Beginners 101 Guide: When the World’s Largest Tech Companies Started Borrowing Trillions to Build the Future

Executive Summary: Tech Giants Are Now Borrowing Like Governments

Something big is happening in the world of money that most people haven’t noticed yet.

The largest technology companies in the world — the ones that run our search engines, store our photos, and build the chips inside everything from phones to fighter jets — are no longer funding their plans with their own profits alone.

They are borrowing enormous sums of money from the public, through what are called bonds, at a pace that has never been seen before in corporate history.

FAF article explains what that means, why it matters, and what might happen next.

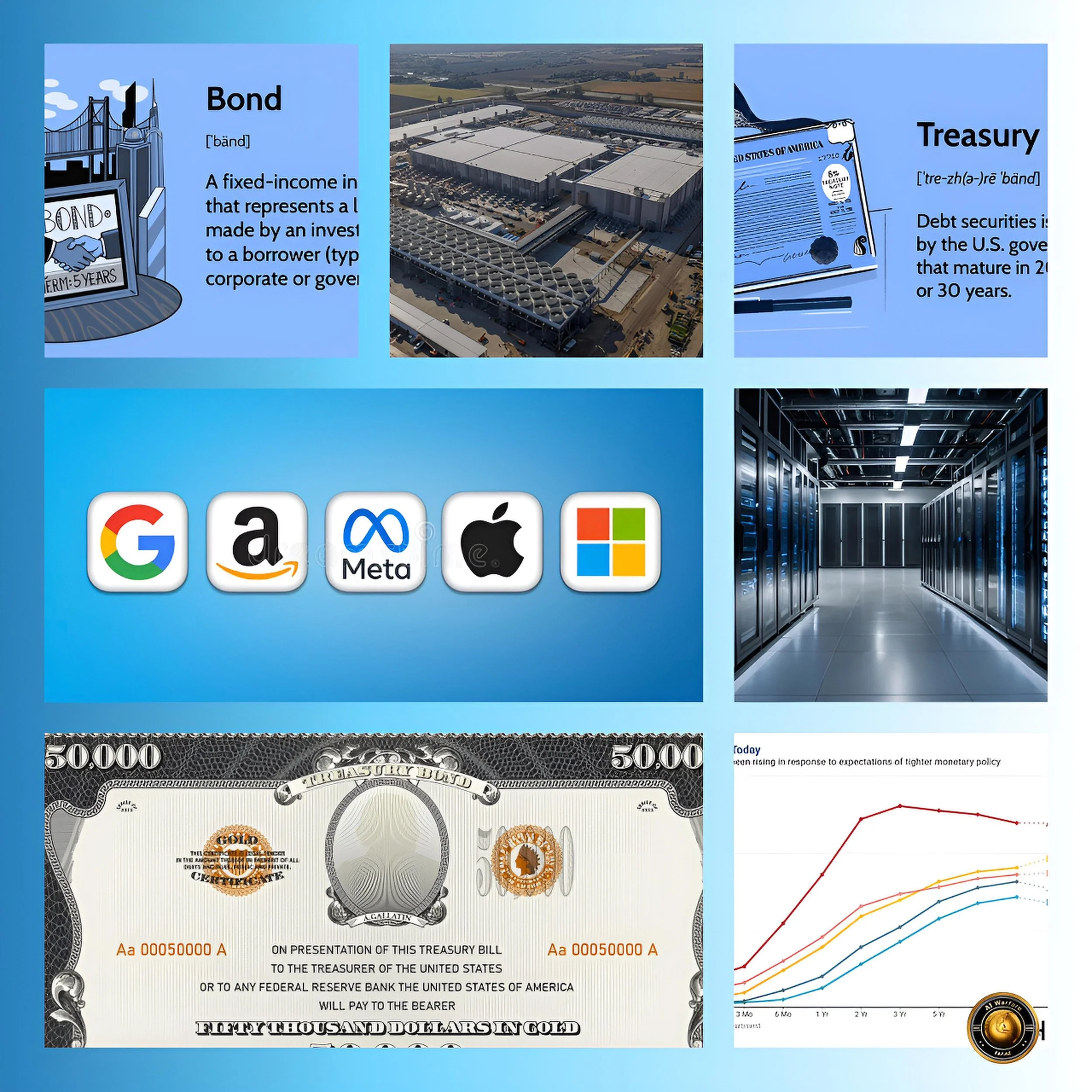

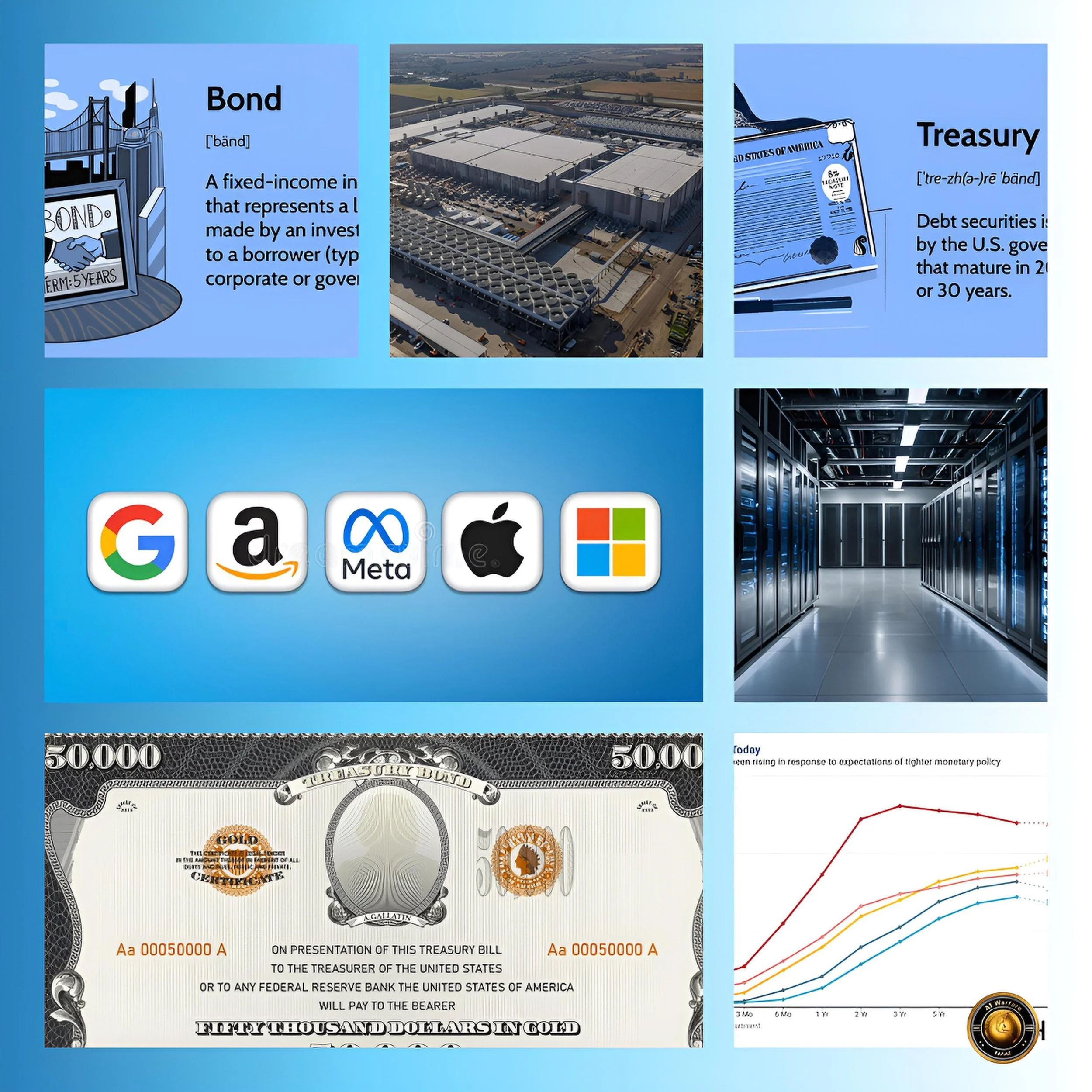

Introduction: What Is a Bond, and Why Should You Care?

Think of a bond as an IOU with a fixed repayment schedule.

When a company needs money to build something large — a factory, a data center, a satellite network — it can either ask shareholders for more equity, use its own saved profits, or borrow from the public by selling bonds.

The people who buy those bonds are usually not individual savers but large institutions: pension funds, insurance companies, and sovereign wealth funds — the giant pools of national savings held by countries like Norway, Singapore, and the Gulf states.

Until very recently, the biggest technology companies didn’t need to borrow much.

They made so much money from selling software and digital advertising that they could fund almost everything from their own cash flows, and they were returning billions to shareholders through buybacks.

That has now changed, and the change happened very fast.

History and Current Status: How We Got Here

To understand why this shift is so striking, it helps to look at a historical parallel.

In the 19th century, building a railway was the most capital-intensive project a private company could undertake.

You needed to buy land, hire thousands of workers, lay hundreds of miles of track, and then wait years before the trains started running and revenue started coming in.

No company could fund that from its own savings.

So railway companies sold bonds — promises to repay investors with interest — and those bonds became the foundation of the modern corporate credit market.

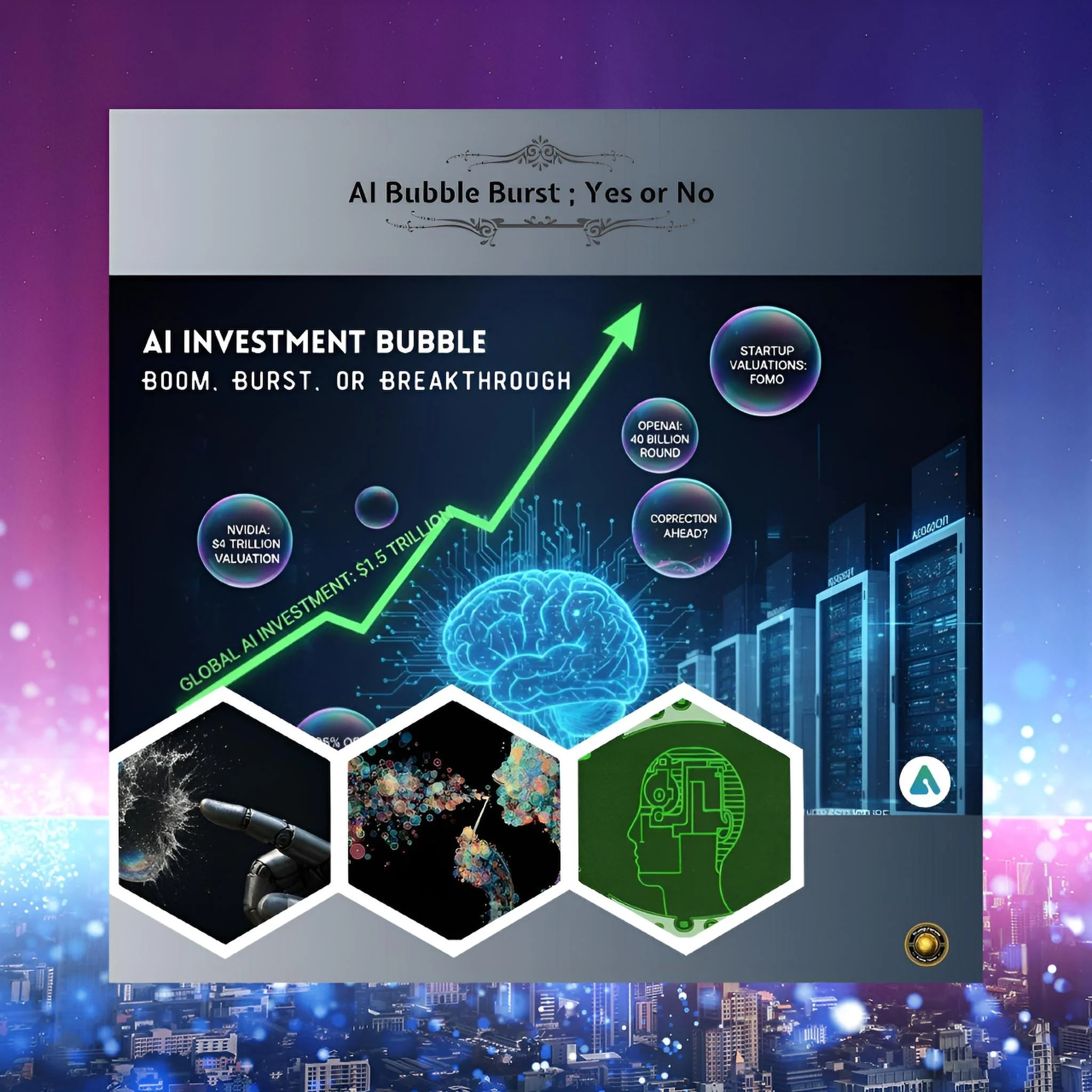

The planned capital expenditure for artificial intelligence by the leading technology firms represents a historic pivot in corporate strategy, and the AI capital expenditure cycle is now the third-largest infrastructure investment wave in US history and growing.

The data centers being built to power AI require the same kind of massive upfront investment as the railways of the 1800s: vast amounts of land, buildings, specialised chips, electrical power, and cooling systems, all of which must be in place before a single AI model can generate revenue.

Worldwide spending on AI is forecast to reach $2.52 trillion in 2026, a possible 44% increase year-on-year, which compares to a total of $1.6 trillion spent on AI between 2013 and 2024.

In other words, what it took humanity more than a decade to spend on AI before, the world is now spending in a single year.

That scale of investment cannot be funded from company cash accounts alone, no matter how profitable those companies are.

Key Developments: The Numbers That Changed Everything

The individual transactions that have taken place in 2026 are staggering in their scale.

Amazon, Meta, Alphabet, Nvidia, Oracle, and SpaceX have together sold roughly $220 billion in AI-linked bonds so far this year, transforming the corporate bond landscape in the process.

To put those numbers in context: $220 billion is more than the entire annual GDP of Portugal.

It is the kind of sum that, historically, only governments could raise through bond markets.

Yet it is being raised by private companies, in a matter of months, to fund the construction of a new kind of infrastructure that most people have never seen and that doesn’t yet generate the returns needed to justify the spending.

Some specific examples help illustrate the scale.

Nvidia, the company that makes the most important chips for running AI systems, priced a $25 billion bond offering in June 2026, its first return to the debt market since 2021, and received $85 billion in orders — more than three times the amount it was selling.

That level of demand means that for every dollar of Nvidia bonds on offer, there were three and a half dollars of investors competing to buy them.

Alphabet, Google’s parent company, issued a rare century bond as part of its debt campaign — a bond that will not mature until the year 2126.

A 100 year bond is so unusual that it is normally only issued by governments. When a technology company issues one, it is essentially asking investors to bet that it will still be a dominant, creditworthy enterprise more than a century from now.

SpaceX completed the largest initial public offering in history in June 2026, debuting on Nasdaq at $135 per share and closing its first day up 19%, and then within days began preparing a bond offering of at least $20 billion.

It is almost unheard of for a newly listed company to borrow that much that quickly, but SpaceX is not a normal company.

Dr. Antonio Bhardwaj, a polymath and global expert in human-centered AI for geopolitical strategy and supercomputing, places these transactions in a broader context. “What is happening in the AI bond market is not simply a story about corporate finance,” he explains. “It is a story about which countries and which companies will control the computational infrastructure of the next half-century. The bond market is the instrument through which that race is being funded — and the investors buying this paper are, whether they know it or not, making bets on the outcome of the most consequential technological competition in history.”

Latest Facts and Concerns: The Risks That Keep Bond Investors Awake

For all the excitement about AI, there are genuine reasons for concern about whether the investment will pay off in the way that bond holders need it to.

Bond investors are very different from stock investors.

A shareholder can wait indefinitely for a company to become profitable.

A bondholder cannot — they are owed fixed payments on fixed dates, and if those payments are not made, the company is in default.

An initiative at the Massachusetts Institute of Technology found that 95% of organisations are obtaining zero return from generative AI projects, and Bain has found that AI cost savings have broadly missed corporate targets.

If the companies buying access to AI infrastructure are not generating returns from it, they will eventually reduce their spending — which means the hyperscalers who borrowed to build that infrastructure will have less revenue to service their debt.

Investors fear that the enormous data centers that are key to the AI buildout could be rendered obsolete by rapid technical improvements that make chips more efficient and reduce demand for capacity — a risk that carries far-reaching implications for those holding bonds with five, eight, or thirty-year maturities.

Imagine lending money to a company that built a network of petrol stations, just before electric vehicles made petrol obsolete.

The infrastructure might still exist, but its value would have collapsed.

Oracle’s free cash flow ran negative $23.69 billion in its most recent fiscal year, and Meta is down 12.4% year to date while Oracle is down 4.85%, reflecting the market’s early attempts to separate companies that can earn a return on AI spending from those that are merely spending.

Cause-and-Effect Analysis: What Happens If the AI Bet Goes Wrong?

The reason that the AI bond market matters to ordinary people — not just institutional investors — is that the money being used to buy these bonds is, in large part, the savings of ordinary citizens held in pension funds and insurance policies.

Technology now accounts for around 10% of the Bloomberg Corporate Bond Index, and Vontobel estimates approximately $1.5 trillion in AI-related bond issuance over the next 5 years, making the AI-related segment 15 to 20% of most corporate bond indices.

That means a growing share of the global savings held in pension funds and insurance policies is becoming exposed to the success or failure of the AI investment thesis.

If the AI boom delivers what its proponents promise, those savings will be secure and the returns attractive.

If it does not, the losses will cascade through the financial system in ways that affect many people far removed from Silicon Valley.

Norway’s $2.1 trillion sovereign wealth fund has identified an AI bubble as a major risk scenario that could cost it 35% of its value, while geopolitical risks including global investment restrictions and severe tariffs could wipe out as much as 37% of its value in a worst-case scenario.

Future Steps: What Comes Next in the AI Debt Story

The pace of AI bond issuance shows no sign of slowing.

Amazon has stated it will not issue further bonds in 2026 after its latest $25 billion deal, suggesting even the most aggressive borrowers are aware of limits — but overall US corporate bond issuance is forecast to reach $2.46 trillion in 2026, up 11.8% from $2.2 trillion in 2025, with AI-related funding the biggest single factor.

The next chapter will be written when companies like OpenAI, which is targeting a public listing as early as late 2026 at a valuation above $1 trillion, begin accessing the bond market.

Unlike the existing hyperscalers, OpenAI does not own the data centers on which its models run — it buys compute from Microsoft.

Its bond issuance, when it comes, will be an attempt to borrow against the value of its AI models and its customer relationships rather than against hard infrastructure assets.

That will require bond investors to make even more abstract assessments of creditworthiness than those currently required to evaluate an Amazon or an Alphabet.

Conclusion: The Long Game in Plain English

Here is the simple version of what is happening.

The world’s most powerful technology companies have decided that building the infrastructure for artificial intelligence is so important — strategically, commercially, and geopolitically — that they are willing to borrow trillions of dollars to do it, locking themselves into fixed obligations that will extend decades into the future.

The markets are, for now, happy to lend to them at favourable rates, because these are extraordinary companies with extraordinary cash generation.

But the risks are real, and they are being distributed across the global financial system in ways that are not yet fully understood.

Dr. Antonio Bhardwaj captures the essential tension. “The bond market is telling us that institutional investors believe the AI supercycle is real, durable, and worthy of long-dated capital commitment. That belief may prove correct. But history teaches us that the greatest infrastructure booms in human history have always produced financial casualties alongside transformative economic gains. The challenge for the generation of policymakers and investors now responsible for navigating the AI debt supercycle is to ensure that when the returns on AI investment eventually materialise — and they will — the financial structures that funded the buildout are resilient enough to survive the inevitable corrections along the way.”

The AI bond market is, in the end, a wager on the future — placed not by speculators but by the most conservative and cautious class of investors in the world.

That should give everyone, from pension savers to finance ministers, reason to pay close attention.