Executive Summary

Artificial intelligence, or AI, is changing the world very fast.

Companies are spending hundreds of billions of dollars on it.

Stock markets are reacting with excitement and fear.

But here is the honest truth: nobody really knows what AI is worth right now.

This article explains why that confusion is normal, why it has happened before, and what it means for ordinary people, investors, and the global economy.

Introduction: The Problem With Pricing the Future

Imagine you are asked to guess how much a seed will grow in the next 20 years.

You know the seed is real. You know trees can grow tall.

But you don't know exactly how tall this particular tree will grow, or when it will start producing fruit, or whether a storm will knock it over in year five.

That is roughly the problem investors face right now with AI.

A stock market is essentially a machine for guessing the future. When things stay roughly the same from year to year, that guessing is not so hard.

But when something truly new and powerful appears — like AI — the guessing becomes extremely difficult.

Nobody knows exactly who will win, how long it will take, or how much money will be made.

History Tells a Familiar Story: It Has Been Like This Before

This kind of confusion is not new. Think about the railways in Britain in the 1840s.

People could clearly see that trains were going to change the world — and they were right. Trains did change everything.

So investors rushed to put money into railway companies.

But most of those investors lost money, even though trains turned out to be hugely important.

The technology won, but the investors were wrong about which companies would profit and how quickly.

The same story repeated itself in the 1990s with the internet.

Between 1995 and the year 2000, the technology-heavy Nasdaq stock index rose by approximately 580%.

Companies that had never made a profit were worth billions of dollars.

Then the bubble burst. By 2002, the Nasdaq had lost about 78% of its value. Millions of ordinary investors lost their savings. And yet — the internet did become as transformative as everyone had hoped.

Amazon survived and became one of the most valuable companies on earth.

Google was founded during the crash and became a giant. The technology was real; the prices were just wildly wrong.

AI is following a similar script. The technology is genuinely powerful.

But working out who profits from it, and when, is as hard now as it was with trains and the internet in their early days.

Current Status: Enormous Spending, Uncertain Returns

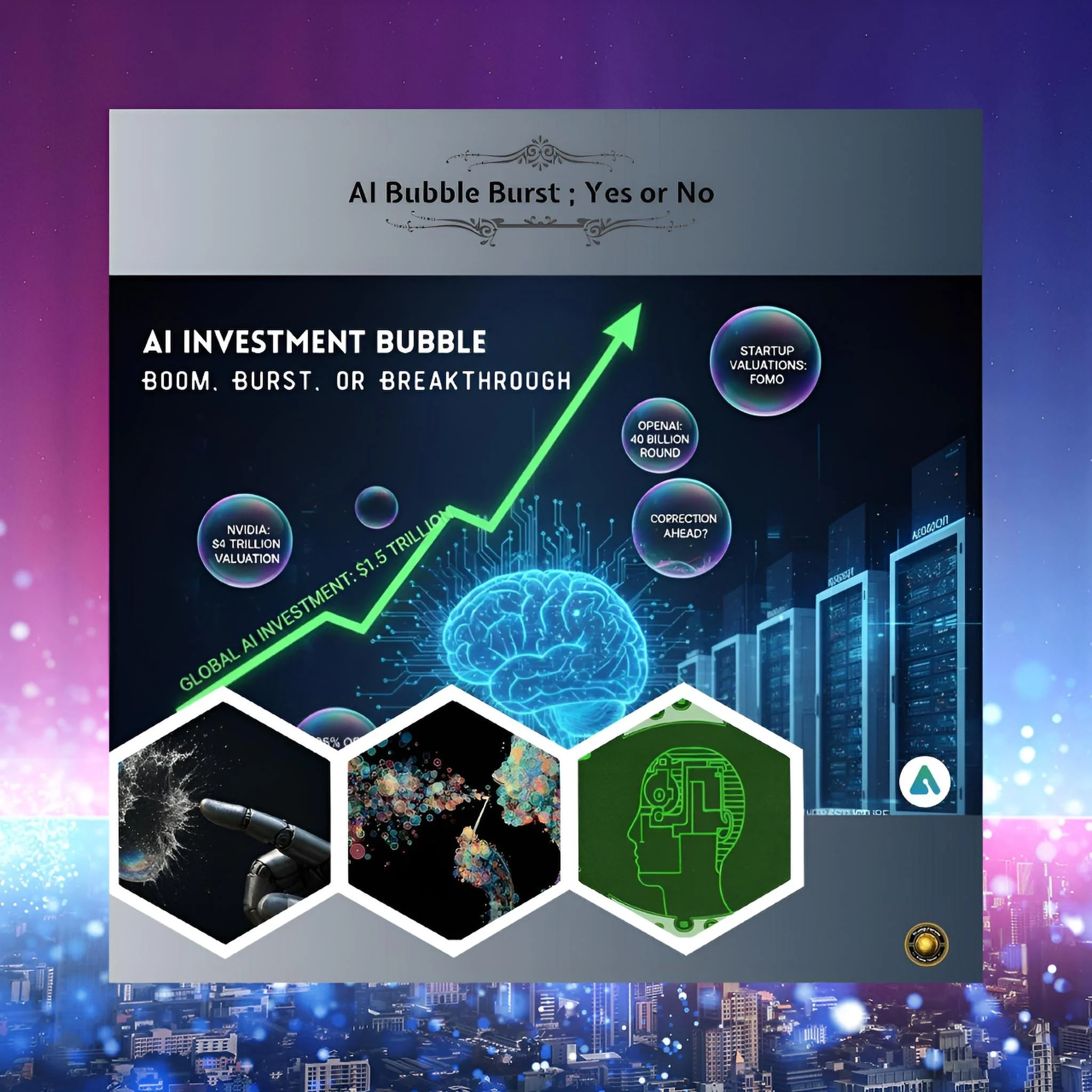

Right now, the numbers involved in AI investment are almost difficult to imagine.

Just three giant companies — Amazon, Google, and Microsoft — are together expected to spend $494 billion on AI-related investments.

The entire AI sector received $202.3 billion in fresh capital in 2025, which is 75% more than the year before.

The AI industry is also borrowing money from bond markets to fund further expansion, with $141 billion in new debt issued in 2025.

These are staggering sums. But here is the puzzle: the actual measured benefit of all this spending has been surprisingly modest so far.

Wharton University's researchers estimate that AI will increase the total size of the global economy by about 1.5% by 2035.

That sounds significant — and it is — but it means the return on those hundreds of billions in investment will be spread very slowly across the whole economy, rather than flowing back quickly to investors.

A Nobel Prize-winning economist has estimated that AI will boost overall productivity by only about 0.5% to 0.7% over the next 10 years.

For individual tasks — writing emails, reviewing legal documents, writing computer code — AI can improve productivity by 14% to 55%.

But when companies try to use AI across their entire operations, 95% of those efforts fail to grow beyond small test programs.

Think of it this way: AI is very good at helping individual workers do specific jobs faster.

But turning those individual improvements into something that transforms an entire company — or an entire economy — is much harder and slower than the investment numbers suggest.

Key Developments: The DeepSeek Shock and the Crumbling of Assumptions

One of the biggest surprises in AI investing happened on January 27, 2025.

A small Chinese company called DeepSeek released an AI model that appeared to be just as capable as the best American AI systems — but built at a fraction of the cost.

The reaction in financial markets was immediate and dramatic. Nvidia, the company that makes the most advanced AI chips, lost $589 billion in market value in a single day.

Why such a violent reaction?

Because investors had built their confidence in AI valuations on a specific assumption: that making good AI requires spending enormous amounts of money on advanced chips and data centers, and that only the biggest American companies could afford to do this.

DeepSeek suggested that assumption might be wrong.

If a cheaper AI system could compete with an expensive one, then the companies spending the most money on AI infrastructure might not have the dominant position everyone assumed.

It is as if everyone was sure that only the most expensive cars, requiring the most complex factories, could win the race — and then a small workshop appeared with a cheaper car that performed just as well.

Suddenly the value of those expensive factories looks questionable.

The price of renting AI computing power has already fallen from about $4 per hour to about $2 per hour. Industry analysts are already using the phrase "price war" to describe competition in AI chips and services.

This falling price is good news for people who use AI.

But it is worrying news for companies whose very high stock prices depend on AI products remaining expensive and scarce.

The Valuation Problem: Very Big Numbers, Very Big Questions

The seven largest technology companies — often called the Magnificent Seven — now make up about 30% of the entire S&P 500 stock index.

That means if you invest in a standard index fund tracking American stocks, nearly a third of your money is sitting in these seven companies.

And a large part of those companies' values is based on expectations about AI.

Analysts estimate that between 15% and 25% of the S&P 500's entire value — hundreds of index points — comes directly from investors' belief that AI will soon deliver huge economic benefits.

If those beliefs turn out to be premature — if AI takes longer to produce those benefits than investors assumed — the market could drop to a level of 3,900 to 4,400 on the S&P 500, a significant decline from current levels.

However, there are important differences between today and the worst days of the dot-com bubble.

Back in 2000, the biggest tech companies were being priced at 70 times their expected earnings.

Today, the biggest AI companies trade at about 25 to 30 times expected earnings.

That is still expensive, but it is much more connected to reality. Nvidia's revenue from AI data centers grew by 279% in 2024.

These are real businesses with real profits. The issue is not that the companies are fraudulent — it is that the prices already reflect enormous optimism about a future that has not yet fully arrived.

Cause and Effect: Why the Confusion Is Built Into the Technology Itself

Here is a helpful way to understand why investors are confused.

When AI makes a single lawyer faster at reviewing documents, that benefit is easy to measure.

But when AI is deployed across an entire law firm, then across the entire legal industry, then across the whole economy — the effects start interacting with each other in complex ways.

Some lawyers become more productive.

Others lose their jobs. Law firms may charge less, benefiting clients but hurting profits. New kinds of legal services may emerge that did not exist before.

The total economic effect becomes genuinely hard to calculate, and very hard to time.

This is what economists call the "productivity paradox." When electricity arrived in factories in the late 1800s, factory owners initially saw little improvement in productivity.

Workers and managers needed years to reorganize their factories around the capabilities of electric motors.

The full productivity benefits of electricity did not show up in economic data until about 20 years after it was widely available.

The internet showed a similar pattern.

Widespread commercial internet access began in the mid-1990s; the major macroeconomic productivity effects did not clearly show up in national statistics until the early 2000s.

AI is likely following a similar pattern. The task-level improvements are real and measurable right now.

The economy-wide productivity transformation is real, but will take years — maybe a decade or more — to fully appear in the kind of data that economists and investors can confidently use to justify stock prices.

Future Steps: What Should Happen Next

For investors, the most important lesson from history is patience combined with diversification.

Rather than placing all bets on the companies building the underlying AI infrastructure — the chips, the data centers, the foundational models — experienced investors are beginning to look at companies that are effectively using AI within specific industries: healthcare companies using AI for drug discovery, financial firms using AI for fraud detection, logistics companies using AI for routing optimization.

For policymakers and governments, the AI investment landscape raises questions about energy supply, data governance, education, and competitive fairness.

The physical demands of AI data centers — electricity, water, land — are already creating planning challenges in multiple countries.

Governments that invest early in the infrastructure and workforce training needed to support AI adoption may benefit from faster productivity gains; those that delay may find the benefits arriving even later than economists currently project.

For ordinary people watching their pension funds and savings accounts — many of which now hold significant AI-related stocks through index funds — the key message is that volatility is normal and to be expected.

The value of AI stocks has already swung sharply in 2026 as markets react to new information about costs, competition, and deployment realities.

Those swings will likely continue for years. But the underlying technology is not going away.

Conclusion: The Fog Will Lift, But Not Yet

AI is genuinely transformative. The evidence for that is strong and growing.

Productivity at the task level is improving dramatically. Investment is pouring in from every direction.

The foundations of a new era in human economic productivity are being laid right now, in data centers around the world.

But markets price the future, and the future of AI is still genuinely unclear in all the ways that matter most to investors: who will win, how quickly, at what cost, and against what competitive landscape.

competitive landscape can change overnight.

The productivity data shows that macro-level transformation is slower than micro-level breakthroughs.

History shows that even truly revolutionary technologies can leave their early investors poorer while enriching those who invest later, at prices that reflect reality rather than hope.

The fog surrounding AI valuations is not a mistake or a failure. It is what a technological revolution looks like from the inside, in real time.

It has looked exactly like this before. And like before, the fog will eventually lift — probably just not as soon as everyone currently hopes.