The Strait of Hormuz and the Unraveling of Global Commodity Order: War, Supply Chains, and Systemic Fragility in the Age of Chokepoint Economics

Executive Summary

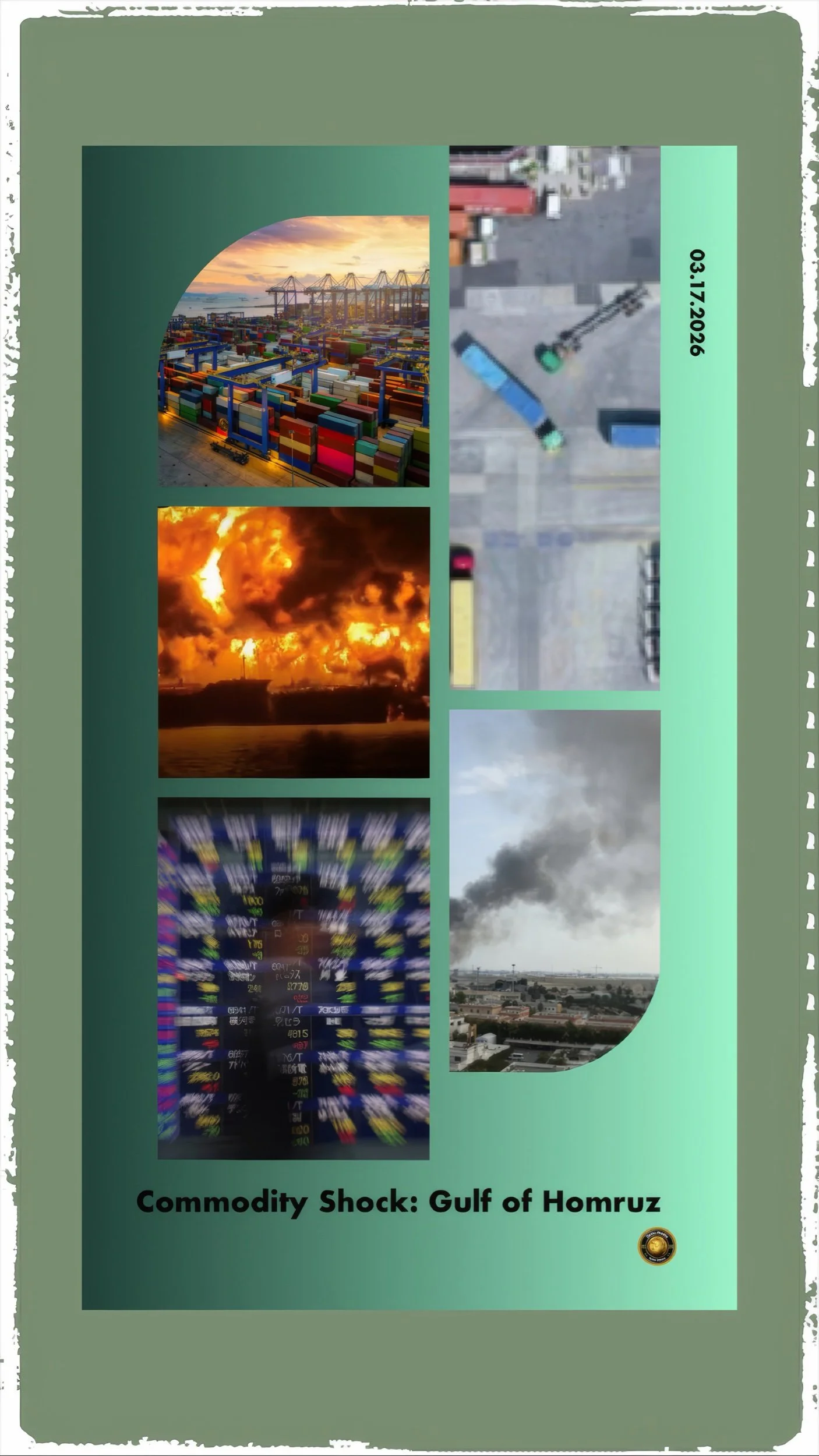

Strait of Hormuz Closed: How One Narrow Waterway Holds the Global Economy Hostage Beyond Energy Markets

The third Gulf War, which erupted on February 28, 2026, following joint United States and Israeli strikes on Iranian nuclear and military infrastructure, has precipitated a commodity crisis of systemic proportions that extends far beyond the oil markets that typically dominate strategic analysis of Middle Eastern conflicts.

Within three weeks of the war's commencement, the Strait of Hormuz — through which approximately 20% of the world's daily oil supply and nearly a third of all maritime crude transport transits — had been effectively shut to commercial navigation.

Iran's Islamic Revolutionary Guard Corps launched retaliatory attacks on commercial shipping, confirmed at 21 separate incidents by March 12, reducing tanker traffic first by 70% before it fell to near zero.

Brent crude briefly topped $106 per barrel by March 16, reaching a peak of $126 per barrel earlier in the month — its highest since July 2022.

Yet the crude oil price, while capturing the world's attention, represents only one dimension of an unfolding crisis that is simultaneously disrupting urea, sulphur, ammonia, aluminium, helium, and critical industrial chemicals, all of which flow in enormous quantities through the same narrow waterway.

FAF analysis examines the structural reasons behind the Gulf's disproportionate role in global commodity supply, the sectoral damage already underway across transportation, manufacturing, and food production, and the long-term geopolitical and economic consequences that will define the post-conflict order.

Introduction: A War With Many Commodities

Beyond Oil and Gas: How the Third Gulf War Is Rewriting the Rules of Global Commodity Supply Chains

Every major Middle Eastern conflict of the past half-century has been interpreted primarily through the lens of oil.

The 1973 Arab oil embargo, the 1980-1988 Iran-Iraq War, the 1990 Iraqi invasion of Kuwait, and the repeated crises over Iran's nuclear programme — each of these episodes trained global institutions, financial markets, and strategic planners to focus on the barrel as the primary unit of geopolitical risk.

The third Gulf War, which commenced on February 28th, 2026, with Operation Epic Fury, is revealing this framework to be dangerously incomplete.

The Gulf region is not merely a reservoir of hydrocarbons. It is, in the twenty-first century, one of the world's primary platforms for the industrial transformation of raw materials into the chemical and mineral building blocks of modern civilisation.

Its hydrocarbons are the feedstock for fertilizer, the energy source for smelting, the process fuel for refineries that turn petroleum into sulphur, ammonia, and a dozen other industrial inputs.

Its geography — situated between fast-growing Asia and wealthy Europe — makes it the natural hub for maritime commodity flows.

And its infrastructure, accumulated over fifty years of petrochemical investment, is deeply integrated into supply chains that keep farms productive, factories operational, and hospitals stocked.

When the Strait of Hormuz closes, therefore, the world does not merely lose oil. It loses the circulation of an entire economic ecosystem.

The humanitarian and industrial consequences of this are now materialising with a speed and severity that have surprised even seasoned commodity analysts.

The war in Iran is, in this sense, a stress test of globalisation itself — exposing the degree to which decades of efficiency-driven supply chain optimisation have concentrated critical dependencies in a single, vulnerable geography.

Historical Context: The Gulf's Rise as a Global Industrial Platform

The Hormuz Chokepoint: Why the Iran War Is Pushing Fertilizers, Helium, and Aluminium Into Crisis Mode

The Gulf Cooperation Council states' emergence as commodity exporters beyond oil is a story that unfolded gradually across the latter decades of the twentieth century and accelerated sharply after 2000.

Saudi Arabia, the UAE, Qatar, Kuwait, and Bahrain all recognised early that hydrocarbon revenues, while vast, were finite, and that the same natural gas that powered their electricity grids and fed their petrochemical plants could serve as a source of diversified industrial wealth.

Qatar's trajectory is illustrative. The discovery of the North Field — the world's largest single natural gas reservoir, shared with Iran's South Pars field — transformed the emirate from a peripheral Gulf state into a global LNG superpower.

The development of Ras Laffan Industrial City from the 1990s onwards created one of the world's most concentrated petrochemical and industrial complexes, integrating LNG liquefaction, helium extraction, urea and ammonia production, polymer manufacturing, and aluminium smelting within a single industrial ecosystem.

Qatar now supplies approximately a third of global helium output — a figure that reflects not only abundance but also a deliberate industrial strategy.

Saudi Arabia pursued a parallel course through its SABIC petrochemical subsidiary, which became one of the world's largest producers of industrial chemicals, polymers, and fertilizer intermediates.

The UAE's Emirates Global Aluminium became one of the world's top five aluminium producers, exploiting cheap gas-powered electricity to smelt aluminium from imported bauxite, with a cost advantage unavailable to competitors in Europe or North America.

By the 2020s, the Gulf states collectively supplied 22% of the world's traded urea, 24% of its aluminium, a third of its helium, and 45% of its sulphur — making the region an indispensable node in the global industrial system.

This concentration was not accidental. It was the product of deliberate policy choices by Gulf governments seeking to monetise their hydrocarbon endowments more fully, attract industrial investment, and create employment for growing national populations.

But it also created a structural vulnerability that was rarely acknowledged in strategic planning: a single maritime chokepoint — 21 miles wide at its narrowest — stood between this industrial platform and the markets of Europe, Asia, and Africa.

Current Status: The Scale of the Disruption

The Hidden Casualties of the Iran War: Sulphur, Urea, and the Fragile Chemistry of the Modern Economy

When Operation Epic Fury commenced on February 28, 2026, and Iran declared the Strait of Hormuz closed to vessel passage, the consequences for commodity markets were felt almost immediately.

Iran's IRGC carried out 21 confirmed attacks on merchant ships within the first two weeks of the conflict, creating conditions under which no commercial insurer would cover vessels attempting to transit the strait.

Over 150 ships are anchored outside the strait, waiting in hope of a rapid diplomatic resolution that has not materialised.

By March 16, the disruption had propagated through multiple commodity markets simultaneously.

Brent crude, the global oil benchmark, had traded as high as $126 per barrel at its peak, before settling around $106 per barrel following the International Energy Agency's announcement of the largest-ever coordinated release of strategic oil reserves — 400 million barrels — a measure that provided temporary relief but could not substitute for the structural loss of supply.

Iran's IRGC, in a statement that shook financial markets, declared that "not 1 litre of oil" would pass through the strait and threatened that prices would reach $200 per barrel if hostilities continued.

But oil is only the beginning of the story. QatarEnergy declared force majeure on March 2, halting LNG production from the Ras Laffan complex following military strikes on the facility. This development simultaneously disrupted approximately 20% of global LNG supply and approximately 30% of global helium output.

Urea prices rose 35% in the 3 weeks following the war's commencement. Aluminium reached a four-year high. Global container shipping rates have surged by 12% since the conflict began.

And nearly half of the world's sulphur supply was, as of mid-March, stranded on the Persian Gulf side of the strait, unable to reach the fertilizer plants in China, Morocco, and Indonesia that depend on it.

Key Developments: Sector by Sector

The Fertilizer Crisis and Its Agricultural Cascades

The disruption to fertilizer supply chains may prove to be the most consequential long-term effect of the Hormuz blockade on global welfare.

The Gulf states dominate nitrogen fertilizer production because natural gas — their most abundant resource — is the primary feedstock for the Haber-Bosch process that synthesises ammonia, from which urea, ammonium nitrate, and other nitrogen fertilizers are derived.

The Gulf's share of world ammonia production is approximately 30%, while its share of globally traded urea reaches between 35% and 45%.

Urea prices at the New Orleans fertilizer hub — the primary benchmark for the North American market — surged from $475 per metric ton to $680 per metric ton within days of the strait's effective closure.

This 43% price increase arrived at the worst possible time: the spring planting season for the American Midwest, when corn and soybean farmers commit to fertilizer applications that determine yield expectations for the year's primary crop.

The timing mirrors, in structural terms, the disruption caused by Russia's invasion of Ukraine in February 2022, which similarly struck at the beginning of planting season and produced fertilizer price spikes that cascaded into food inflation across developing economies.

The sulphur disruption compounds the fertilizer problem.

Sulphur, a byproduct of oil and gas refining, is a critical input for the production of phosphate fertilizers.

China imports roughly 4 million metric tons of sulphur annually from Gulf producers. At the same time, Morocco's OCP Group — the world's largest phosphate exporter and a critical supplier to African and Asian agricultural markets — depends on approximately 3.7 million metric tons per year from the same region.

With nearly 45% of global sulphur supply stranded inside the Gulf, the downstream impact on phosphate fertilizer production is already being felt.

Oxford Economics raised its fertilizer price forecast by 20% for the second quarter of 2026, while Fitch Ratings warned of a "significant impact on the nitrogen fertiliser market" if the blockade persists.

The implications for food security are profound.

The UN Food and Agriculture Organisation warned that aggregate world food prices could rise approximately 2% in 2026 — a figure that, in percentage terms, sounds modest but translates into hundreds of billions of dollars in additional costs for food-importing nations, many of which are already under fiscal strain following the inflationary period of 2022-2024.

For countries in sub-Saharan Africa and South Asia that depend on imported nitrogen and phosphate fertilizers to sustain agricultural productivity, a prolonged supply disruption risks not merely higher food prices but declining crop yields in the 2026-2027 growing seasons.

India's agricultural sector faces particular vulnerability.

The country is both a major consumer of Gulf-sourced fertilizers and a significant importer of crude oil through the Hormuz route — making it doubly exposed to the consequences of the blockade.

India's kharif season, the country's most extensive agricultural period, commences in June with the onset of the monsoon.

If fertilizer supply disruptions are not resolved before May, the impact on sowing decisions and input availability could carry into the late 2026 harvest.

The Helium Crisis and the Semiconductor Industry

Of all the commodity disruptions triggered by the Hormuz blockade, the helium crisis has attracted the most alarm in advanced industrial economies, for reasons that go well beyond its relatively modest unit price.

Helium is an irreplaceable industrial gas: its unique thermodynamic properties — the lowest boiling point of any element — make it essential for the cooling of superconducting magnets used in MRI machines, the purging and pressurisation of rocket engines, and critically, the cooling of semiconductor fabrication equipment in microchip manufacturing.

Qatar supplies approximately a third of global helium output, processed as a byproduct of LNG production at the Ras Laffan complex. When military strikes forced QatarEnergy to halt LNG production on March 2nd, helium production ceased simultaneously.

The American Chemical Society's Chemical and Engineering News reported on March 5th that the war had "taken one-third of the world's helium supply off the market." It warned that if the conflict continued for more than two weeks, disruption for helium users would become severe.

The implications for the semiconductor industry — already navigating the aftereffects of the 2020-2023 chip shortage — are substantial.

Chipmakers in Taiwan, South Korea, Japan, and the United States rely on helium for the precise environmental controls required in cutting-edge fabrication facilities.

Unlike many industrial gases, helium cannot be synthesised or substituted; it must be extracted from natural gas deposits that contain it in sufficient concentrations, and the global supply base is limited to a handful of locations, of which Qatar's Ras Laffan is one of the most productive.

The International Semiconductor Industry Association has identified helium supply security as a "critical infrastructure" concern following the Qatar shutdown.

The helium crisis thus introduces a technology dimension to what began as an energy crisis.

In an era defined by the geopolitical competition over semiconductor supply chains — already the subject of intense US-China rivalry and the object of industrial policy interventions from Washington's CHIPS Act to the EU's own semiconductor strategy — a 30% reduction in global helium supply represents a direct challenge to the continuity of advanced manufacturing.

The downstream effects could include production slowdowns at fabrication plants, rising helium prices that increase chip production costs, and heightened pressure on alternative helium sources in the United States, Russia, and Australia.

The Aluminium Industry Under Pressure

Aluminium's exposure to the Hormuz crisis operates through multiple vectors.

The Gulf region accounts for approximately 24% of global aluminium trade, with production concentrated in the UAE, Qatar, and Bahrain.

These producers exploit cheap, gas-fired electricity to power energy-intensive smelting operations — a competitive advantage that has allowed Gulf aluminium to undercut producers in Europe and North America for decades.

When QatarEnergy suspended downstream aluminium production alongside its LNG halt on March 3rd, a significant portion of Gulf smelting capacity went offline.

At the same time, the blockade has disrupted the inbound supply chains on which Gulf aluminium production depends. Emirates Global Aluminium's Al-Taweelah alumina refinery, situated near the UAE's Khalifa Port, is the region's primary processor of bauxite — the ore from which alumina is refined before smelting.

Bauxite arrives by ship from Guinea, Australia, and other mining centres; with commercial shipping effectively suspended in the Gulf, the flow of bauxite has been curtailed, threatening to deplete alumina inventories.

The result has been a four-year high in aluminium prices on the London Metal Exchange, with ramifications across the automotive, aerospace, packaging, and construction industries that rely on aluminium as a primary material input.

Europe is particularly exposed. Its industrial base — already weakened by the energy price shock that followed Russia's 2022 invasion of Ukraine — depends on Gulf aluminium imports to supplement its own constrained production capacity.

German automotive manufacturers, who consume aluminium intensively in vehicle body construction, have warned of potential supply disruptions if the blockade extends beyond a few weeks.

The European aerospace industry, which sources aluminium for both civilian and military applications, faces similar pressures.

Transportation: The Shipping Industry and the Rerouting Calculus

The immediate effect of the Hormuz blockade on global shipping has been to reintroduce the constraints of the Red Sea crisis on a larger scale.

When Houthi attacks on commercial shipping in the Red Sea began in late 2023, carriers responded by diverting vessels around the Cape of Good Hope — adding two to three weeks to Asia-to-Europe transit times and significantly increasing fuel consumption.

The Hormuz closure has replicated and, in some respects, intensified this disruption: vessels that would ordinarily load at Gulf ports cannot do so, while those attempting to transit face the threat of Iranian drone and missile attacks.

Vespucci Maritime CEO Lars Jensen estimated at the TPM26 shipping conference in March 2026 that approximately 2 million twenty-foot equivalent units of cargo would be affected by the conflict, based on vessels from Gulf ports or bookings within the next 90 days.

The compound index monitoring global container shipping spot rates had surged 12% since the war began, reversing what had been, at the start of 2026, a buyer's market with slight overcapacity.

Carriers who had been under pressure to accept lower long-term rates abruptly reversed their negotiating positions, stalling contract finalisation and shifting market dynamics decisively in their favour.

Beyond container shipping, the crisis has disrupted air cargo routes. Middle Eastern aviation hubs — Dubai International, Doha's Hamad International, and Abu Dhabi International — handle a disproportionate share of global air freight between Asia and Europe, particularly for time-sensitive, high-value goods including pharmaceuticals, electronics, and perishable agricultural products.

With combat operations in the region, airspace closures and diversion requirements have grounded or rerouted significant volumes of air cargo, adding transit time and cost to supply chains that cannot use ocean shipping alternatives.

The ripple effects on fuel costs across all transport modes are significant. Airlines, trucking companies, and rail operators all face higher fuel bills as crude oil and refined product prices remain elevated.

For industries with thin margins — food processing, logistics, retail — higher transportation costs quickly translate into pressure on consumer prices.

Pharmaceuticals and Healthcare: The Invisible Vulnerability

The pharmaceutical industry's exposure to the Gulf crisis operates along dimensions that have received insufficient attention in public analysis.

India, the world's largest exporter of generic medicines, sources a significant proportion of its active pharmaceutical ingredients — the chemical compounds that constitute the active component of drugs — from manufacturers that rely on Gulf-derived petrochemicals and industrial gases.

The disruption of these input supply chains, combined with the closure of Middle Eastern air cargo routes, has created compound pressure on pharmaceutical supply chains.

The Print reported on March 15th that the war is disrupting critical medicine supplies to the Gulf region itself, with refrigerated cancer drugs — which require unbroken cold chains and often transit through Middle Eastern aviation hubs — facing particular risk.

For patients in Gulf states who depend on imported oncology medications, the combination of airspace restrictions and port closures threatens treatment continuity with no simple substitution.

The humanitarian dimension of this disruption deserves greater prominence in international policy discussions than it has thus far received.

The helium shortage also has a direct healthcare dimension.

MRI scanners — essential diagnostic tools in hospitals worldwide — rely on helium-cooled superconducting magnets.

A prolonged helium supply crisis could, in extremis, affect the operational continuity of MRI facilities that require periodic helium replenishment, with implications for medical imaging capacity in health systems already managing post-pandemic backlogs.

Cause-and-Effect Analysis: The Architecture of a Systemic Crisis

When the Gulf Burns, the World Starves: The Iran War's Devastating Impact on Global Agriculture and Industry

The commodity crisis generated by the Hormuz blockade is not a simple supply-demand imbalance in individual markets.

It is a systemic event — one in which disruptions in one commodity cascade through intermediate production processes into shortages in others, amplified by financial market dynamics and the psychology of precautionary hoarding.

The causal architecture can be understood as operating across three distinct layers.

The first layer is the direct supply disruption: the physical inability of vessels to transit the Strait of Hormuz prevents the export of oil, gas, urea, ammonia, sulphur, aluminium, helium, and dozens of other commodities from Gulf production facilities to their global markets.

This layer generates immediate price spikes and inventory drawdowns in importing countries.

The second layer is the feedstock cascade: the same blockade that prevents exports also prevents the import of raw materials required for Gulf production.

Emirates Global Aluminium cannot receive bauxite; Gulf fertilizer plants that depend on imported catalysts and chemicals face operational disruptions; QatarEnergy's complex industrial ecosystem at Ras Laffan, which integrates gas, chemicals, and metals production in interdependent processes, cannot function when logistics are severed in multiple directions.

Production disruptions compound the export blockade, meaning that even if the strait reopens, recovery of supply will take weeks or months rather than days.

The third layer is the financial and expectational amplification: commodity traders, aware of the physical disruption, engage in precautionary buying and speculative positioning that drives prices above what the physical supply shortage alone would justify.

Importers who fear further disruption place orders beyond their immediate needs, creating artificial demand surges that exacerbate price increases. Agricultural commodity markets, already volatile after the 2022 food price crisis, are particularly susceptible to this dynamic.

The interaction between these three layers creates a crisis that is more severe and more durable than any single component would suggest. Even a swift military resolution — which analysts, as of mid-March 2026, consider unlikely — would not immediately reverse the damage.

Carnegie Endowment researchers warned that "even if the Strait of Hormuz does open soon, restarting production and transport for fertilizers and their components could take weeks — weeks that farmers preparing for planting season do not have".

The disruption of JIT (just-in-time) production schedules and the physical repositioning of the global shipping fleet cannot be undone overnight.

Geopolitical Stakes: The Structural Vulnerabilities of Globalisation

The Third Gulf War's Silent Victims: How Commodity Shortages Are Cascading From Pharmaceuticals to Semiconductors

The third Gulf War is exposing structural vulnerabilities in the global economic architecture that have been building for decades.

The logic of comparative advantage and free trade, which drove the globalisation of supply chains from the 1980s onwards, produced spectacular gains in productive efficiency but also created concentrated dependencies on specific geographies that were never adequately stress-tested.

The Gulf's dominance in petrochemical production is one example of this dynamic; China's dominance in rare-earth processing is another; and Taiwan's concentration in advanced semiconductor fabrication is a third.

In each case, the concentration of productive capacity in a single location provided cost advantages that made dispersion economically irrational at the individual-firm level, even as aggregate systemic risk was growing.

The Hormuz crisis is, in this sense, a structural consequence of the same logic that produced the 2020-2023 semiconductor shortage and the 2021-2022 supply chain chaos — the repeated discovery that efficiency-optimised global supply chains are brittle under stress.

The geopolitical response to this discovery will inevitably include pressure to diversify supply chains. But diversification is expensive and slow.

New fertilizer production capacity cannot be built outside the Gulf overnight; helium extraction requires specific geological conditions; aluminium smelting requires cheap, sustainably sourced electricity, which is hard to source at scale in non-Gulf locations.

The transition to more diversified supply chains, even if it begins now, will take years if not decades. In the interim, the world remains exposed.

The role of the United States as both a military stakeholder and an economic stakeholder in the crisis is structurally complex.

Washington's decision to strike Iran, alongside Israel, was driven by strategic calculations about nuclear non-proliferation and regional security architecture.

But the same strikes set in motion the commodity disruptions that are now creating inflationary pressure in the United States itself, complicating President Donald Trump's domestic economic agenda and generating political friction with NATO allies who are bearing disproportionate costs from the energy price shock.

Trump's demand for NATO assistance and his decision to oversee the largest-ever strategic oil reserve release reflect the magnitude of the economic blowback from a conflict that was, in its initial strategic conception, presumed to be militarily decisive and economically manageable.

Iran's own position is paradoxical.

As a major hydrocarbon producer that depends on oil exports for government revenue, Iran has an inherent incentive to avoid prolonged Hormuz disruption.

But the strategic logic of using the strait as a coercive instrument — threatening the global economy to deter further US and Israeli military action — is compelling from Tehran's perspective, precisely because the costs are borne so widely.

The IRGC's threat that oil prices would reach $200 per barrel is a credible deterrent only because the world understands, now more than ever, how dependent it is on Gulf commodity flows.

Future Steps: What Comes Next for Global Commodity Markets and Geopolitical Order

Chokepoint Economics: The Iran Conflict and the Systemic Unraveling of Globalised Industrial Supply Chains

In the near term — the next 30 to 90 days — the trajectory of commodity markets will be determined primarily by the pace of military developments and the prospects for diplomatic resolution.

A ceasefire or negotiated humanitarian corridor arrangement that permitted commercial vessel transit would provide immediate relief to shipping and allow the gradual resumption of commodity exports from Gulf facilities that have not suffered physical damage.

But the physical restoration of damaged infrastructure at Ras Laffan, at Gulf aluminium facilities, and at fertilizer plants that drone attacks have struck will take considerably longer.

In the medium term — 6 to 18 months — the crisis is likely to accelerate strategic investments in supply chain diversification that governments and corporations have been contemplating but not fully committing to since 2022.

Fertilizer-importing nations in Asia and Africa will intensify efforts to develop domestic production capacity or diversify sourcing toward producers in Russia (under continued sanctions pressure), Canada, and North Africa. Semiconductor manufacturers will accelerate efforts to develop helium conservation technologies and alternative sourcing arrangements.

Aluminium consumers will seek longer-term contracts with producers outside the Gulf, including in Australia, Canada, and Norway.

The impact on global food systems deserves particular attention in policy planning.

The combination of higher fertilizer prices, higher fuel costs for agricultural machinery and transport, and supply uncertainty during the critical spring 2026 planting period creates the conditions for a significant food price event in the second half of 2026 and into 2027.

For food-importing nations with limited fiscal space — particularly in sub-Saharan Africa, South Asia, and parts of the Middle East — the consequences could be severe, potentially requiring emergency humanitarian responses from multilateral institutions including the World Food Programme and the International Monetary Fund.

The structural reform of global commodity governance — including diversifying supply chains, building strategic reserves for non-energy commodities, and redesigning trade agreements to include supply security provisions — was barely on the international policy agenda before February 28th, 2026.

The Hormuz crisis will likely propel it to the centre of G7 and G20 discussions in the months ahead.

The IEA's strategic oil reserve release demonstrated that institutional mechanisms exist for crisis management in the energy sector; no equivalent mechanisms exist for helium, urea, sulphur, or aluminium.

The geopolitical architecture of the post-conflict Middle East will also require fundamental reconsideration.

The third Gulf War has demonstrated that the security of the Strait of Hormuz is a global public good of the first order — not merely for energy supply, but for the entire edifice of modern industrial civilisation.

The institutional arrangements for its protection — historically dependent on the US naval presence and deterrence — have been revealed as insufficient in a context in which the United States itself is a party to the conflict.

New multilateral frameworks for strait security, potentially including roles for regional powers such as India and Turkey, for Gulf states themselves, and for major commodity-importing nations in Asia and Europe, will need to be negotiated as part of any durable post-conflict settlement.

Conclusion: Chokepoint Economics and the Future of Globalisation

From Farmlands to Chip Factories: How the Gulf War Is Threatening Global Food and Technology Security

The third Gulf War has delivered a brutal pedagogical lesson about the relationship between geography, industrial concentration, and global economic stability.

The Strait of Hormuz is not simply an oil artery; it is the circulatory system through which flows a disproportionate share of the fertilizers that grow the world's food, the aluminium that constructs its infrastructure, the helium that cools its semiconductors, and the petrochemicals that sustain its pharmaceutical and manufacturing industries.

The assumption, embedded in decades of supply chain management doctrine, that these flows could be taken for granted because they had never been seriously interrupted — that geographical concentration was a cost-benefit rather than a risk — has been exposed as a form of collective strategic myopia.

The world is paying the price for that myopia in the form of $ 106-per-barrel oil, 35% higher fertilizer costs, a 30% reduction in global helium supply, and the spectre of food price crises in economies that can least afford them.

The path forward requires not merely the resolution of the immediate military conflict, but a fundamental rethinking of the architecture of globalisation — one that builds resilience and redundancy into critical supply chains at the cost of some productive efficiency, and that treats supply security as a strategic imperative alongside climate resilience and technological competitiveness.

The crisis of March 2026 has made that case more powerfully than any academic analysis ever could.

The question is whether the world's governments, businesses, and institutions will learn their lessons before the next chokepoint closes.