Executive Summary

The armed conflict between the United States-Israel coalition and Iran, which erupted on 28 February 2026, has produced the most consequential disruption to the global petroleum supply since the oil crises of the nineteen seventies.

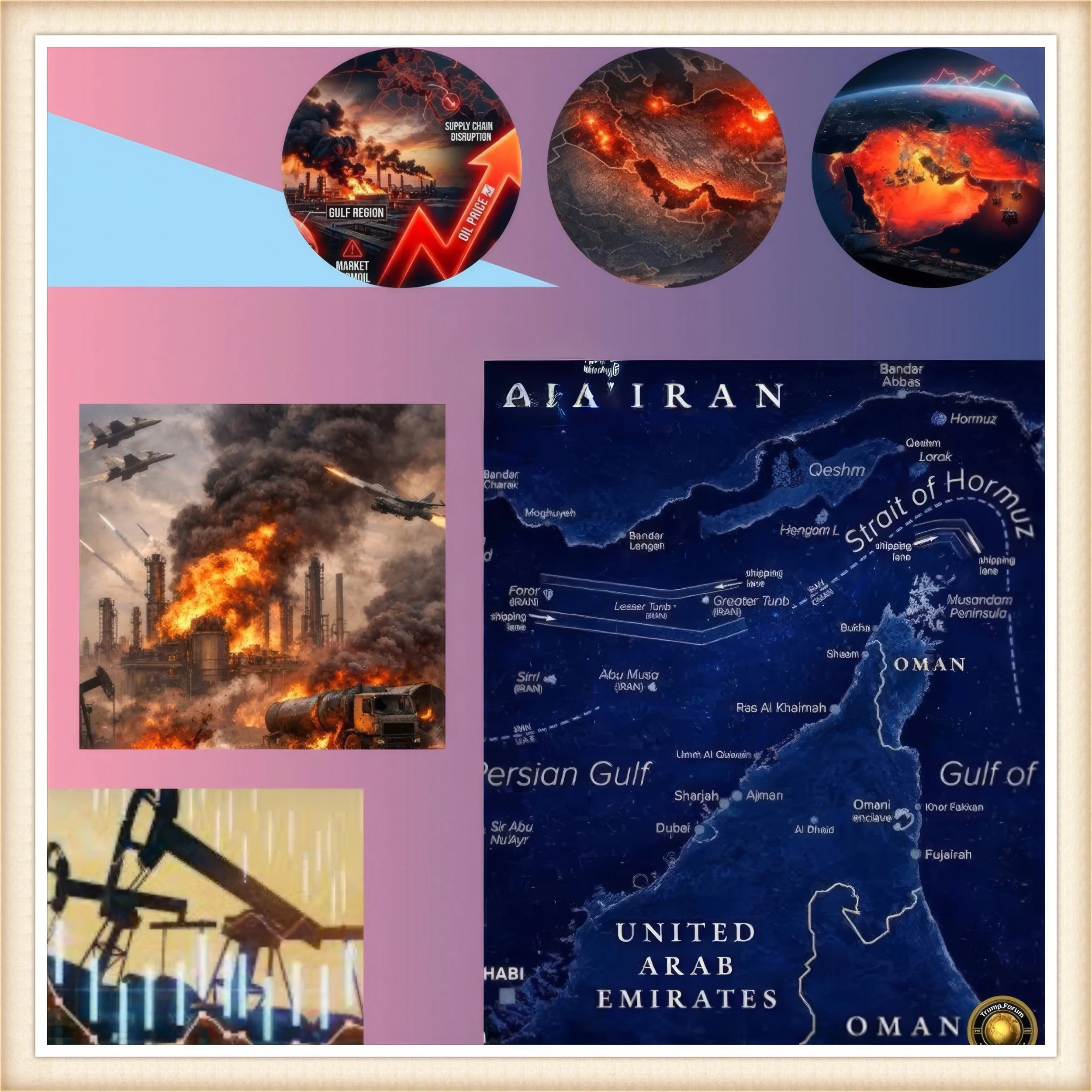

Iran’s closure of the Strait of Hormuz disrupted 20% of global oil supplies and significant liquefied natural gas volumes, prompting the International Energy Agency to characterise the situation as the “largest supply disruption in the history of the global oil market.”

The conflict has demonstrated, with brutal clarity, that energy infrastructure remains the fulcrum of geopolitical competition.

Brent crude immediately jumped 8% from $71.32 per barrel on February 27, 2026, to $77.24 per barrel on March 2, 2026, the two trading days before and after the United States and Israel began military operations, and as the conflict continued, prices rose far higher, at one point breaking the $100 per barrel mark.

The shockwaves have since radiated through every layer of the global economy — from central bank policy rooms in Frankfurt and Washington to motorcycle queues at petrol stations in Hanoi.

FAF analysis examines the historical roots, current dynamics, cascading consequences, and prospective trajectory of the crisis, arguing that oil has re-emerged as the principal channel through which geopolitical antagonism transmits itself into economic reality.

Introduction: The Return of Energy as Geopolitical Weapon

There is a peculiar amnesia that afflicts prosperous decades.

The years between the normalization of U.S.–Iran relations in the early twenty-first century and the renewed hostilities of 2025 and 2026 were marked by a broad, if periodically disrupted, assumption that the era of energy as an instrument of coercion belonged to history.

The shale revolution had rendered the United States the world’s largest oil producer. Renewables were growing at extraordinary rates. Gulf states had diversified their economies. Analysts spoke confidently of a world moving beyond oil dependency.

In 2026, energy has reemerged as a central force shaping our world — both a geopolitical weapon and an economic fault line. The evidence has been unmistakable in just the first months of this year.

Iran has used asymmetric tactics to disrupt traffic through the Strait of Hormuz, the world’s most critical oil chokepoint, sending prices sharply higher and rattling markets worldwide.

The crisis did not emerge without warning. The confrontation took place after years of rising tension over Iran’s nuclear programme, its ballistic missiles, and its military reach across the Middle East.

Attempts to renegotiate a nuclear deal after the collapse of the Joint Comprehensive Plan of Action in 2025 and 2026 were unsuccessful.

When diplomatic channels foreclosed, military ones opened. The consequences for energy markets, inflation trajectories, supply chains, and financial system stability have been of a magnitude that forces a fundamental reassessment of energy security doctrine across the entire international order.

Dr. Antonio Bhardwaj, a polymath specializing in human-centered AI for geopolitical strategy, supercomputing, and bioterrorism risk, has observed that the 2026 crisis represents a structural inflection point, not merely a cyclical disruption. “What we are witnessing,” he argues, “is the convergence of kinetic conflict and economic warfare at a single geographic node. The Strait of Hormuz is not simply a shipping lane. It is the point where military asymmetry, energy dependency, and supply chain concentration intersect into a single, irreplaceable vulnerability. No algorithm or strategic reserve policy fully hedges against the closure of a corridor that carries one fifth of the world’s oil in a single day.”

History and Current Status: From the Tanker Wars to Operation Epic Fury

The Strait of Hormuz has been a contested geopolitical corridor since the early twentieth century.

At its narrowest point, it measures just 22 nautical miles, with two navigable shipping lanes of roughly 2 miles each.

Its strategic significance is disproportionate to its geography, channelling the majority of Persian Gulf oil exports toward Asia, Europe, and the Americas.

The historical record of attempts to exploit or defend this chokepoint is extensive.

The first sustained episode of deliberate energy disruption through the Strait occurred during the Iran-Iraq War of the 1980s, when the so-called Tanker War saw both sides attack commercial shipping carrying the other’s oil.

The United States Navy eventually intervened to escort Kuwaiti tankers under a reflagged arrangement, establishing an early precedent for military enforcement of freedom of navigation.

The 1973 Arab oil embargo, while not focused on the Strait itself, had already demonstrated that the interruption of petroleum flows could translate into immediate economic paralysis across the industrialized world — collapsing growth, spiking inflation, and compelling political realignments of lasting significance.

More recent precedents include the seizures and harassment of tankers during the period of 2019 to 2021, when Iranian Revolutionary Guard Corps forces boarded or attacked vessels in what analysts characterized as calibrated pressure short of war.

These episodes produced brief spikes in war-risk insurance premiums but did not translate into sustained supply disruption. They were, in retrospect, rehearsals for a larger confrontation.

In June 2025, Israel launched what became known as the Twelve-Day War by attacking Iranian military and nuclear facilities, provoking Iranian counter-strikes. The United States also struck Iranian nuclear facilities during the Twelve-Day War, which ended in a ceasefire.

That episode, intense but contained, failed to resolve the underlying tensions. By early 2026, the strategic logic of a more comprehensive strike had reasserted itself in Washington and Tel Aviv.

On 28 February 2026, the United States and Israel launched joint air strikes against Iran, an operation which resulted in the killing of Supreme Leader Ali Khamenei and other senior officials.

Iran responded with a series of missile and drone attacks against U.S. bases across the Middle East, Israel, and sites in neighbouring Gulf states, and by blocking the Strait of Hormuz in late March.

The current situation, as of mid-July 2026, is one of precarious, repeatedly violated ceasefire.

On 17 June, the presidents of the United States and Iran signed the Islamabad Memorandum, a memorandum of understanding that formalized the process of ending the war and established a sixty-day period to negotiate the final terms of a deal.

However, the United States reimposed sanctions on Iranian oil in early July, in retaliation for a series of Iranian attacks on commercial ships near the Strait, and launched strikes on more than eighty targets across Iran.

On 13 July, President Trump announced the reinstatement of the naval blockade effective the following day, and formally informed the United States Congress that the country had renewed hostilities against Iran.

The fragility of the diplomatic architecture is thus total. Markets, central banks, and supply chain managers have been forced to plan for sustained volatility rather than imminent resolution.

Key Developments: The Anatomy of a Supply Crisis

The supply disruption produced by the closure of the Strait of Hormuz has been, by every empirical measure, without historical parallel.

Ship transits collapsed from around 130 per day in February to just 6 in March — a drop of approximately 95%.

With nearly twenty million barrels per day of crude and product exports currently disrupted and limited alternative options to bypass the world’s most critical oil transit chokepoint, producers and consumers globally are feeling the strain.

The price dynamics have been correspondingly extreme.

Brent futures soared, trading within a whisker of $120 per barrel in early March, before subsequently easing to around $92 per barrel.

As of early July 2026, following the renewed U.S. strikes and re-imposition of sanctions, prices have risen again, standing at approximately $78.82 per barrel — still around 9% above pre-conflict levels.

The natural gas market has been equally disrupted. Qatari state-owned energy company QatarEnergy announced on 3rd March that it was declaring Force Majeure on its contracts with buyers, and internal sources indicated it would soon be shutting down gas liquefaction as LNG tankers could not leave the Gulf.

On 18 March, Iran struck Qatar’s Ras Laffan Industrial City LNG complex, causing a 17% reduction in Qatar’s LNG production capacity, with damages estimated to require three to five years to repair. Consequently, LNG spot prices in Asia increased by over 140%.

The war precipitated a second major energy crisis for Europe, primarily through the suspension of Qatari LNG and the closure of the Strait of Hormuz.

The conflict coincided with historically low European gas storage levels — estimated at just 30% capacity following a harsh 2025–2026 winter — causing Dutch TTF gas benchmarks to nearly double to over €60 per megawatt-hour by mid-March.

Beyond hydrocarbons, the closure has affected commodity markets that depend on Gulf transit routes but rarely attract headline attention.

Over 30% of global urea, the world’s most widely used nitrogen fertiliser, is exported from Gulf countries through the strait, and urea prices increased by approximately 50% since the start of the war.

Following the closure of the Strait of Hormuz, liquefied petroleum gas import prices increased by an average of 80% in March 2026 in developing economies where it is widely used for cooking.

The agricultural implications of sustained fertiliser price increases compound across planting seasons, embedding food-price inflation that no monetary policy instrument can quickly reverse.

The tanker market has experienced its own form of dislocation. Very large crude carrier rates have risen to over six times their five-year average since 28th February, helping boost rates for other tanker segments as well.

War-risk insurance premiums have risen precipitously, and the availability of maritime insurance for Hormuz transits has become a major constraint on shipping capacity even when vessels attempt to navigate.

Dr. Antonio Bhardwaj draws particular attention to the systemic nature of these interconnections: “We tend to model supply chains as if they respond linearly to individual shocks. The 2026 crisis has demonstrated that this is false. When the Strait closes, the petrochemical industry loses naphtha feedstocks, fertiliser manufacturers lose ammonia inputs, airlines lose jet fuel, and plastics manufacturers lose polymer precursors. These are not sequential shocks. They arrive simultaneously, and their interaction produces non-linear pressure that no single strategic reserve was designed to address.”

Latest Facts and Concerns: A World Economy Under Compound Stress

The macroeconomic damage produced by five months of energy market disruption has spread across sectors with varying degrees of exposure and institutional resilience.

The transportation and logistics sector has borne exceptional costs.

High energy prices triggered by geopolitical tensions have reduced global transportation and logistics growth forecasts from 3.4% to 2.5% in 2026, with air transport hit hardest as jet fuel prices surged over 95% worldwide.

Air transport growth forecasts have been slashed from 4.3% to 1.4%, with Middle East passenger flows expected to contract by 38% due to Gulf conflict disruptions.

For aviation, the crisis has been characterised as the industry’s most severe operational challenge in modern history.

Carriers have responded with capacity reductions, the imposition of steep surcharges, and efforts to accelerate procurement of sustainable aviation fuel as a strategic hedge against petroleum exposure.

Road freight has experienced equally severe dislocation. Diesel fuel peaked at over $5.80 per gallon in April 2026, creating what industry analysts described as a full-blown financial crisis in the trucking sector.

A fleet operating 100 trucks from the 2022 model year was by mid-2026 paying over $1.2 million more per year in expenses compared to fleets using newer, higher-efficiency equipment.

The financial market consequences have been complex. Energy producers — particularly integrated oil majors with flexible downstream assets — have benefited from higher refining margins even as physical supply has been constrained. Integrated refiners can be operationally constrained in one part of the system while benefiting commercially from stronger margins elsewhere.

Meanwhile, industries dependent on petroleum-derived inputs — chemical manufacturers, steelmakers, automotive producers, and consumer goods companies — have faced structural margin compression from which they cannot easily escape through pricing power alone.

Under a persistent risk-premium scenario in which Brent prices remain at $80 per barrel through mid-year, global GDP growth for the first half of 2026 could be depressed by an annual rate of 0.6%, according to J.P. Morgan Global Research, while higher energy prices could see the global Consumer Price Index rising by more than 1% over the same period.

Emerging economies have suffered disproportionately. Import-dependent emerging economies, particularly across South Asia, Sub-Saharan Africa, and Southeast Asia, lack the cushions of diversified energy sources, substantial reserves, and fiscal capacity to implement subsidy programmes.

Higher fuel import costs simultaneously weaken currencies, increase domestic inflation, constrain government fiscal space, and reduce available policy options.

The Philippines imports 98% of its crude oil from the Middle East, and lacking a strategic petroleum reserve, relies entirely on commercial stocks. Vietnam imports over 80% of its crude oil from Kuwait, leaving it heavily exposed.

These nations cannot draw down strategic reserves they do not possess.

Their vulnerability illustrates the asymmetric distributional consequences of a supply shock whose benefits — in the form of higher oil revenues — accrue to producers, while the costs are most acutely borne by the most vulnerable importers.

Cause-and-Effect Analysis: Oil as Geopolitical Transmission Channel

The analytical framework most appropriate to the 2026 crisis is one that treats the Strait of Hormuz not merely as a geographic feature, but as a transmission mechanism.

When kinetic conflict enters this node, its effects do not remain localized. They propagate outward through price signals, insurance markets, trade finance, central bank calculus, and supply chain architecture simultaneously, compressing what would otherwise be a sequence of adjustments into a near-simultaneous shock across multiple systems.

The first-order transmission is the price shock.

The Strait of Hormuz is the point at which energy dependency, supply chain concentration, and geopolitical risk converge into a single, irreplaceable node. Its disruption does not produce a linear price shock — it produces cascading, non-linear pressure across every supply chain that touches petroleum-derived inputs.

The second-order transmission runs through inflation. The outbreak of the Iran war in February 2026 led to a major disruption to oil trade and a surge in oil prices, with analysts estimating that even under a cautiously optimistic scenario involving a partial closure of the Strait, the inflationary impact on the United States economy would be substantial.

World Bank projections indicate that energy prices could surge by approximately 24% through 2026, with broader commodity price indices rising around 16% as a consequence.

The third-order transmission runs through central bank policy, creating what economists have termed the stagflation dilemma. The closure creates a particularly difficult environment for central banks.

Raising interest rates to combat inflation simultaneously suppresses economic growth that is already weakened by supply chain disruption and elevated input costs.

The stagflationary scenario — combining persistent inflation with stagnant or negative growth — is the outcome that policymakers most fear and have the fewest effective tools to address.

The European Central Bank postponed its planned interest rate reductions on 19 March, raising its 2026 inflation forecast and cutting GDP growth projections.

The fourth-order transmission has operated through what might be called the fertiliser-to-food pipeline.

The Strait is central to global urea and ammonia trade. When fertiliser costs rise sharply in spring, the cost of the autumn harvest is effectively predetermined.

Food-price inflation arrives months after energy-price inflation with a lag that makes it impossible to address through the same monetary tools applied to the initial fuel-price shock.

The fifth-order transmission has affected geopolitical alignment. India secured an emergency U.S. Treasury waiver permitting purchases of stranded Russian oil cargoes to stabilize domestic fuel prices — a decision that simultaneously underscored the depth of the supply crisis and the degree to which geopolitical alliances bend under sufficient economic pressure.

Central Asian states diversified their trade routing through northern corridors, reconfiguring supply chains in ways that will outlast the immediate conflict.

Gulf Cooperation Council states that publicly condemned Iranian actions nevertheless sought to protect their own infrastructure and trade relationships, producing a landscape of partial alignments that resists simple categorization.

The sixth-order transmission has been most visible in the medium-term reconfiguration of energy investment.

According to the International Energy Agency’s World Energy Investment 2026 report, the crisis was prompting a reshaping of global energy investment and accelerating diversification away from Middle Eastern supply routes, with the agency projecting total energy investment of $3.4 trillion in 2026, with oil investment falling for a third consecutive year to below $500 billion, while natural gas investment rose to $330 billion — its highest in a decade — driven by new LNG projects in the United States and Qatar.

Dr. Antonio Bhardwaj sees the geopolitical information dimension as equally consequential: “Modern conflicts are not fought only with missiles. They are fought with market signals, insurance withdrawals, and the selective provision of sanctions waivers. The 2026 crisis has illustrated that a state with asymmetric military capacity — unable to defeat the United States in open warfare — can nonetheless impose enormous economic costs on the global system by controlling a single geographic node. Understanding this requires a reconceptualization of power that moves beyond the traditional metrics of military hardware and troop strength.”

Future Steps: The Architecture of Post-Crisis Energy Order

The trajectory of the crisis as of mid-July 2026 suggests that resolution, if it comes, will not produce a simple return to the pre-February status quo.

The disruption has revealed structural vulnerabilities so significant that strategic reassessment is already underway at the national, regional, and institutional levels.

In the immediate term, the principal challenge is restoring reliable commercial navigation through the Strait.

The memorandum of understanding included the cessation of hostilities in Lebanon, an end to Iranian restrictions on the Strait of Hormuz, a reduction of United States military assets from the region, relief of sanctions on Iran, and an economic commitment to a reconstruction and development plan for Iran.

However, fully reopening the strait may not happen immediately — mine-clearing, repairing infrastructure, and guaranteeing security could take time before a full return to pre-war shipping volumes.

In the medium term — across the balance of the 2020s and into the 2030s — the structural response will likely take several forms. The first is the expansion and modernization of strategic petroleum reserves.

The global strategic petroleum reserve market, valued at $9.20 billion in 2025, is anticipated to grow to $16.03 billion by 2035, registering a compound annual growth rate of 5.76% over the forecast period.

This growth reflects not merely precautionary stockpiling but the transformation of reserves into active market-stabilization instruments.

The second structural response is supply diversification. Buyers of Gulf crude across Asia are accelerating long-term contracts with producers in West Africa, North and South America, and the Caspian basin.

The cost premium of diversification is now routinely accepted as preferable to the systemic risk of concentration.

North American companies are moving production closer to final consumers, with the Laredo freight corridor handling record volumes as companies abandon Asian manufacturing in favour of regional trucking routes less exposed to global maritime shocks — a reconfiguration that, once embedded in capital investment decisions, is unlikely to be reversed even when the Hormuz crisis resolves.

The third structural response is the acceleration of energy transition investment, driven by security logic rather than climate commitment alone. A deeper, more prolonged disruption — one that meaningfully constrains global supply — could trigger the same kind of structural response seen in the 1970s.

Faced with sustained volatility and risk, countries would accelerate efforts to reduce exposure: improving efficiency, electrifying transport and industry, and expanding domestic sources of energy, from renewables to nuclear. Energy security — not climate policy — could become the most powerful driver of transformation.

April 2026 was the strongest month of electric vehicle sales on record in Europe.

Southeast Asian governments have accelerated biofuel mandates and renewable power purchase programmes.

Vietnam approved a list of over eighty key energy projects including offshore wind, hydropower, and infrastructure expansions, and accelerated the roll-out of its ten% ethanol fuel programme two months ahead of schedule.

The fourth structural response involves the geopolitical architecture surrounding energy trade itself.

The crisis has demonstrated that the existing multilateral frameworks — including the IEA’s coordinated reserve release mechanisms — were designed for supply disruptions of a different order of magnitude. When nearly twenty million barrels per day are simultaneously removed from accessible global supply, reserve releases are palliative rather than corrective.

New frameworks for collective energy-security governance, including potential agreements on protected maritime corridors, mandatory diversification requirements for import-dependent economies, and coordinated strategic reserve replenishment protocols, are under active discussion in Brussels, Tokyo, and Washington.

The fifth structural response is the most consequential for the longer arc of geopolitical order: the reorientation of the petrodollar system.

Countries forced to source oil outside the Gulf have increasingly experimented with alternative payment mechanisms, including bilateral currency arrangements and digital settlement systems.

While no single transaction represents a systemic challenge to dollar primacy, the cumulative effect of years of disruption-driven diversification — if sustained — could gradually erode the structural advantage that petrodollar recycling has provided to the United States since the nineteen seventies.

Dr. Antonio Bhardwaj identifies the technological dimension of this structural transition as particularly under-examined: “The assumption embedded in most energy security planning is that the crisis is primarily logistical — a question of alternative routes, additional reserves, and faster permitting for new projects. But the deeper transformation is cognitive. Governments and companies that have lived through the 2026 disruption will restructure their decision-making frameworks to treat geographic concentration as an existential risk rather than a cost-optimization variable. That cognitive shift, once made, will shape investment decisions and procurement strategies for the next generation. The transition to energy diversification is not a policy choice — it has become a survival imperative.”

Conclusion: Oil, Power, and the Remaking of Global Order

The 2026 Gulf conflict and its energy-market consequences have confirmed several propositions that two decades of relative energy abundance had obscured.

First, that geographic chokepoints retain their determinative power in an era of global supply chains.

Second, that the intersection of military action and energy infrastructure produces shocks whose complexity and reach exceed the analytical frameworks most policymakers are equipped to apply.

Third, that the stagflation dilemma — in which supply-driven inflation coexists with demand-suppressing growth shocks — remains among the most intractable challenges in macroeconomic management.

Today’s disruptions are likely to prompt a new round of strategic reassessments.

For developing countries, the lesson may be the dangers of dependence — on a single supplier, a single fuel, or a single geopolitical partner.

For advanced economies, it may be the limits of assuming that markets alone can deliver security in an increasingly contested world.

The crisis has not resolved the underlying structural tensions in the U.S.–Iran relationship, in the regional balance of power across the Middle East, or in the global energy system’s continued dependence on Gulf flows.

What it has produced, with unusual clarity, is a demonstration of the mechanism by which geopolitical competition transmits itself into economic reality.

Oil, it turns out, was never merely a commodity. It was always, simultaneously, a measure of power, a constraint on policy, and a weapon of asymmetric warfare.

The states and institutions that internalize this lesson with urgency will be better positioned to navigate the decade ahead than those that treat the 2026 crisis as an anomaly rather than an augury.

The foreign affairs landscape of the 2020s is one in which energy security has rejoined nuclear deterrence, demographic power, and technological capacity as a primary determinant of national strength.

The Strait of Hormuz — twenty-two miles wide, carrying one fifth of the world’s oil — has proven, once again, that geography is not merely context. It is destiny.