Cheap Drones and the Fracturing of the Gulf's AI Dream: When Commercial Infrastructure Becomes a Battlefield

Executive Summary

The war involving the United States, Israel, and Iran, which began accelerating in early 2026, has exposed a structural vulnerability at the heart of the Gulf's most ambitious economic project: the construction of artificial intelligence infrastructure on a scale unprecedented outside the United States.

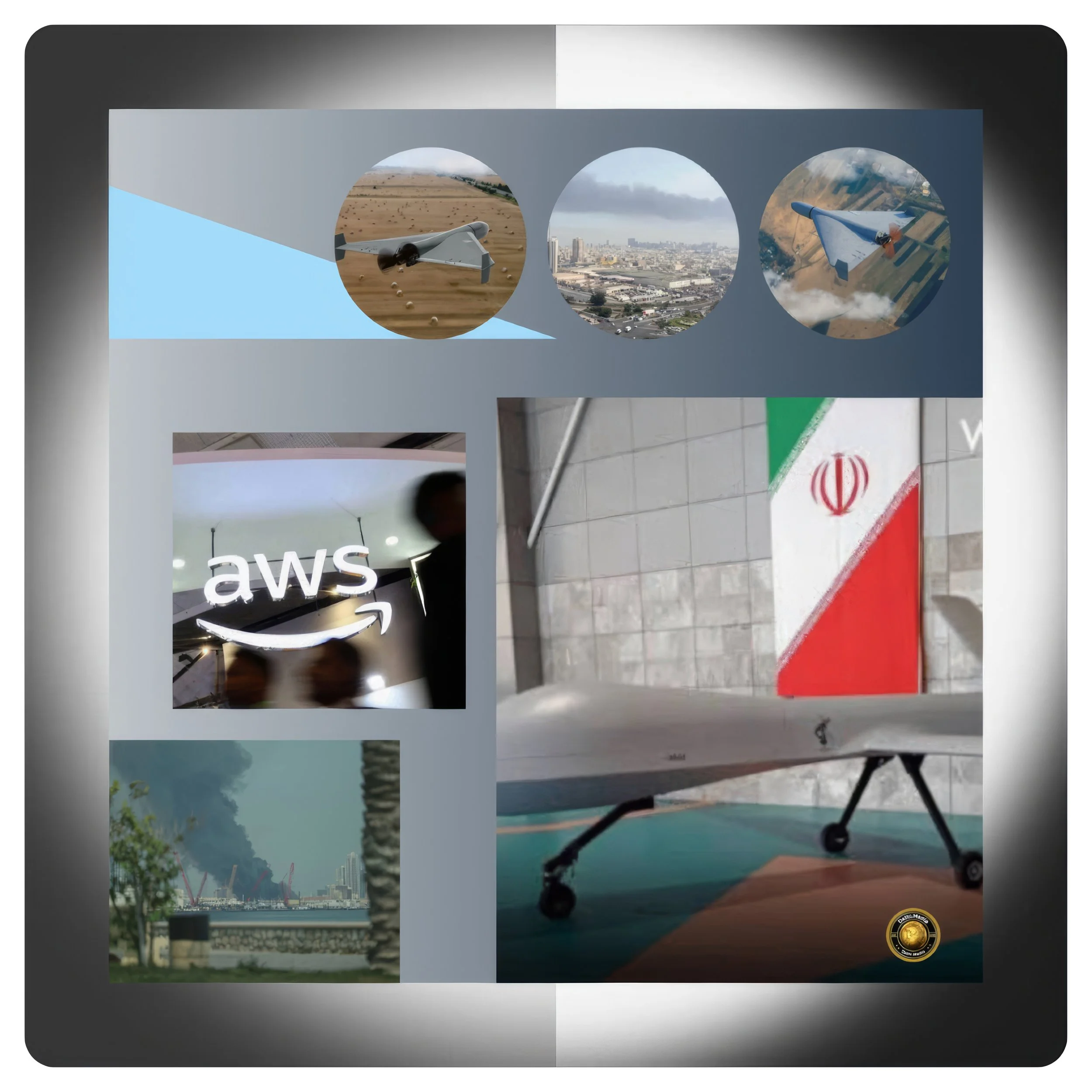

On March 2nd, 2026, drone strikes attributed to Iran struck two Amazon Web Services data centers in the United Arab Emirates and one additional facility in Bahrain.

The Islamic Revolutionary Guard Corps subsequently published a list of 29 technology targets across the Gulf, including infrastructure linked to AWS, Microsoft, Google, Nvidia, IBM, Oracle, and Palantir.

These developments did not emerge in isolation.

They arrived in the middle of a historic $700 billion-plus buildout of AI data centers across Saudi Arabia, the UAE, Qatar, and Bahrain, underwritten by sovereign wealth capital, American technology transfer, and a shared political vision in Washington and the Gulf to anchor the region inside a U.S.-aligned AI ecosystem.

The drone attacks have not ended that ambition, but they have fundamentally altered its terms.

Protection has become inseparable from access. AI deals will henceforth carry defense conditions.

The Gulf's AI boom is no longer purely a commercial story.

It is simultaneously a security story, a geopolitical story, and a contest for the future governance of technology infrastructure.

Introduction: The Convergence of Capital, Strategy, and War

The Gulf's emergence as a global node in artificial intelligence infrastructure did not happen accidentally.

It was the product of deliberate policy choices made over nearly a decade.

Gulf Cooperation Council states recognized, with unusual clarity relative to other developing economies, that the political economy of the 21st century would be organized around data, compute, and AI capability rather than around oil and gas alone.

Saudi Arabia, the UAE, Qatar, and Bahrain each made early and substantial investments in digital infrastructure, in AI research institutions, and in partnerships with the American and European technology industry.

That strategy converged with American interests. Washington, confronting the reality of Chinese technological competition, concluded that keeping the Gulf inside a U.S.-aligned AI ecosystem was a strategic imperative.

The alternative, a Gulf that turned to Huawei, Alibaba Cloud, ByteDance, and other Chinese technology platforms for its AI backbone, was one that American policymakers in both the Biden and Trump administrations regarded as strategically unacceptable.

The result was a progressive unlocking of American chip exports, an acceleration of cloud investment by U.S. hyperscalers, and a set of political agreements that bundled AI access with security commitments.

The war in Iran has now introduced a disruptive variable into this equation that capital alone cannot resolve.

For the first time in history, hyperscaler data centers — the physical infrastructure that supports global cloud services — have been struck in wartime.

The attacks were carried out not with ballistic missiles or supersonic cruise weapons that require expensive and technically sophisticated air defense systems to intercept, but with Shahed 136 drones whose unit cost is estimated in the low tens of thousands of dollars.

The asymmetry between offensive cost and defensive cost has profound implications for the entire enterprise of AI infrastructure development in a conflict-adjacent region.

History and Current Status: The Making of a Gulf AI Superpower

The ambition to transform the Gulf into an AI and technology hub predates the current conflict by many years.

Saudi Arabia announced a $40 billion sovereign wealth fund allocation for AI investment in 2024, targeting semiconductors, data centers, and AI companies.

The UAE's G42 emerged as one of the most important non-American technology platforms in the world, attracting Microsoft, OpenAI, and a succession of U.S. chip approvals.

Qatar's sovereign wealth fund, the Qatar Investment Authority, prioritized AI-related fields as a portfolio category.

Ooredoo, the Qatari telecommunications conglomerate, secured $500 million in financing in September 2024 to expand its AI and data center capacity, including an ongoing partnership with Nvidia for AI-ready platforms across the broader MENA region.

By late 2025, the scale of ambition had become extraordinary. The UAE unveiled a 5-gigawatt AI campus described as the largest outside the United States, spanning 10 square miles.

Microsoft committed $15.2 billion to AI and cloud infrastructure in the UAE between 2023 and 2029, with an additional $7.9 billion expansion announced in November 2025 delivered through Khazna Data Centers.

Groq announced a $1.5 billion Saudi investment for the world's largest inference data center.

Saudi Arabia's NEOM signed a $5 billion DataVolt agreement for 1.5 gigawatts of AI factory capacity.

Saudi Arabia's national AI champion HUMAIN, established in early 2025, announced a $3 billion strategic partnership with Blackstone-backed AirTrunk for AI data centers in the kingdom.

The region's data center capacity was projected to triple from 1 gigawatt in 2025 to 3.3 gigawatts by 2030.

The U.S. government ratified this trajectory with a decisive policy shift in November 2025, when the Commerce Department authorized the sale of 35,000 Nvidia Blackwell-class chips each to UAE's G42 and Saudi Arabia's HUMAIN — reversing earlier restrictions prompted by fears that advanced American technology would flow toward China through Gulf intermediaries.

A broader approval for 70,000 AI chips across both countries was confirmed by early 2026.

These approvals were part of what the Trump administration described as a "Compute Diplomacy" strategy designed to embed Gulf states permanently within the U.S. AI supply chain.

Both G42 and HUMAIN pledged to divest from Chinese technology platforms as a condition of receiving U.S. chips, a political bargain that formalized the alignment of AI access with strategic orientation.

That was the status of the Gulf's AI ecosystem on the eve of the conflict's escalation.

Technology spending in the MENA region was on course to reach $169 billion in 2026, according to Gartner forecasts.

Boston Consulting Group had published a report confirming that the Middle East was emerging as a critical global hub for AI compute, with Qatar, the UAE, and Saudi Arabia offering AI data center costs approximately 50% lower than comparable Western facilities.

The region appeared to have achieved lift-off.

Key Developments: From Data Centers to Drone Targets

The morning of March 2, 2026 changed the calculus.

At approximately 4:30 AM, what was assessed to be an Iranian Shahed 136 drone struck an AWS data center in the UAE, triggering a catastrophic fire and necessitating a complete power shutdown.

Water deployed to suppress the fire caused additional equipment damage. A second AWS facility in the UAE was struck shortly thereafter.

A 3rd facility in Bahrain sustained infrastructure damage when an Iranian drone struck nearby and detonated on impact.

The attacks disabled 2 of the 3 availability zones within AWS's ME-CENTRAL-one region, triggering widespread disruption across Gulf banking, fintech, ride-hailing, insurance technology, digital marketplaces, and government cloud services.

Because the UAE functions as the primary cloud-hosting hub for the entire Gulf, companies in Saudi Arabia, Qatar, Kuwait, Oman, and Bahrain that rely on UAE-based AWS infrastructure experienced simultaneous system failures.

AWS confirmed that physical damage to infrastructure was the cause of disruption and warned that recovery would be gradual given the scale of destruction.

The UAE's position as a financial and technology nexus amplified the economic consequences of what would, in purely military terms, have been a minor engagement.

Call center platforms, bank authentication systems, payment processing, and government digital services all experienced outages.

On March 11th, 2026, the IRGC published its target list through the Tasnim news agency, formally naming 29 technology targets across Bahrain, Qatar, and the UAE and identifying Google, Microsoft, Nvidia, IBM, Oracle, and Palantir as targets linked to U.S. military intelligence and AI systems.

In a subsequent Telegram post on March 31st, 2026, the IRGC expanded its declared target set to 18 additional U.S. technology and finance companies, including Apple, accusing them of functioning as intelligence assets for the U.S. government.

The IRGC had warned explicitly that its "legitimate targets are gradually expanding."

The conflict had entered a qualitatively new phase in which commercial AI infrastructure was treated, as a matter of declared Iranian doctrine, as a legitimate military objective.

In parallel, the U.S. and allied forces struck at least two data centers in Tehran, one of them connected to the IRGC itself, according to Holistic Resilience, a nonprofit tracking airstrikes.

These reciprocal strikes on digital infrastructure confirmed what analysts had long theorized but never before witnessed at scale: that data centers had become battlefield assets on both sides of modern interstate conflict.

Latest Facts and Concerns: The Drone Asymmetry and Its Implications

The economic and strategic dimensions of the problem are inseparable from the technical asymmetry that makes cheap drones so disruptive to expensive infrastructure.

Each Patriot interceptor missile costs approximately $4 million.

The Iranian Shahed 136 drones that struck the AWS facilities cost in the low tens of thousands of dollar.

The Terra Drone A1 interceptor developed by the Japanese firm Terra Drone and Ukrainian partners — which Gulf states began exploring as a counter-drone solution in April 2026 — costs approximately $2,500 per unit.

Gulf states were examining this option precisely because conventional missile-based air defense systems, already strained by months of Iranian drone salvos, were depleting stockpiles at unsustainable rates.

The U.S. responded with a $16.5 billion arms deal approved in March 2026, directing $8.4 billion to the UAE for drones, missiles, radar technology, and F-16 fighter jets, and approximately $8 billion to Kuwait for air and missile defense radar systems.

This was a direct consequence of the attacks on AI infrastructure. The defense dimension of the Gulf AI story was no longer theoretical.

The financial implications are substantial and still unfolding.

Saudi Arabia's Vision 2030 program, the broadest and most expensive economic diversification effort in the Gulf, was already under review before the war began due to budget shortfalls.

The conflict has cost Saudi Arabia more than $10 billion in lost revenues and additional war expenses.

Sovereign wealth fund capital is under mounting pressure as defense budgets surge, a dynamic that risks crowding out the infrastructure and technology investments that sit at the heart of Vision 2030's second phase.

Saudi Arabia's $1.15 trillion Public Investment Fund has pivoted its 2026–2030 investment plan away from high-profile megaprojects toward modernization of infrastructure, industrial integration, and AI-driven economic transition — in part because the conflict has forced a reordering of priorities.

The concern about Chinese penetration of Gulf AI infrastructure has deepened rather than receded as a result of the conflict.

China's "Artificial Intelligence+" strategy, which embeds Chinese AI systems in infrastructure including security apparatuses, urban landscapes, and industrial processes, remained a live option for Gulf states that might conclude the U.S.-aligned path carries unacceptable security risk.

Chinese firms have in the past served as a proving ground for technology systems outside Western markets, and Beijing's bargaining position in the Gulf is strengthened by intra-GCC competition.

The conflict has introduced a new variable into this dynamic: if U.S.-aligned AI infrastructure comes with a target painted on it, the political calculus of deeper alignment with Washington becomes more complicated, even as the security guarantees that Washington offers become more valuable.

The integrity of subsea fiber optic cables passing through the Strait of Hormuz has emerged as a related and under-discussed vulnerability.

These cables connect Gulf data centers to global internet infrastructure, and analysts have noted that Iran will certainly have recognized their strategic importance.

U.S. and allied naval forces monitor the Strait closely, but the concentration of global AI traffic through a chokepoint already contested by Iranian military doctrine is a structural risk that no amount of investment in physical data center hardening can fully eliminate.

Cause-and-Effect Analysis: How the War Reshaped the Terms of the AI Bargain

The causal chain running from the war in Iran to the reconfiguration of Gulf AI politics is multi-layered.

At the first level, the drone strikes on AWS infrastructure demonstrated, empirically and for the first time, that civilian cloud infrastructure is a viable military target.

The proof of concept was the IRGC's, and it has been delivered. No future investor in Gulf data centers can evaluate their risk profile on the assumption that commercial status confers protection.

The insurance and liability implications alone will reshape the economics of hyperscale deployment in the region.

At the second level, the attacks have converted a latent political condition — that AI access and security alignment are related — into an explicit and transactional one.

The U.S. government's "Compute Diplomacy" strategy was always premised on the linkage between chip exports and strategic orientation.

The attacks have now made that linkage visible to Gulf policymakers, technology executives, and sovereign wealth fund managers in a way that abstract policy documents never could.

Protection is now literally inseparable from access.

Future AI deals will be negotiated in the full awareness that data centers require physical defense, and physical defense requires American hardware, American contractors, and American political commitment.

At the third level, the conflict has altered the internal balance within Gulf states between the stakeholders who prioritize economic diversification and those who prioritize security.

Before the war, Vision 2030 and its equivalents were primarily economic and social programs with security dimensions treated as background conditions.

The war has foregrounded security. Sovereign wealth funds that were allocating capital to AI campus construction must now weigh the possibility of those investments being destroyed by $25,000 drones.

Defense ministries that previously had no stake in data center policy now have an obvious and urgent interest. The integration of commercial AI infrastructure with military protection is not a future scenario — it is the present reality.

At the fourth level, the attacks have strengthened the hand of the United States in its competition with China for influence over Gulf AI ecosystems.

Every time Iran targets infrastructure affiliated with American technology companies, it validates Washington's argument that alignment with the U.S.-led AI order is also alignment with the most capable military force in the region.

Conversely, every Shahed drone that strikes an AWS facility creates a political problem for Gulf governments that cannot protect the facilities they have built with American capital.

The result is a dynamic in which American technology companies and the American security state are becoming more deeply intertwined in the Gulf than at any previous point.

At the fifth level, the conflict has raised the cost and complexity of the Gulf's ambition to become a globally competitive AI hub.

A 50% cost advantage in data center construction relative to Western competitors becomes less compelling if that cost must be supplemented by missile defense systems, armed security perimeters, redundant infrastructure capable of surviving physical attack, and cyber defenses capable of withstanding IRGC campaigns targeting U.S. digital infrastructure in the Gulf.

The total cost of an AI campus in the post-drone-strike environment is higher than the pre-war projections indicated.

Insurance premiums, defense contracts, infrastructure hardening, and the political cost of deeper security alignment with Washington all add to the bottom line.

The Geopolitics of Infrastructure: Washington, Riyadh, Abu Dhabi, and the New Alignment

The strategic logic that drives U.S. engagement with Gulf AI development is not simply commercial.

Washington's concern is structural: a Gulf AI ecosystem built on Chinese cloud platforms, Chinese AI chips, and Chinese governance frameworks would give Beijing enduring access to the data flows, infrastructure dependencies, and political leverage that flow from being the foundational technology provider.

The IRGC's target list, perversely, has reinforced the American case.

By treating U.S.-linked AI infrastructure as a legitimate military objective, Iran has made it harder for Gulf governments to argue that a more diversified, less politically aligned approach to AI procurement would reduce their security exposure.

On the contrary, the attacks suggest that the primary threat to Gulf AI infrastructure comes from a regional stakeholder whose strategic conflict is specifically with the United States and Israel, not with Chinese-linked technology platforms.

This dynamic creates a gravitational pull toward deeper U.S.-Gulf integration even as it raises the cost and risk profile of that integration.

Saudi Arabia's Crown Prince Mohammed bin Salman visited Washington and committed to investing $1 trillion in the U.S. economy, concluded a $142 billion defense deal covering advanced air capabilities and missile defense systems, received a major non-NATO ally designation, and locked in a set of AI cooperation agreements that involved Nvidia chip approvals and the HUMAIN framework.

These deals were announced before the March 2026 drone strikes. Their implementation is now taking place in a security environment fundamentally different from the one in which they were negotiated.

The UAE's position is particularly consequential. As the primary cloud hosting hub for the Gulf, with Microsoft's $15.2 billion commitment and the 5-gigawatt AI campus at its center, the UAE is simultaneously the most exposed and the most strategically important stakeholder in the Gulf AI ecosystem.

Abu Dhabi's G42 has already made the political choice to divest from Chinese technology platforms and align with the U.S. supply chain.

The drone attacks validate the strategic wisdom of that alignment in security terms while complicating it in commercial terms.

The UAE will need to demonstrate to investors, to technology partners, and to its own population that the infrastructure it has built is defensible.

That demonstration will require not just diplomatic skill but military investment at a scale that was not contemplated when the AI campus plans were drawn up.

Qatar's position is somewhat different.

The Qatar Investment Authority has been a major AI infrastructure investor, and Ooredoo's data center expansion represents a significant national commitment.

But Qatar also hosts the Al Udeid Air Base, the largest U.S. military installation in the Middle East, which gives it both a security guarantee and a target profile that cannot be easily separated.

The IRGC target list included Qatari technology infrastructure alongside that of the UAE and Bahrain, suggesting that Iranian doctrine does not distinguish between Gulf AI assets on the basis of their political relationships with Washington.

From Tehran's perspective, all Gulf states that host U.S. military forces or U.S.-linked AI infrastructure are legitimate targets.

The Security Architecture of AI: What Infrastructure Defense Now Requires

The technical requirements for defending Gulf AI infrastructure against the drone threat are formidable and expensive.

The Ukrainian experience, which Gulf states have been studying carefully given that Iranian drones of the same Shahed series have been used in both conflicts, demonstrates that no single-layer defense is adequate.

A comprehensive counter-drone architecture requires aerostat-mounted radars for early warning, ground-based AESA radars for tracking, acoustic sensor networks for detecting low-flying threats in radar shadows, electro-optical and infrared systems for visual confirmation, 5G cellular detection systems for urban environments, and radio frequency analysis for identifying remotely piloted platforms.

All of these systems must be integrated by software that fuses data, classifies targets, and delivers actionable intelligence in real time.

The cost of this architecture, when applied to a 10-square-mile AI campus of the kind the UAE has built, is substantial.

The $2,500 Terra Drone interceptor offers a cost-competitive response option against Shaheds priced in the low tens of thousands of dollars, but deploying those interceptors at scale requires trained personnel, command and control infrastructure, and a legal framework that permits autonomous engagement of aerial threats in an urban or peri-urban environment.

These are not trivial requirements.

The alternative of relying on national air defense systems is also problematic.

Gulf states have invested heavily in Patriot missile batteries and related systems, but as the war has demonstrated, the rate of missile expenditure in repelling sustained drone salvos is unsustainable.

Each Patriot interceptor costs approximately $4 million. Iran can produce Shaheds at a small fraction of that cost.

The economic arithmetic of sustained air defense using expensive interceptors against cheap drones systematically favors the attacker.

This is one of the central strategic lessons of both the Ukraine war and the current Iran conflict, and it applies directly to the challenge of protecting Gulf AI infrastructure.

The integration of AI itself into defensive systems offers some mitigation. AI-powered threat detection and autonomous defense technologies represent the frontier of counter-drone capability.

Saudi Arabia's defense agreements with Palantir and IBM include provisions for AI-driven threat analysis, and the kingdom's border security modernization integrates AI surveillance and drone-based monitoring.

But the deployment of these systems at full operational capability will take years, and the attacks on Gulf infrastructure are occurring now.

Future Steps: What the Next Phase of Gulf AI Development Looks Like

The trajectory of Gulf AI development in the post-drone-strike environment involves several distinct but interconnected processes.

First, the physical hardening of existing and planned AI infrastructure.

This means not just perimeter security but distributed architecture that reduces single-point vulnerability, redundant power systems, off-site backup capacity, and the integration of data center construction with air defense planning from the earliest design stage.

The comment by the former White House National Security Council official that Gulf states will need to think about missile defense on data centers was not metaphorical. It is now a design requirement.

Second, the renegotiation of AI investment terms to reflect the new security environment.

Technology companies and sovereign wealth funds that committed capital to Gulf AI infrastructure before the drone strikes are reassessing both the physical risk and the political risk of their positions.

Some will withdraw or reduce commitments; others will seek additional security guarantees or insurance provisions.

The pricing of risk in Gulf AI investment will be reset upward.

This does not mean the investments will stop — the capital, the energy advantage, the political will, and the U.S. strategic interest remain in place — but it does mean they will be structured differently and cost more.

Third, the deepening of the security-AI nexus in U.S.-Gulf agreements.

The $16.5 billion arms deal approved in March 2026 and the $142 billion U.S.-Saudi defense agreement reflect the new reality that AI access and military protection are being negotiated as a package. Future agreements will extend this logic further.

American technology companies operating in the Gulf will increasingly find themselves embedded in a security architecture managed by American defense contractors and overseen by the American national security state.

The line between commercial AI deployment and strategic military presence will continue to blur.

Fourth, the potential development of alternative or distributed AI infrastructure architectures that reduce the Gulf's vulnerability toa single-point attack.

drone strikes can disable 2 of 3 availability zones in AWS's entire Middle East region, the concentration of AI infrastructure in a small number of large facilities is a strategic liability.

The architecture of Gulf AI buildout may evolve toward greater geographic distribution, more redundant interconnection, and a deliberate trading of efficiency for resilience.

This will add cost and complexity but may prove essential for political sustainability.

Fifth, the management of the China question in a more complex threat environment.

If the IRGC continues to target U.S.-linked AI infrastructure while leaving Chinese-linked infrastructure untouched, Gulf governments will face increasing domestic pressure from investors and businesses who question whether the U.S. alignment premium is worth the security premium it entails.

Washington will need to make a more compelling case — not just rhetorically but through visible military protection of the facilities it wants to anchor in its technology ecosystem.

The Trump administration's Compute Diplomacy strategy was built on the assumption that American chips plus American investment would be sufficient to secure Gulf alignment.

The drone strikes have demonstrated that chips and investment without credible physical protection may not be enough.

Sixth, the broader question of international norms around the targeting of civilian digital infrastructure.

The reciprocal strikes on data centers in Tehran and in Gulf cities represent a breakdown of the implicit understanding that commercial cloud infrastructure is not a legitimate military target.

No international legal framework specifically prohibits such strikes, and the lack of a normative barrier means the conflict has set a precedent that will be available to other state and non-state stakeholders in future conflicts.

The targeting of digital infrastructure as an instrument of economic warfare is now established practice, and its proliferation poses risks not just to Gulf AI investment but to the global internet architecture that supports it.

Conclusion: A Bargain Renegotiated

The Gulf's AI boom was premised on a bargain: Gulf states would provide capital, energy, land, and political alignment; American technology companies would provide chips, software, and cloud infrastructure; and the United States government would provide the strategic umbrella that made the whole enterprise viable.

That bargain has not collapsed, but it has been fundamentally renegotiated by the drone strikes of March 2026.

The new terms are clearer and more demanding on all sides.

Gulf states must now invest in the physical defense of their AI infrastructure at a scale they did not anticipate and may struggle to afford as defense budgets and sovereign wealth allocation compete for the same pool of capital.

American technology companies must redesign their Gulf deployments to account for physical threat, distributed architecture, and the political conditions that come with operating inside a U.S. strategic framework in a conflict zone.

The U.S. government must convert its "Compute Diplomacy" rhetoric into credible security guarantees, or risk watching Gulf partners hedge toward Chinese alternatives that do not come with an Iranian target designation.

The deeper shift is conceptual. AI infrastructure has always been, at some level, a geopolitical asset.

The attacks on AWS in the UAE and Bahrain have made that truth undeniable. Data centers are no longer insulated commercial assets in a neutral geopolitical landscape.

They are nodes in a contested strategic infrastructure, subject to the same logic of power, rivalry, and protection that governs every other dimension of international politics.

The Gulf's AI boom will continue.

But it will do so under the shadow of cheap drones, asymmetric warfare, and the uncomfortable recognition that in the twenty-first century, building the future requires defending it.