but the risk of escalation — of attacks on Saudi Aramco infrastructure, of broader Gulf state involvement, of a prolonged conflict measured in months rather than days.

The correlation between oil prices and food prices added a second-order inflationary dimension, as energy costs flow through to fertiliser production, agricultural logistics, and retail food supply chains.

Central banks faced an acute dilemma: the classical monetary response to inflation — interest rate increases — risked deepening a demand shock that the supply disruption had already initiated.

The spectre of stagflation, last experienced in its virulent form in the late 1970s, began to animate policy discussions in Washington, Frankfurt, Tokyo, and New Delhi.

Who Gains, Who Loses: The Geopolitics of Pain

Oil shocks are not universally destructive.

They redistribute wealth and geopolitical leverage in ways that generate both losers and strategic beneficiaries, and the 2026 crisis is no exception.

The most immediate beneficiaries among major oil-producing stakeholders are those with export infrastructure outside the Gulf — principally Russia, Norway, Canada, and the United States itself.

Russian crude, already rerouted substantially toward Asian markets following Western sanctions imposed in 2022, was positioned to command significant premiums as Indian and Chinese buyers pivoted away from disrupted Middle East supply chains toward available alternatives.

Moscow's fiscal calculations, already recalibrated to higher oil prices, improved materially even as its military position in Ukraine continued to require external financing.

This created an uncomfortable dynamic for Washington: US military action against Iran was inadvertently improving the financial position of its adversary in Moscow.

US domestic producers stood to benefit from elevated prices, and the Trump administration found itself navigating a tension between its desire for cheap energy to sustain consumer confidence and the windfall revenues accruing to the American shale industry.

Strategic Petroleum Reserve releases were announced, but the volume available — however substantial in absolute terms — could not substitute for the sustained removal of 20% of global maritime oil trade from the supply equation.

The SPR is a shock absorber, not a replacement for hemispheric supply chains.

For Asian economies, the consequences were disproportionately severe.

India, which meets more than 85% of its crude oil requirements through imports, faced simultaneous pressures on its current account deficit, domestic inflation, and sectoral performance across aviation, automotive, chemicals, paints, and downstream energy-intensive industries.

The rupee came under immediate pressure.

Retail fuel prices were hiked; cooking gas prices had already been adjusted upward in anticipation.

Japan and South Korea, both structurally dependent on Gulf LNG, faced analogous pressures in electricity generation costs.

European economies, themselves navigating post-Ukraine energy restructuring, faced renewed pressure from LNG price surges.

The Qatar precautionary suspension of LNG production, however temporary, removed a critical swing supplier from the market at precisely the moment of greatest stress.

European natural gas benchmarks spiked in parallel with crude oil.

For the Gulf states themselves — Saudi Arabia, UAE, Kuwait, Iraq, Bahrain — the crisis was an economic catastrophe masquerading behind temporarily elevated paper prices.

The ability to monetise those elevated prices was denied by the very closure that generated them.

Production curtailments, storage saturation, and export route denial created fiscal pressure even for the region's most wealthy sovereign wealth fund holders.

The paradox of Gulf oil being worth more per barrel but impossible to sell illustrated the brutal geometry of the Hormuz chokepoint.

The Energy Transition: Stress-Testing Its Progress

A critical question embedded in the 2026 crisis is whether accelerating energy transition has materially insulated the global economy from oil shocks, or whether that insulation remains largely theoretical.

The evidence is instructive and somewhat sobering.

The energy transition has indeed progressed substantially.

By 2025, global renewable electricity capacity additions were at record levels, with solar and wind consistently outpacing fossil fuel additions in major economies.

India had achieved the milestone of 50% of its cumulative installed electricity capacity from non-fossil fuel sources as of mid-2025.

Electrification of transport, while uneven, was reducing oil consumption in key segments in Europe, China, and increasingly in the United States.

The International Energy Agency projected global oil demand growth of 830,000 barrels per day in 2025, significantly slower than historical growth rates, reflecting the dampening effects of electrification in key markets.

Yet the 2026 crisis has demonstrated, with brutal clarity, that reduced oil demand growth is not the same as oil supply independence.

The world continues to consume well over 100 million barrels of oil per day.

Renewables, however rapidly expanding, generate electricity — and electricity cannot directly substitute for the petrochemical feedstocks, aviation fuel, marine fuel, or industrial heat applications that represent a very substantial share of oil's end uses.

The energy transition is accelerating in the generation sector but is structurally slower in the transport, industrial, and chemical sectors most acutely exposed to price volatility.

Moreover, the concentration of remaining oil demand in sectors less amenable to electrification creates a paradox of transition: as the easy substitutions are made, what remains is structurally harder to replace and proportionally more vulnerable to supply shocks.

The 2026 crisis has therefore arrived at precisely the inflection point where the world is dependent enough on oil to be severely affected by its disruption, but not yet sufficiently decarbonized to absorb the shock without macroeconomic damage.

Policymakers Under Pressure: Institutions and Responses

The institutional response to the 2026 Hormuz crisis has been simultaneously comprehensive in its ambition and constrained in its efficacy.

Strategic petroleum reserve releases were coordinated among International Energy Agency member states, but the mathematical mismatch between reserve drawdown rates and the sustained physical supply loss rendered this a palliative rather than a solution.

Central banks in major economies signaled readiness to act on financial stability grounds while acknowledging the fundamental impossibility of addressing a supply-side energy shock through monetary instruments alone.

The US naval deployment to the Gulf — consistent with the Earnest Will precedent of the 1980s — aimed to create corridor security for allied shipping, but the political dynamics of escorting vessels through an active mine field, amid drone swarm operations, with casualties already incurred, proved considerably more complex than the command structures had anticipated.

The practical reopening of the strait required not merely naval presence but the cessation or decisive suppression of IRGC maritime operations, which in turn depended on the broader resolution of the US-Iranian conflict — a timeline measured in weeks at minimum.

Diplomatic channels through Omani interlocution — historically the preferred back-channel for US-Iran communication — were reportedly active, but the killing of Khamenei had fundamentally altered Iran's political structure.

With Mojtaba Khamenei named as the new Supreme Leader, the internal consolidation of authority within Iran's theocratic hierarchy was itself incomplete, creating uncertainty about who held effective decision-making power over the IRGC's operational stance.

This institutional fluidity in Tehran added layers of unpredictability to the crisis management calculus.

The Gulf Cooperation Council states navigated their own acute tensions.

Their dependency on the strait for export revenues placed them in fundamental alignment with Hormuz reopening, yet their proximity to Iranian retaliatory capability — demonstrated through strikes on GCC territory — constrained the degree to which they could publicly or operationally support US military objectives.

The destruction of water desalination plants in the region — which analysts noted breached previously observed red lines — elevated the humanitarian stakes and complicated the political economy of GCC coordination.

Cause and Effect

A Structural Analysis

The 2026 Hormuz crisis is not an anomalous event produced by random contingency.

It is the predictable outcome of a set of structural conditions that have been accumulating across decades: the geographic concentration of global oil production in a politically volatile region; the failure to build adequate alternative export infrastructure; the absence of a credible global governance framework for critical maritime chokepoints; and the willingness of state stakeholders facing existential military pressure to resort to maximum economic disruption as an instrument of asymmetric warfare.

Iran's strategic logic, as reconstructed from its actions, was internally coherent. It could not match US-Israeli conventional military superiority. It could not deter strikes on its nuclear or energy infrastructure through threats of direct military retaliation.

What it could do was impose costs through the one instrument uniquely available to its geographic position: control of Hormuz.

The pre-positioning of warheads near regional borders before the crisis suggested that the broader escalation was planned rather than improvised — Iran had prepared for this scenario even if the precise trigger remained uncertain.

The effect of that strategic calculation is radiating outward through the global economic system in ways that are both immediate and durable.

Oil prices at $100 to $120 per barrel represent a direct transfer of wealth from oil-importing economies — covering the majority of the world's population — to oil-exporting entities capable of monetizing elevated prices.

This transfer is inflationary, demand-suppressive, and fiscally destabilizing for governments that subsidize domestic energy consumption. It also deepens pre-existing inequalities between energy-secure and energy-insecure nations.

The macroeconomic transmission mechanism is well established.

Higher oil prices raise transportation costs, which elevate prices for virtually every trade-able good. They increase the cost of petrochemical inputs across manufacturing supply chains.

They raise the cost of agricultural production through fertilizer and machinery fuel impacts. They squeeze household disposable incomes, reducing consumption across discretionary and, at extreme price levels, even non-discretionary categories.

Central banks, constrained from easing monetary policy by the inflationary impulse, cannot offset the demand destruction through conventional tools.

The combination of supply-shock inflation and demand destruction defines stagflation — the most intractable macroeconomic configuration for policy management.

At extreme price levels — the $150 per barrel threshold identified by multiple analysts — demand destruction becomes significant enough to collapse the demand side of the oil market itself, setting the stage for an eventual violent price correction.

The path to such a correction, however, passes through a period of severe economic disruption that falls disproportionately on lower-income households and emerging market economies.

Future Steps

What Comes After the Shock

The resolution of the 2026 Hormuz crisis will unfold across three timescales: the immediate, the medium-term, and the structural. Each demands different instruments and different stakeholders.

In the immediate term, the priority is the physical reopening of the strait to commercial navigation.

This requires either a ceasefire in the US-Iran conflict sufficient to halt IRGC maritime operations, or a naval enforcement campaign capable of suppressing mine and drone threats to a level that insurers and commercial operators regard as acceptable. Neither option is straightforward.

A ceasefire requires political counterparts in Tehran with authority to deliver — the post-Khamenei transition period introduces profound uncertainty.

A naval enforcement campaign risks escalation and casualty spirals that could deepen, rather than resolve, the conflict.

The US and its partners must also manage the expectations and safety concerns of Gulf state governments whose populations are exposed to Iranian retaliatory capability.

In the medium term — over a period of 6 to 24 months — the crisis will accelerate several structural responses. Alternative pipeline routes, already under discussion for years, will receive urgent political and financial support.

The Abu Dhabi Crude Oil Pipeline, which bypasses Hormuz and has capacity for approximately 1.5 million barrels per day, will be fully utilised.

Saudi Arabia's East-West Pipeline, with capacity of approximately 4.8 million barrels per day, connects Gulf fields to Red Sea terminals.

These alternative routes cannot fully substitute for Hormuz transit volumes, but they materially reduce dependence on the strait for the Gulf's two largest producers.

Strategic petroleum reserve frameworks will be reviewed globally, with pressure to expand both volume and accessibility.

The 2022 SPR release in response to the Russia-Ukraine conflict demonstrated both the utility and the limitations of reserve-based market stabilization; the 2026 crisis will likely prompt legislative and administrative reform in major consumer nations.

The energy transition itself will receive a powerful political impetus.

Every oil shock in history has triggered renewed investment in energy security diversification — the 1973 embargo prompted the establishment of the IEA and the development of North Sea and Alaskan production; the 1979 shock accelerated conservation mandates and efficiency standards.

The 2026 crisis will similarly accelerate investment in renewables, electrification infrastructure, and demand-side efficiency, not purely from climate motivation but from the strategic imperative of reducing exposure to Hormuz-type vulnerabilities.

The crisis has made the geopolitical case for energy transition in terms that even the most skeptical industrial and political stakeholders cannot easily dismiss.

Structurally, the 2026 crisis will force a fundamental reappraisal of the geography of energy risk.

The concentration of proven oil reserves in the Persian Gulf — a region of enduring political volatility — is not an accident of geology that can be wished away.

Managing that concentration requires a multi-decade strategy combining supply diversification, demand reduction through electrification, infrastructure redundancy, and diplomatic frameworks that reduce the probability of major power conflicts in the Gulf region.

The failure to build those frameworks in the decades since the Tanker War of the 1980s represents a collective strategic failure for which the world is now paying a considerable price.

Conclusion

The Price of Dependence

History does not repeat itself, but it rhymes with uncomfortable precision.

The 2026 Hormuz crisis rhymes with 1973, with 1979, with the Tanker War of the mid-1980s — but in each case with the volume turned higher, the physical consequences more severe, and the institutional buffers somewhat less adequate relative to the scale of disruption.

The strait has never been closed in recorded modern history.

That it has now been effectively closed for the first time establishes a precedent of incalculable consequence: it demonstrates that the threat, long treated as a theoretical extreme, is an operational reality that state stakeholders can and will execute when sufficiently pressed.

The world's oil dependency is not simply a technological or economic condition. It is a geopolitical vulnerability embedded in the physical geography of hydrocarbon reserves and the political instability of the Gulf.

The energy transition, however genuinely transformative over a multi-decade horizon, has not yet progressed far enough to insulate the global economy from the shock of a Hormuz closure. The 2026 crisis has exposed that gap with devastating clarity.

What it has also exposed, less dramatically but no less consequentially, is the inadequacy of the world's collective risk management frameworks for energy security.

The SPR exists but is insufficient. OPEC+ spare capacity exists but is landlocked. Alternative pipeline routes exist but are under-capacity.

Diplomatic back-channels exist but are disrupted by the very escalation they are designed to prevent.

The architecture of resilience, assembled over 50 years since 1973, has proven inadequate to the scenario it was always ultimately designed to address.

The economic consequences — stagflation, demand destruction, fiscal stress across emerging markets, potential global recession — are not a surprise to any analyst who has studied the history of oil shocks.

They are the known, predictable output of a known, predictable vulnerability that the international community chose, repeatedly, not to fully resolve.

The Hormuz crisis of 2026 is, in this sense, not merely a geopolitical shock. It is a bill coming due on decades of strategic complacency.