An Attack on the World Economy: The Strait of Hormuz Crisis, Energy Markets, and the Geopolitical Reckoning of 2026

Executive Summary

How the Strait of Hormuz Became the World's Most Dangerous Economic Chokepoint in 2026

The de facto closure of the Strait of Hormuz in early March 2026, following United States and Israeli military strikes against Iran beginning on February 28th, has produced one of the most severe and structurally consequential energy market disruptions since the oil shocks of the 1970s.

Brent crude oil prices surged from approximately $70 per barrel before hostilities began to nearly $120 per barrel within 10 days, before partially retreating toward $80 following signals from President Donald Trump on March 9 that military operations would conclude "very soon."

By March 13, however, Brent crude had climbed back above $100 per barrel, undermining earlier optimism and revealing how profoundly fragile the global energy architecture remains when a single maritime corridor is placed under threat.

The crisis has simultaneously disrupted approximately 20% of global oil supply, frozen roughly 20% of the world's liquefied natural gas (LNG) trade, forced Saudi Arabia, the UAE, Iraq, and Kuwait to slash collective output by millions of barrels per day, and triggered emergency reserve releases from the International Energy Agency (IEA) at historic scale.

The macroeconomic consequences — including stagflationary shocks, threats of global recession, currency volatility, and cascading inflation — have forced a fundamental reassessment of the durability and design of the global energy order.

Whatever the diplomatic resolution of the military conflict, the energy markets as they existed before February 28th have been permanently altered.

Introduction: A Chokepoint That the World Could Not Afford to Lose

From Tariffs to Tankers: Trump Discovers the Unbearable Political Cost of War in the Gulf

Geography, as classical strategic theorists have long argued, does not yield to political convenience.

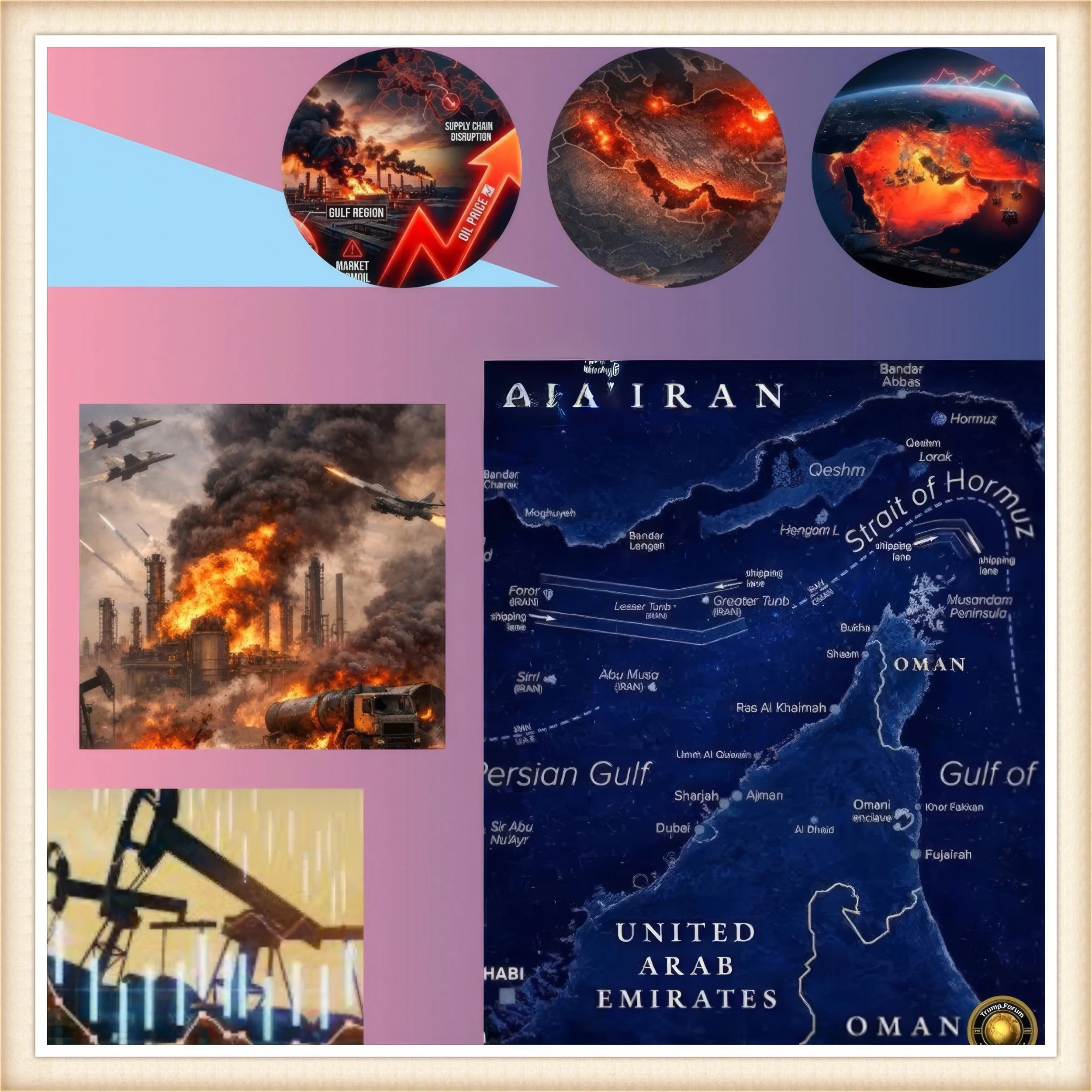

The Strait of Hormuz — a narrow waterway approximately 20.5 Mile wide at its most constricted point, separating the Iranian coastline from the Sultanate of Oman — has for decades stood as the world's most consequential maritime energy corridor.

In the years leading up to the 2026 crisis, roughly 20 million barrels of oil per day, or approximately 20% of global petroleum liquids consumption, transited this passage daily, representing nearly $600 billion in annual energy trade.

Approximately 20% of global LNG flows, the bulk of them originating in Qatar, passed through the same waterway.

Despite repeated warnings from energy analysts, geopolitical researchers, and strategic thinkers that the strait represented an existential vulnerability in the architecture of global energy supply, neither markets nor policymakers adequately priced in the systemic risk of its closure — until that closure became a present reality.

The US-Israeli military campaign against Iran, launched on February 28, 2026, transformed a long-standing theoretical risk into an operational catastrophe of the first order.

Within days, Iranian drone and missile attacks on tankers, combined with explicit threats from the Islamic Revolutionary Guard Corps (IRGC) to treat any vessel associated with the United States, Israel, or their allies as a "legitimate target," effectively stopped maritime traffic through the strait.

Lloyd's List Intelligence reported an 80% drop in seaborne traffic by early March. Data from the first week of March revealed a staggering 83% reduction in shipping activity compared to normal volumes.

The world had lost access to one in every five barrels of its daily oil supply, not through an embargo or an OPEC production decision, but through the application of asymmetric military force at the world's most vulnerable energy chokepoint.

The consequences for global markets, politics, and the structural architecture of energy supply are both immediate and enduring.

History and Current Status: The Strait Through the Centuries of Strategic Contest

Oil at $120 a Barrel and Rising: Trump's Iran War Rewrites the Rules of Global Energy Markets

The Strait of Hormuz has occupied a central place in strategic and commercial geography for millennia.

From the Hormuz trading kingdom of the medieval era to the Portuguese fortifications of the sixteenth century and the British imperial presence that endured into the mid-twentieth century, control of the passage between the Persian Gulf and the Gulf of Oman has been a prize of extraordinary geopolitical significance.

The modern energy dimension of this geography emerged with the explosion of Persian Gulf oil production in the mid-twentieth century, transforming the strait from a regional commercial route into one of the fundamental arteries of the global industrial economy.

The first serious modern test of the strait's vulnerability came during the Iran-Iraq War of 1980 to 1988, when the so-called Tanker War of 1984 to 1988 saw hundreds of merchant vessels attacked by both belligerents.

The United States ultimately intervened through Operation Earnest Will in 1987 and 1988, re-flagging Kuwaiti tankers and providing US Navy escorts to protect the flow of Gulf oil.

That intervention established a precedent of American military commitment to keeping the strait open that shaped regional security assumptions for nearly four decades.

Subsequent crises — including Iranian threats to close the strait during periods of tension over its nuclear program between 2011 and 2019 — were contained through a combination of deterrence, diplomacy, and the credible American naval presence in the Fifth Fleet, headquartered in Bahrain.

The 2026 crisis represents a qualitative rupture with this history.

For the first time, the strait has been functionally closed not through a formal blockade but through the application of drone and missile capabilities against commercial shipping, combined with the withdrawal of maritime insurance coverage by major international underwriters.

By March 2, 2026, on a waterway that normally sees 24 major vessels transit per day, only four were recorded making the passage.

Iran's IRGC declared that not "a liter of oil" would pass, and Iranian military spokesperson Ebrahim Zolfaqari warned that oil prices would reach $200 per barrel, asserting that "the oil market hinges on regional stability, which you have unsettled."

These are not the rhetorical postures of a minor regional contestant but the operationally credible statements of a state that has demonstrated, in real time, its capacity to halt the flow of one fifth of the world's oil.

As of March 13, Brent crude stood above $100 per barrel, having already achieved the largest single-week increase in oil prices since the COVID-19 pandemic's initial shock in 2020.

WTI crude futures were trading at $95.87 per barrel. The IEA has authorized the release of a historic 400 million barrels from emergency strategic reserves — a measure without modern precedent in scale.

The White House has temporarily lifted certain sanctions on Russian oil exports in an effort to supplement global supply, a development that carries its own profound geopolitical implications.

Meanwhile, tankers carrying Gulf crude are sitting stranded in port or at anchor, their cargoes undeliverable and their operators unable to secure insurance at any commercially viable premium.

Key Developments: The Architecture of a Crisis

Stagflation Returns: Why the Hormuz Crisis Threatens to Repeat the Economic Trauma of the 1970s

The sequence of events that produced the Hormuz crisis of 2026 reflects a convergence of strategic miscalculation, structural vulnerability, and the domestic political pressures of the most powerful state in the international system.

The United States and Israel launched coordinated military strikes against Iran on February 28, 2026, in what the Trump administration framed as an operation to neutralize Iran's nuclear capabilities.

The immediate market response was sharp but not initially catastrophic: US crude prices surged by 7.5% and Brent rose by 6.2% on the first day of hostilities.

Oil had already been trading elevated in anticipation of potential military action, and at first, markets appeared to price in a short, decisive campaign followed by a rapid normalization.

That calculus proved dramatically mistaken. Rather than accepting military defeat passively, Iran activated its asymmetric maritime capabilities with a speed and effectiveness that caught both planners and markets off guard.

Within the first four days of the conflict, Iran had employed drones and direct threats to produce an 80% reduction in shipping traffic through the strait.

At least four tankers were struck by drones. Qatar's state-owned energy company suspended LNG production "due to military attacks."

Satellite imagery revealed damage to sections of Saudi Arabia's Ras Tanura refinery — the largest in the country — forcing it to cease operations after two drones were intercepted above the facility.

A fire erupted in the UAE port of Fujairah, a critical oil storage and trading hub, after a drone was intercepted.

Iran had effectively extended the conflict landscape from the purely military domain into the energy infrastructure of the entire Gulf region.

The response of Gulf oil producers to the effective closure of their primary export route has been equally dramatic.

Saudi Arabia, the world's largest oil exporter, has reduced production by between 2 million and 2.5 million barrels per day, as rapidly filling onshore storage tanks leave producers no alternative to cutting output.

Bloomberg News reported the UAE cutting output by 500,000 to 800,000 barrels daily; Kuwait reducing production by 500,000 barrels per day; and Iraq slashing approximately 2.9 million barrels per day.

JP Morgan calculated that Gulf nations collectively can store approximately 343 million barrels of oil as a buffer against a complete production halt, but Rystad Energy warned that Iraq's remaining operational oil fields "face an imminent, near-certain shutdown" as storage capacity approaches exhaustion.

The combined Gulf production cuts represent one of the largest involuntary supply reductions in the history of oil markets, not driven by OPEC cartel discipline but by the physical impossibility of exporting through a contested maritime corridor.

Trump's political positioning has evolved rapidly under these pressures.

On March 5, he told Reuters that he was "not concerned" about rising gas prices and that the military operation remained his priority, adding that if gas prices "rise, they rise."

By March 9, with Brent crude approaching $120 per barrel and the national average US gasoline price reaching $3.48 per gallon — a 17% increase from pre-war levels — Trump pivoted sharply, declaring the campaign "very complete" and suggesting it would be "over very soon."

Oil prices crashed toward $80 on his comments, but the recovery was short-lived.

By March 13th, crude was back above $100 per barrel, with Trump then saying the United States "has plenty of time" to continue fighting — a statement that drove another round of price increases.

Latest Facts and Concerns: The Dimensions of Damage

The Closure That Changed Everything: How Iran Shut Down One Fifth of the World's Oil Supply

The economic data accumulating from the Hormuz crisis presents a landscape of compounding damage across multiple dimensions of the global economy.

The scale of the supply disruption is unprecedented in the post-1973 era in terms of its speed of onset.

China, which sources approximately 45.7% of its oil through the Strait of Hormuz, faces the most acute import dependency of any major economy.

Japan and South Korea, which import roughly 80% of their energy needs, are confronting what analysts have described as a "cold reality" as Qatari LNG — their primary alternative gas source — has been frozen in Gulf storage.

European wholesale gas prices have surged by 25%, as the continent — still structurally dependent on alternative LNG supplies following the loss of Russian pipeline gas in 2022 — finds those alternatives now bottled up in the same Gulf corridor.

Goldman Sachs and UBS analysts have warned that if the disruption extends through the second quarter of 2026, global headline inflation could rise by 0.7 to 0.8 % points, while global GDP growth could face a drag of up to 0.4 percentage points — effectively erasing the gains of the post-2024 global economic recovery.

The Economist has stated directly that if the Strait of Hormuz remains closed until the end of March, crude could surge to $150 or even $200 per barrel, conditions that would constitute "a recipe for global recession and a surge in inflation — a repeat of the stagflation of the 1970s."

Warren Hogan, economic advisor at Judo Bank, called the episode potentially "one of the most abrupt increases in oil costs impacting the global economy ever."

Iran's threats have extended beyond tanker attacks. Dubai has reported drone attacks, Kuwait's airport has been targeted, and Iranian-affiliated forces have sustained pressure on energy infrastructure across the Gulf.

The maritime insurance landscape has been effectively destroyed as a functional market for Gulf shipping, with major international underwriters withdrawing coverage entirely after the first week of hostilities.

Without insurance, commercially operated tankers cannot legally or practically transit the strait, making the functional closure self-reinforcing even if physical threat levels fluctuate.

The IEA's release of 400 million barrels from strategic reserves, while historic, represents a finite intervention against what could be a structural shift in supply availability that lasts months or longer.

Cause-and-Effect Analysis: How One Waterway Became the Pivot of Global Economic Fate

Midterms, Markets, and Military Campaigns: The Political Economy of America's War Against Iran

The causal architecture of the 2026 Hormuz crisis is neither simple nor monocausal.

It reflects the intersection of multiple long-building structural vulnerabilities with a specific set of policy choices made by the Trump administration in early 2026.

The foundational structural cause is the extreme and persistent concentration of global energy export infrastructure around a single chokepoint.

Despite decades of theoretical recognition that the Strait of Hormuz represented an existential risk, the international community made no serious collective effort to develop alternative export infrastructure sufficient to route a meaningful share of Gulf oil and gas through alternative corridors.

The existing alternative routes — principally the Saudi Petroline pipeline across the Arabian Peninsula and the Abu Dhabi Crude Oil Pipeline — handle only approximately one third of the volume that normally passes through the strait, leaving the other two thirds with no viable alternative export pathway.

This infrastructure deficit is not an accident: the economics of pipeline construction at the necessary scale, combined with the political complexity of routing pipelines through sovereign territories with competing interests, made the development of genuine redundancy impractical in the commercial environment of the past four decades.

The second structural cause is the design of global oil futures markets and their interaction with geopolitical risk.

As JP Morgan analysts observed, markets were "transitioning from assessing pure geopolitical risk to confronting actual operational disruptions, as refinery shutdowns and export limitations begin to hinder crude processing and supply flows in the region."

The speed with which Brent crude moved from $73 per barrel to nearly $120 in fewer than ten days reflects not only the severity of the physical supply disruption but also the accumulated underpricing of Hormuz risk that had persisted for years.

BloombergNEF, writing in January 2026 before hostilities began, estimated only a $4 per barrel "war premium" built into crude prices at that point — a figure that proved spectacularly inadequate as events unfolded.

The proximate political cause of the crisis is the decision by the Trump administration to pursue military action against Iran without adequate planning for the energy market consequences.

Trump's initial dismissal of rising gas prices — "if they rise, they rise" — reflects an assumption, ultimately proven incorrect, that the military campaign would be sufficiently swift to prevent sustained energy market disruption.

This mirrors the administration's experience with tariffs in spring 2025: in both cases, a policy of maximum pressure was pursued without a realistic model of the second and third-order economic consequences, and in both cases, the political and economic feedback effects forced a rapid reversal of posture.

The pattern reveals a recurring structural weakness in the administration's approach to economic statecraft: a tendency to treat market pain as a manageable and temporary cost of geopolitical assertion, rather than as a constraining variable that shapes the ultimate viability of the policy itself.

The effect structure is equally complex.

The most immediate effect — crude price escalation and LNG supply disruption — has propagated rapidly into downstream inflation across global economies.

For oil-importing economies in Asia, the effect is a direct and severe terms-of-trade shock, forcing central banks to choose between raising interest rates to combat inflation and cutting them to sustain growth under conditions of energy-induced slowdown — the classic stagflationary trap.

For Gulf oil-producing states, paradoxically, the effect is also damaging: Saudi Arabia, the UAE, Kuwait, and Iraq are losing export revenue not because their oil lacks buyers but because their ships cannot safely sail.

The Saudi Ras Tanura refinery attack, combined with forced production cuts, represents a direct economic wound to the kingdom whose entire fiscal architecture depends on energy export revenue.

For the United States, the effect is felt through gasoline prices that directly contradict the central economic narrative of the administration, threatening Republican prospects in the November 2026 midterm elections.

Future Steps: The Road Through and Beyond the Crisis

Asia, Europe, and the Gulf in Crisis: Who Bears the Greatest Pain From the Hormuz Blockade

The trajectory of the Hormuz crisis will be determined by a narrow set of variables whose resolution will shape the global energy order for years or decades.

In the immediate term, the central question is whether a ceasefire between the United States and Iran can be established quickly enough to prevent the physical closure of the strait from metastasizing into a structural supply deficit that inflicts lasting damage on global growth.

If a ceasefire is reached and verified in the coming days or weeks, energy flows could resume — at least partially — as tankers cautiously return to the corridor and maritime insurers begin to re-extend coverage.

Even under this relatively optimistic scenario, the supply chain disruptions, refinery closures, storage overfills, and infrastructure damage already sustained will produce elevated commodity prices for months, as suppliers manage compromised facilities and disrupted logistics.

The medium-term structural implications are more consequential and more permanent.

The Hormuz crisis has demonstrated, with brutal empirical clarity, that the global energy system's dependence on a single 20.5 Mile chokepoint is not merely a theoretical vulnerability but a practical catastrophe risk.

The political and investment incentives to develop genuine alternative export infrastructure — expanded pipeline capacity, enhanced emergency stockpile coordination, accelerated development of non-Gulf renewable and nuclear generation capacity — will intensify sharply in the aftermath of this crisis.

Saudi Arabia will face renewed urgency to expand its East-West Pipeline capacity; the UAE to develop its Abu Dhabi Crude Oil Pipeline toward its full theoretical capacity; and importing nations in Asia and Europe to accelerate both energy diversification and strategic reserve deepening.

The geopolitical realignment triggered by the crisis carries its own long-term energy implications.

The White House's decision to temporarily lift sanctions on Russian oil exports to compensate for Gulf supply losses represents a significant and potentially difficult-to-reverse concession to Moscow at a moment of European vulnerability.

If Russian oil flows are restored to a degree sufficient to compensate partially for Gulf losses, Russia emerges from the Hormuz crisis as a strategic beneficiary — strengthening its position in global energy markets at a moment when Western policy had been directed toward its isolation.

China, which depends on Gulf oil for nearly 46% of its imports, will draw its own conclusions from the crisis, accelerating investment in alternative supply sources, strategic reserve capacity, and the geopolitical relationships — including with Russia — that provide energy security outside the reach of US military power projection.

The long-term implication for US credibility as the guarantor of Gulf energy security is profound. For nearly four decades, the American military presence in the Gulf — particularly the Fifth Fleet — was understood as the structural guarantee of Hormuz's openness.

The 2026 crisis has demonstrated that even a direct US military campaign against Iran, the primary threat to that corridor, is not sufficient to maintain free maritime passage when Iran chooses to contest it through asymmetric means.

The doctrine of American-guaranteed Gulf energy security, a cornerstone of the post-1980 strategic order, has been severely tested.

Whether it can be reconstituted, and on what institutional and diplomatic basis, is among the most important questions facing international energy and security policy in the coming years.

Conclusion: A Before and After Moment in the History of Energy Markets

Beyond the Battlefield: How the US-Iran Conflict Is Reshaping Global Energy Architecture Forever

The Strait of Hormuz crisis of 2026 is not a temporary disruption in an otherwise stable energy landscape.

It is a structural rupture that has exposed the fragility of a global energy architecture built on decades of accumulated assumptions — about American deterrence, about the reliability of Gulf supply, about the adequacy of existing alternative infrastructure, and about the capacity of financial markets to price geopolitical tail risk accurately.

The world before February 28th, 2026, operated on the assumption that the strait was functionally inviolable, protected by the weight of American military power and the overwhelming mutual interest in maintaining the flow of Gulf energy.

The world after March 2026 knows that this assumption was dangerously incomplete. Iran demonstrated, with a fleet of drones and a doctrine of asymmetric maritime warfare, that a determined regional state can effectively close the world's most critical energy chokepoint even in the face of a direct US military campaign.

The political economy of the crisis is equally instructive.

Trump's trajectory — from dismissing the economic consequences of war to signalling a rapid conclusion, then reversing again under market pressure — mirrors the pattern of his retreat from the trade war of spring 2025. In both cases, the structural reality of economic feedback constrained the exercise of political will.

This pattern suggests not merely the particular vulnerabilities of one administration but a broader truth about the structural limits on the exercise of geopolitical power in an era of deeply interdependent global markets.

States that use economic and military coercion as instruments of strategic competition discover, often at great cost, that the markets they seek to discipline have the capacity to discipline them in return.

The Hormuz crisis of 2026 is, in this sense, a case study in the inescapable constraints that economic interdependence places on state power — and a warning, for all stakeholders in the global energy system, that the infrastructure of that system is far more fragile than the reassuring assumptions of recent decades have led them to believe.