Cheap Drones, Expensive Ambitions: How Asymmetric Warfare Is Reshaping the Gulf's Artificial Intelligence Order

Executive Summary

The war involving the United States, Israel, and Iran, which escalated dramatically in early 2026, has transformed the strategic calculus governing one of the most consequential infrastructure buildouts of the twenty-first century.

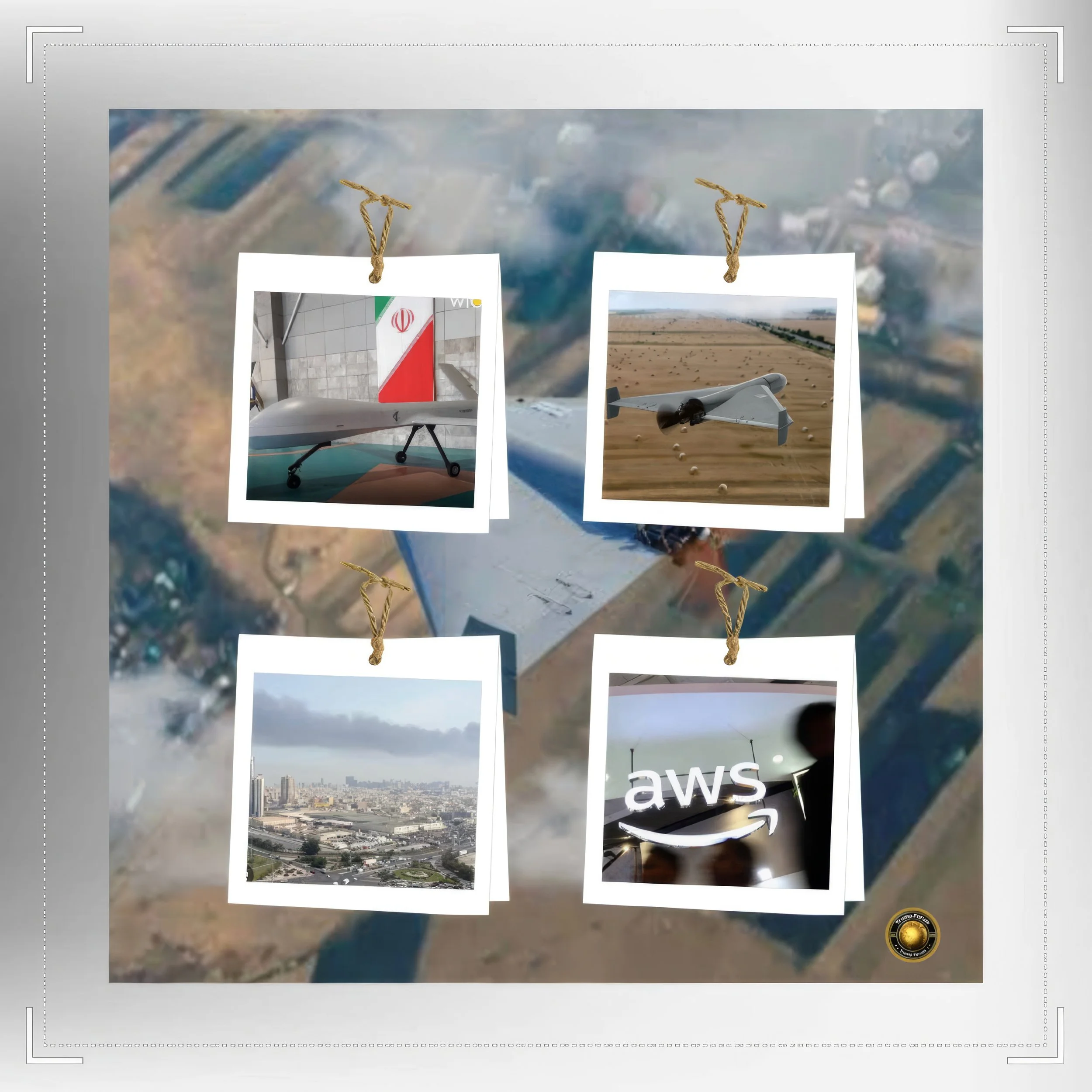

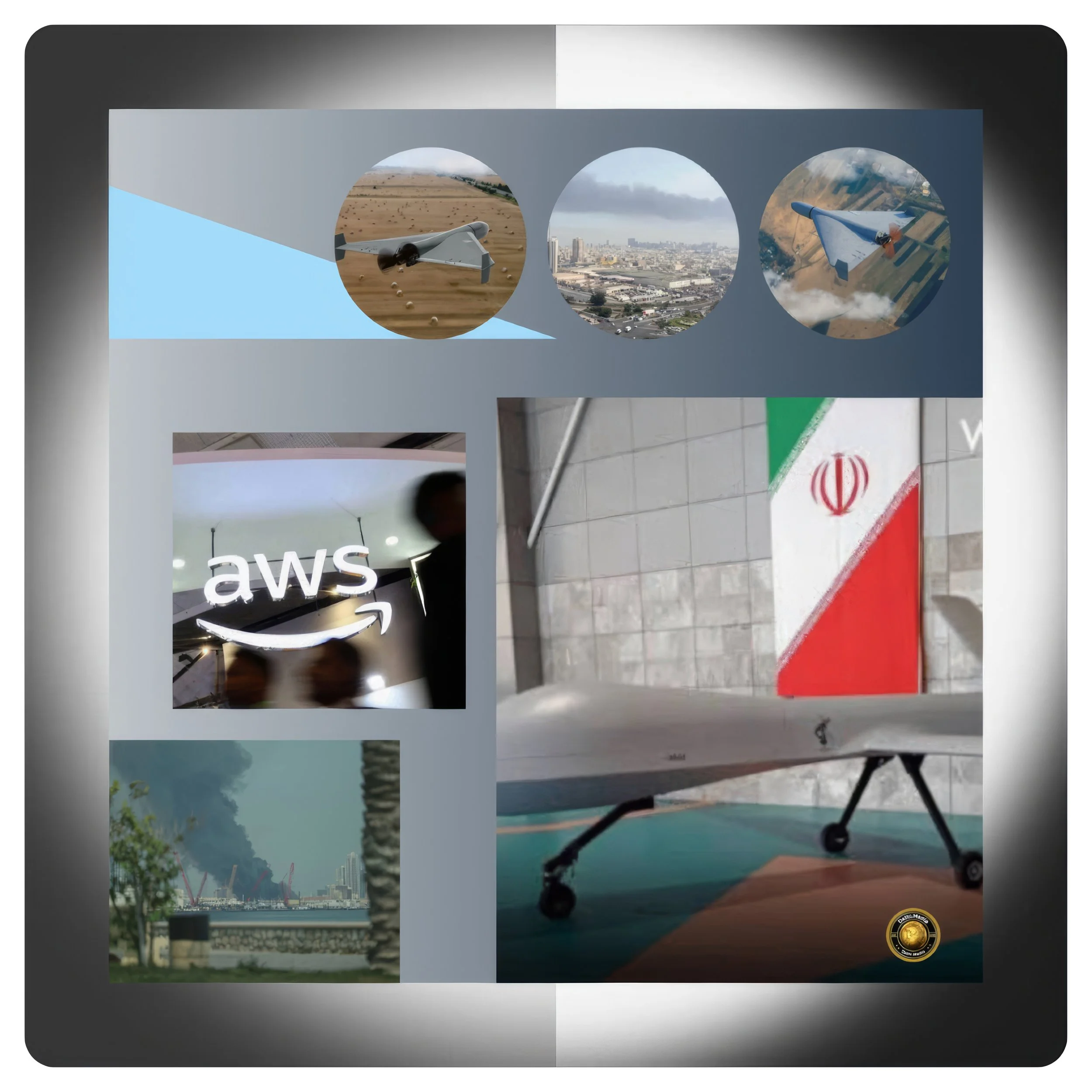

On March 1st, 2026, drone strikes attributed to Iranian-aligned forces struck three Amazon Web Services facilities — two in the United Arab Emirates and one in Bahrain — causing sweeping disruptions to cloud services across the Gulf region.

The Islamic Revolutionary Guard Corps subsequently published a target list of 29 technology assets spread across Bahrain, Qatar, and the UAE, naming facilities associated with AWS, Microsoft, Google, Nvidia, IBM, Oracle, and Palantir.

These events arrived in the middle of a $700 billion-plus regional buildout of AI data centers underwritten by sovereign wealth capital, American technology transfer, and a shared geopolitical vision.

The attacks did not terminate Gulf AI ambitions, but they permanently altered their character.

Protection has become inseparable from access, and future AI infrastructure deals will be bundled with defense cooperation agreements, tighter security conditions, and explicit political alignment with Washington.

The securitization of AI is no longer a distant possibility — it is the present reality.

Introduction

When Infrastructure Became a Battlefield

The dominant narrative surrounding the Gulf's emergence as a global AI infrastructure hub has, until recently, rested on a set of assumptions so widely shared as to seem self-evident.

Gulf states possess the sovereign capital, the surplus energy, the available land, and the political stability to host hyperscale data centers on a scale that rivals or exceeds comparable deployments in Western Europe.

American technology companies need these assets to expand cloud and AI capacity beyond the increasingly constrained domestic regulatory and environmental environment.

Washington needs the Gulf inside a U.S.-aligned AI ecosystem to deny China the strategic advantage of regional AI dominance.

These three interests aligned in a configuration that produced one of the most concentrated waves of technology infrastructure investment in recent history.

Microsoft committed $15.2 billion to the UAE across the period 2023 through 2029, including equity investment in G42, data center capital expenditure, and local operating expenses.

Saudi Arabia's NEOM signed a $5 billion agreement with DataVolt for a 1.5-gigawatt AI factory, while Groq announced a $1.5 billion investment in Saudi Arabia in partnership with Aramco Digital to build what may become the world's largest AI inference data center.

The UAE unveiled a 5-gigawatt AI campus, the largest such facility outside the United States, spanning 10 square miles and reflecting a $44 billion investment pipeline.

The Middle East and Africa data center market was projected to grow at an 11.7% compound annual growth rate from 2025 to 2030, with Gulf states accounting for the dominant share of that expansion.

Into this landscape of capital abundance and strategic ambition arrived, on March 1st, 2026, a wave of drones carrying modest payloads and costing, per unit, somewhere in the low tens of thousands of dollars.

The targets were not oil fields or military bases. They were server rooms.

The conflict that produced them was the direct consequence of coordinated U.S.-Israeli strikes on Iran that resulted in the death of Supreme Leader Ayatollah Ali Khamenei in late February 2026, triggering a wave of Iranian retaliatory operations across the Gulf.

The proposition that hyperscale commercial cloud infrastructure could be treated as a neutral, insulated asset class was, in a matter of hours, permanently falsified.

History and Current Status

The Gulf's AI Bargain and Its Origins

To understand what the drone strikes of March 2026 have changed, it is necessary to understand what they interrupted.

The Gulf's AI infrastructure boom did not emerge spontaneously.

It was the product of a decade of deliberate economic planning in Riyadh, Abu Dhabi, and Doha, accelerated by the growing urgency of post-oil economic transition and validated by Washington's strategic interest in keeping the Gulf's technology ecosystem anchored to U.S. platforms.

Saudi Arabia's Vision 2030 program, launched in 2016, set the broad ambition of diversifying the Kingdom away from hydrocarbon dependence by building competitive industries in tourism, manufacturing, entertainment, and increasingly, technology.

The establishment of HUMAIN, Saudi Arabia's national AI champion, in early 2025 marked the institutional crystallization of this ambition.

HUMAIN announced a strategic partnership with the Blackstone-backed data center operator AirTrunk to build AI data centers in Saudi Arabia, with a planned investment of $3 billion across the coming years.

Saudi Arabia's Public Investment Fund signed a $2.7 billion contract with Hexagon for a 480-megawatt AI compute facility in Riyadh, described as the largest single AI infrastructure deal in GCC history.

The Saudi LEAP technology conference in early 2025 exceeded $20 billion in investment commitments from a single event.

The UAE pursued a parallel but distinct trajectory.

G42, Abu Dhabi's state-backed AI and cloud conglomerate, became the vehicle through which Microsoft's $15.2 billion commitment was channeled, with G42 agreeing to divest from Chinese hardware suppliers as a condition of accessing U.S. chips and investment.

The UAE's willingness to accommodate U.S. security concerns on this front established a template for the broader relationship — technology access in exchange for geopolitical alignment.

A preliminary agreement to export approximately 500,000 advanced Nvidia chips annually to the UAE builds on Washington's broader strategy of promoting U.S.-made AI systems globally.

The U.S.-UAE $1.4 trillion technology investment framework, agreed in March 2025, formalized this relationship at the highest levels of bilateral engagement.

The strategic logic from Washington's perspective was articulated explicitly in the Trump administration's AI Action Plan, which identified international AI diplomacy and security as one of its three central pillars, and signaled a significant expansion of AI exports to U.S. allies and partners as part of the effort to win what the White House described as the "race to achieve global dominance in artificial intelligence."

In this framework, the Gulf's sovereign wealth capital and its energy surplus were not merely commercial attractions — they were strategic assets that Washington sought to lock into a U.S.-aligned ecosystem before Beijing could deepen its own regional footprint.

This was the architecture of the Gulf AI bargain before March 2026: Gulf states would provide capital, land, energy, and political alignment; American technology companies would provide chips, software, and cloud infrastructure; and the United States government would provide the strategic umbrella that made the enterprise viable.

That bargain was not destroyed by the drone strikes. It was renegotiated by them, under conditions that favor the security state over the commercial enterprise.

Key Developments

From Commercial Asset to Military Target

The sequence of events that transformed Gulf AI infrastructure from a commercial asset class into a recognized military target unfolded with startling speed.

On the weekend of February 28th, 2026, the United States and Israel executed coordinated strikes on Iranian territory, killing Supreme Leader Khamenei and dismantling significant elements of Iran's nuclear and missile infrastructure.

Iran's response was immediate and multi-dimensional.

Within hours, the Islamic Republic launched what would become a sustained campaign of ballistic missile, cruise missile, and drone attacks across the Gulf, directed at both military and economic targets.

The UAE bore the heaviest initial burden.

As of April 9th, 2026, the UAE had intercepted and destroyed 537 ballistic missiles, 2,256 drone attacks, and 26 cruise missiles fired from Iran, deploying THAAD and Patriot missile defense systems acquired from the United States.

Despite the overwhelming majority of projectiles being intercepted, interception debris and falling fragments caused damage to civilian infrastructure across Abu Dhabi and Dubai, starting fires and disrupting services.

The strikes on AWS data centers on March 1st, 2026 were qualitatively distinct from other elements of the Iranian campaign.

They were the first known military strikes on major commercial cloud infrastructure operated by American technology companies.

The disruption they caused was not limited to data storage.

Cloud services supporting banking systems, payment platforms, ride-sharing applications, and digital delivery services across the Gulf were affected.

The IRGC then escalated the political dimension of the campaign on March 11th, 2026, when it published a formal target list, released through the Tasnim news agency, naming Google, Microsoft, Nvidia, IBM, Oracle, and Palantir as legitimate targets on the grounds that their AI and cloud platforms enabled American and Israeli assassination operations.

A subsequent list, released in late March, expanded the declared targets to 18 American technology firms including Apple and Meta.

Dubai's acknowledgment that debris from an intercepted Iranian projectile struck an Oracle-linked building in Dubai Internet City underscored that the threat was not hypothetical.

Bahrain's officials began questioning whether additional aerial defense layers should protect commercial campuses. UAE regulators signaled reviews of data localization and redundancy mandates.

The defense dimension of the Gulf AI story, which had existed as a background condition in pre-war planning, suddenly became the foreground.

The economic arithmetic of what had happened was deeply unfavorable to the defenders. Each Patriot interceptor missile costs approximately $4 million.

The Iranian Shahed-136 drones that struck the AWS facilities cost in the low tens of thousands of dollars.

The Terra Drone A1 interceptor, a counter-drone system that Gulf states began exploring in April 2026, costs approximately $2,500 per unit, but deploying it at scale requires trained personnel, command and control infrastructure, and a legal framework permitting autonomous engagement of aerial threats in urban or peri-urban environments.

The economic asymmetry between offense and defense — between a $30,000 drone and a $4 million interceptor — is not a correctable market failure. It is a structural feature of asymmetric warfare, one that military theorists have identified as decisive in both the Ukraine conflict and the current Gulf campaign.

Latest Facts and Concerns

The Securitization of AI Infrastructure

The most significant immediate consequence of the March 2026 strikes was the acceleration of what analysts had previously described as the "securitization" of Gulf AI infrastructure — the process by which commercial technology assets are progressively brought within the orbit of military planning, defense cooperation, and strategic political conditionality.

Gulf states eye cheap Ukrainian-developed drones amid depleted air defense stocks after Iranian attacks, seeking cost-competitive counter-drone solutions.

The financial implications are substantial and still unfolding. AI data center investment in the GCC was projected to reach $5 to $7 billion in 2026, representing a significant escalation from prior years, but those projections were formulated before the drone strikes introduced a new and unquantified layer of physical security expenditure.

The Middle East as a whole was targeting $100 billion annually in energy and AI investment. MENA technology spending overall was projected at $169 billion for 2026.

All of these figures must now be revised upward to account for the cost of physical protection.

A 50% cost advantage in data center construction relative to Western competitors becomes meaningfully less compelling if that cost must be supplemented by missile defense systems, armed security perimeters, redundant infrastructure capable of surviving physical attack, and cyber defenses capable of withstanding sustained IRGC campaigns.

The Forbes analysis published on April 21st, 2026 found that drone defense is now starting to become a must-have for all companies with valuable infrastructure, comparing the emerging dynamic to the trajectory of cybersecurity.

Just as cybersecurity transformed from an afterthought into a mandatory line item in technology investment budgets over the course of two decades, physical counter-drone capability is now on a comparable trajectory for any company operating hyperscale infrastructure in a conflict-adjacent geography.

Qatar's experience is instructive.

Qatar secured a non-binding security guarantee from the United States following Iranian strikes on Doha, and Saudi Arabia obtained a strategic defense agreement with the White House, but those arrangements reflected traditional diplomatic lobbying rather than explicit conditionality tied to technology investment.

The drone strikes of March 2026 have accelerated the fusion of these two previously distinct tracks — technology investment and security guarantees — into a single negotiating framework.

Steven A. Cook, a senior fellow at the Council on Foreign Relations, described AI as "the mother of all insurance policies," a formulation that captures the geopolitical calculation motivating Gulf AI investment with unusual precision.

The Gulf states are betting that by becoming critical partners to Google, Microsoft, and OpenAI, they can make themselves sufficiently strategically important to Washington that the United States will provide robust security guarantees.

That bet has not been definitively validated by events, but the drone strikes have made it more urgent and more explicit.

Cause-and-Effect Analysis

The Causal Architecture of a New Strategic Order

The causal chain running from the Iran war to the reconfiguration of Gulf AI politics operates across multiple levels, each reinforcing the others in a dynamic that will outlast the immediate conflict.

At the first level, the drone strikes on AWS infrastructure demonstrated empirically and for the first time that civilian cloud infrastructure is a viable and productive military target.

Prior to March 2026, this was a theoretical proposition debated in security studies journals and defense planning documents.

The IRGC supplied the proof of concept. No future investor in Gulf data centers can evaluate their risk profile on the assumption that commercial status confers protection.

The insurance and liability implications alone are transformative: standard commercial property coverage does not extend to wartime damage, which means that the enormous financial exposures created by a $700 billion AI infrastructure buildout are now only partially covered by conventional risk management instruments.

At the second level, the demonstrated vulnerability of Gulf AI infrastructure has altered the negotiating dynamic between American technology companies and the Gulf states that host them.

The Gulf's cost advantages — cheap land, cheap energy, low regulatory friction, proximity to capital — remain real, but they must now be weighed against physical risk.

American companies operating in the region face pressure from shareholders, insurance underwriters, and their own security departments to demand explicit protection commitments as a condition of sustained investment.

This means that Gulf host governments, which previously competed primarily on economic terms, must now offer a security premium on top of the economic package.

At the third level, the attacks have accelerated the deepening integration of the American security state into Gulf AI infrastructure.

Washington's AI cooperation agreements with Riyadh and Abu Dhabi had already emphasized security requirements and cooperation, and the Bureau of Industry and Security had implemented reporting and security requirements as part of recent semiconductor sales approvals.

The drone strikes create a political environment in which further integration is not only acceptable but actively demanded by all parties.

The result is a dynamic in which American technology companies and the American security establishment are becoming more deeply intertwined in the Gulf than at any previous point in the bilateral relationship.

At the fourth level, the conflict has reshaped the competitive landscape between American and Chinese technology ecosystems in the Gulf.

Prior to the war, the principal strategic concern for Washington was that Gulf states — despite their formal commitments to U.S. alignment — might quietly maintain or expand their commercial relationships with Chinese technology companies, particularly Huawei, ZTE, and Chinese cloud providers.

The drone strikes have sharpened the choice. Gulf states are now acutely dependent on U.S. military technology for their physical defense.

Accepting Chinese AI infrastructure while relying on American missile defense creates a contradiction that is politically and strategically unsustainable.

The war has therefore accelerated the decoupling of Gulf technology infrastructure from Chinese supply chains in a manner that no regulatory pressure or diplomatic negotiation had achieved.

At the fifth level, the conflict has raised the cost and complexity of the Gulf's ambition to become a globally competitive AI hub.

The $2.7 billion Hexagon contract, the $5 billion NEOM data center, the $15.2 billion Microsoft commitment — all of these investments were calibrated to a risk environment that no longer exists.

Rebuilding the financial model of Gulf AI infrastructure to incorporate the cost of sustained physical protection will require either significant additional capital, meaningful increases in the fees charged to end users and cloud customers, or acceptance of lower returns on sovereign wealth capital.

None of these outcomes is catastrophic, but all of them represent a material deterioration in the original investment thesis.

At the sixth and deepest level, the drone strikes have created a precedent that will shape state and non-state behavior in future conflicts.

The IRGC's successful exploitation of commercial cloud infrastructure as a military target will be studied and emulated by other asymmetric stakeholders in future conflicts.

Hezbollah, Houthi forces, and state-aligned cyber and physical attack units in multiple regions now have a validated template for targeting Western technology infrastructure as an instrument of economic coercion.

The era in which commercial data centers could be treated as neutral infrastructure, insulated from the logic of armed conflict by their civilian character, has definitively ended.

Future Steps

The Architecture of a Securitized AI Landscape

The practical implications of this new environment are already visible in the immediate responses of governments, technology companies, and defense contractors.

They point toward a future AI landscape in the Gulf that will look fundamentally different from the commercial infrastructure paradigm that dominated the period from 2020 to early 2026.

The first and most immediate response involves the physical hardening of existing and planned AI infrastructure.

This encompasses conventional physical security upgrades — perimeter fencing, blast-resistant construction, dispersed power systems — but extends to the deployment of layered counter-drone architectures integrating radar detection, electronic jamming, kinetic interceptors, and AI-powered threat classification systems.

The integration of AI into defensive systems is not incidental — it is the frontier of counter-drone capability, and the Gulf AI infrastructure that is the target of drone attacks is simultaneously the platform on which the best defensive response will be built.

The second response involves the restructuring of technology deals to incorporate explicit security dimensions.

Future AI infrastructure agreements between American technology companies and Gulf states will increasingly resemble hybrid commercial-strategic instruments, combining investment commitments with defense cooperation provisions, security guarantees, and explicit conditions governing supply chain integrity.

The template established by G42's divestment from Chinese hardware as a condition of Microsoft's investment will be extended and deepened.

The third response involves the evolution of the U.S.-Gulf security architecture to explicitly incorporate AI infrastructure protection.

The existing framework of U.S. military presence in the region — the Fifth Fleet in Bahrain, CENTCOM's forward deployment, bilateral defense agreements with Saudi Arabia, the UAE, and Qatar — provides the foundation for this expansion.

But explicitly extending security guarantees to commercial AI infrastructure, rather than relying on the incidental protection provided by general-purpose military deployments, represents a qualitative change in the American security commitment.

Washington must balance the strategic benefits of this deepened engagement against the political costs of appearing to be the military guarantor of corporate profit margins in a region with complex human rights dynamics.

The fourth response involves the reconfiguration of AI infrastructure redundancy and resilience.

The single-region deployment model, in which a hyperscale data center is built in one location and expected to serve regional demand continuously, is no longer adequate.

Gulf governments and their American partners will invest in geographically distributed infrastructure, cross-border redundancy, and dynamic failover capabilities that can route workloads away from facilities under threat.

The UAE's regulatory review of data localization and redundancy mandates, signaled immediately after the March 2026 strikes, reflects this reorientation.

The fifth response involves the development of entirely new markets and industries around the protection of AI infrastructure.

Drone defense is now starting to become a must-have for all companies with valuable infrastructure, analogous to the trajectory of cybersecurity.

The firms that develop, certify, and operate these systems — physical security integrators, counter-drone technology companies, AI-powered threat detection platforms — will find the Gulf a ready and well-capitalized market.

The Israeli defense technology sector, despite the complex political dynamics of the current conflict, possesses the most advanced counter-drone capability in the world and will find ways to channel that technology into Gulf defensive architectures, potentially through third-party intermediaries or through the normalization tracks that survive the current war.

The sixth and longest-range response involves the emergence of what can be described as a new political economy of AI infrastructure, in which technology access, defense cooperation, and political alignment are formally bundled into a single strategic package.

The vision of AI infrastructure as a neutral, globally accessible commercial good — a cloud service available to any customer regardless of political affiliation, analogous to a utility — is being replaced by a vision of AI infrastructure as a strategic resource whose distribution is governed by alliance membership, security commitments, and explicit political conditions.

This shift has profound implications not only for the Gulf but for every region of the world where American technology companies seek to expand.

The Asymmetric Logic That Governs the New Landscape

Understanding what is happening in the Gulf requires grappling seriously with the asymmetric logic that makes cheap drones so strategically consequential.

The economic arithmetic is unforgiving.

Each Patriot missile costs approximately $4 million.

The Shahed-136 drones used against Gulf infrastructure cost in the low tens of thousands of dollars.

Even the Terra Drone A1 interceptor, at approximately $2,500 per unit, requires the construction of a comprehensive command and control architecture costing orders of magnitude more than the individual interceptor.

The defender must always intercept; the attacker can always vary, feint, and overwhelm.

This asymmetry is not unique to the Gulf. It is the central strategic challenge of the contemporary security environment, manifested with particular acuity in the Ukraine conflict and now imported into the Gulf's AI infrastructure landscape.

The lesson of Ukraine is that even highly capable air defense systems, supplied with sophisticated interceptors and supported by Western intelligence, cannot indefinitely sustain a favorable cost exchange rate against mass drone attacks.

The only sustainable response is a combination of kinetic defense, electronic warfare, AI-powered threat detection, and — critically — the development of cheap counter-drone interceptors that can restore cost parity with the attack.

The Gulf states are already pursuing this logic. Reports from April 2026 indicate that they are exploring cheap Ukrainian-developed drones as counter-drone interceptors, seeking to field a cost-competitive response to Shahed attacks following the depletion of conventional air defense stocks.

The Terra Drone A1, developed through Japanese-Ukrainian collaboration, represents another pathway.

But deploying these systems at scale in a complex urban and commercial environment, around data centers located in or near major cities, introduces legal, regulatory, and operational challenges that have no precedent.

The integration of AI into counter-drone systems is not merely technically attractive — it is economically necessary.

Human-in-the-loop systems that require a trained operator to authorize each engagement cannot match the tempo of a massed drone attack.

Autonomous or semi-autonomous AI-powered systems can, in principle, achieve the reaction speed required to intercept drone swarms.

But deploying AI-powered lethal autonomous systems around civilian commercial infrastructure in an urban environment raises profound questions of law, liability, and ethics that no government has yet resolved.

The Political Economy of AI Access Under Conflict Conditions

The political economy of AI infrastructure in the Gulf before March 2026 was fundamentally commercial in character.

Technology companies competed for land, energy contracts, and regulatory approvals. Sovereign wealth funds evaluated investment opportunities against financial return benchmarks.

Regulators focused on data sovereignty, consumer protection, and the management of AI-related risks to labor markets and social stability.

The war has not eliminated these commercial and regulatory dimensions, but it has superimposed a political economy of strategic access on top of them.

In this new political economy, the ability to offer AI infrastructure — chips, cloud services, large language model access, data center capacity — is no longer simply a function of technical capability and commercial willingness.

It is a function of geopolitical alignment.

The United States has already demonstrated this logic through its chip export control regime, which restricts the sale of advanced Nvidia semiconductors to countries that fail to meet security and alignment standards.

The drone strikes accelerate the extension of this logic from the chip level to the infrastructure level.

Gulf states that want access to American AI technology now face a more demanding set of conditions than before March 2026.

They must demonstrate security alignment with Washington's strategic objectives, accept monitoring and reporting requirements on their AI deployments, commit to supply chain integrity by excluding Chinese technology companies from their AI infrastructure, and provide the political and military cooperation that Washington requires to sustain its own position in the region.

In return, they receive not only the technology itself but the security guarantees that make the technology investable.

This is a significant expansion of conditionality relative to the pre-war environment.

It reflects a broader trend in American foreign policy under the Trump administration toward the explicit linkage of economic and strategic instruments — a form of transactionalism that the Gulf states understand well from their experience with oil markets and security commitments, but that takes on new characteristics when applied to AI infrastructure.

Saudi Arabia: The Pivotal Case

Saudi Arabia's position in this new landscape deserves particular attention, both because of the scale of its AI ambitions and because of the fiscal constraints that complicate their realization.

The Saudi Public Investment Fund cut its construction budget by 58%, from $71 billion in 2024 to $30 billion in 2025, signaling a fiscal reorientation even before the war introduced new security costs.

Vision 2030 was already under review before the conflict began, owing to budget shortfalls generated by lower oil prices and the enormous capital demands of projects like NEOM.

The drone strikes add a new layer of complexity to an already difficult fiscal situation.

Saudi Arabia's AI infrastructure ambitions — HUMAIN, the Hexagon compute facility, the DataVolt agreement, the Groq partnership — represent commitments totaling tens of billions of dollars.

Layering physical security costs onto these commitments, at a time when the sovereign wealth budget is contracting, requires either difficult trade-offs between AI investment and other development priorities, or deeper reliance on American financial and strategic partnership.

The latter path is the more likely outcome.

The U.S.-Saudi AI relationship, formalized through the strategic defense agreement signed last year, provides a framework within which security and technology investment can be jointly managed.

American companies investing in Saudi AI infrastructure have an interest in advocating for U.S. security guarantees that protect their assets. Washington has an interest in sustaining the Saudi AI investment commitment as a bulwark against Chinese penetration.

The alignment of these interests, sharpened by the drone strikes, will likely produce a closer and more explicitly securitized U.S.-Saudi technology relationship than anything seen previously.

The UAE: Resilience and Exposure

The UAE entered the conflict with deeper technical and institutional AI capabilities than any other Gulf state, and with a more advanced framework of U.S. security cooperation.

G42's divestment from Chinese hardware, the Nvidia chip export agreement, and the Microsoft $15.2 billion commitment had already established a tightly aligned U.S.-UAE AI relationship before the first drone struck the AWS facility.

The UAE's air defense infrastructure — THAAD, Patriot, and increasingly the counter-drone systems now being urgently procured — is among the most capable in the region.

But the UAE's very success as an AI hub makes it a uniquely attractive target.

The 5-gigawatt AI campus unveiled in late 2025, the 35 data centers with a combined $44 billion investment pipeline — these are precisely the concentrated, high-value assets that asymmetric attackers seek to exploit.

Dubai Internet City and Abu Dhabi's technology zones are located in dense urban environments where the rules of engagement for counter-drone systems are particularly complex.

The acknowledgment that debris from an intercepted projectile struck the Oracle-linked building in Dubai Internet City illustrates the paradox that even successful defense generates collateral risk in a dense urban context.

The Emerging Doctrine: Protection as Condition of Access

The deepest structural consequence of the March 2026 drone strikes is the emergence of an implicit doctrine in which protection is a condition of access to AI infrastructure.

This doctrine is not yet formally articulated by any government or technology company.

It is emerging organically from the behavior of stakeholders operating under the new risk environment created by the conflict.

But its outlines are clear enough to describe with some confidence.

Under this doctrine, American technology companies will not sustain hyperscale AI infrastructure deployments in conflict-adjacent geographies without explicit security guarantees from host governments and from Washington.

Gulf host governments will seek those security guarantees as a condition of their broader alignment with the U.S.-led AI ecosystem.

Washington will provide those guarantees, but at a political price — deeper integration into the U.S. strategic architecture, more explicit exclusion of Chinese technology companies, and greater transparency about the uses to which Gulf-based AI infrastructure is put.

The implications of this doctrine for the broader global AI landscape are profound.

If AI infrastructure becomes a strategic resource whose distribution is governed by alliance membership and political conditionality, the vision of a globally open AI ecosystem — in which any government or company can access world-class AI capabilities on the basis of commercial rather than political criteria — becomes correspondingly less achievable.

The fracturing of the global technology order that began with chip export controls and Huawei restrictions is being accelerated by the Gulf drone strikes into a more fundamental and durable bifurcation.

Conclusion

The Renegotiated Bargain and Its Consequences

The Gulf AI boom will continue.

The capital is committed, the energy surplus is real, the political will in both Riyadh and Washington is intact, and the strategic logic of anchoring the Gulf inside a U.S.-aligned AI ecosystem is, if anything, strengthened by the Iranian challenge.

But it will continue under conditions fundamentally different from those that prevailed before March 1st, 2026.

The bargain has been renegotiated.

Protection is now inseparable from access. Future AI deals in the Gulf will be hybrid instruments — part commercial transaction, part security agreement, part geopolitical alignment commitment.

The cheap drone, costing tens of thousands of dollars, has forced a renegotiation of agreements worth hundreds of billions.

The economic asymmetry between offense and defense that makes the drone so strategically powerful is not correctable through market mechanisms or engineering solutions alone.

It requires a structural response at the level of political economy — a deliberate choice by governments and technology companies to treat AI infrastructure as a strategic resource demanding strategic protection.

The drone strikes have made visible what was always latent in the Gulf AI project: that it was never purely commercial.

The capital may be sovereign wealth; the energy may be natural; the land may be cheap.

But the strategic significance of the enterprise — its role in the AI race between great powers, its position in the competition between Washington and Beijing for technological and political influence, its function as an instrument of Gulf states' own long-term sovereignty and relevance — was always political.

The war in Iran has simply stripped away the commercial packaging that concealed this political reality, leaving the structure of interests, alignments, and vulnerabilities visible for all to analyze.

How governments, companies, and strategists respond to that visible structure will shape the political economy of AI for a generation.