US Lures Scorned Allies into Anti-China Minerals Trade Empire : Trump’s Project Vault Stockpile- Part I

Executive summary

Washington’s Secret Weapon: Critical Minerals Bloc Shakes Global Order

The Trump administration has turned critical minerals into the organizing principle of a new geopolitical club, using trade policy, industrial strategy, and security rhetoric to bind more than 50 partner countries into a preferential "minerals zone" designed to reduce reliance on China.

At the inaugural Critical Minerals Ministerial in Washington, Vice President J.D. Vance proposed a bloc that would coordinate tariffs and price floors for key raw materials, link access to financing with club membership, and build a US-centric supply network for technologies ranging from weapons systems to batteries and artificial intelligence hardware.

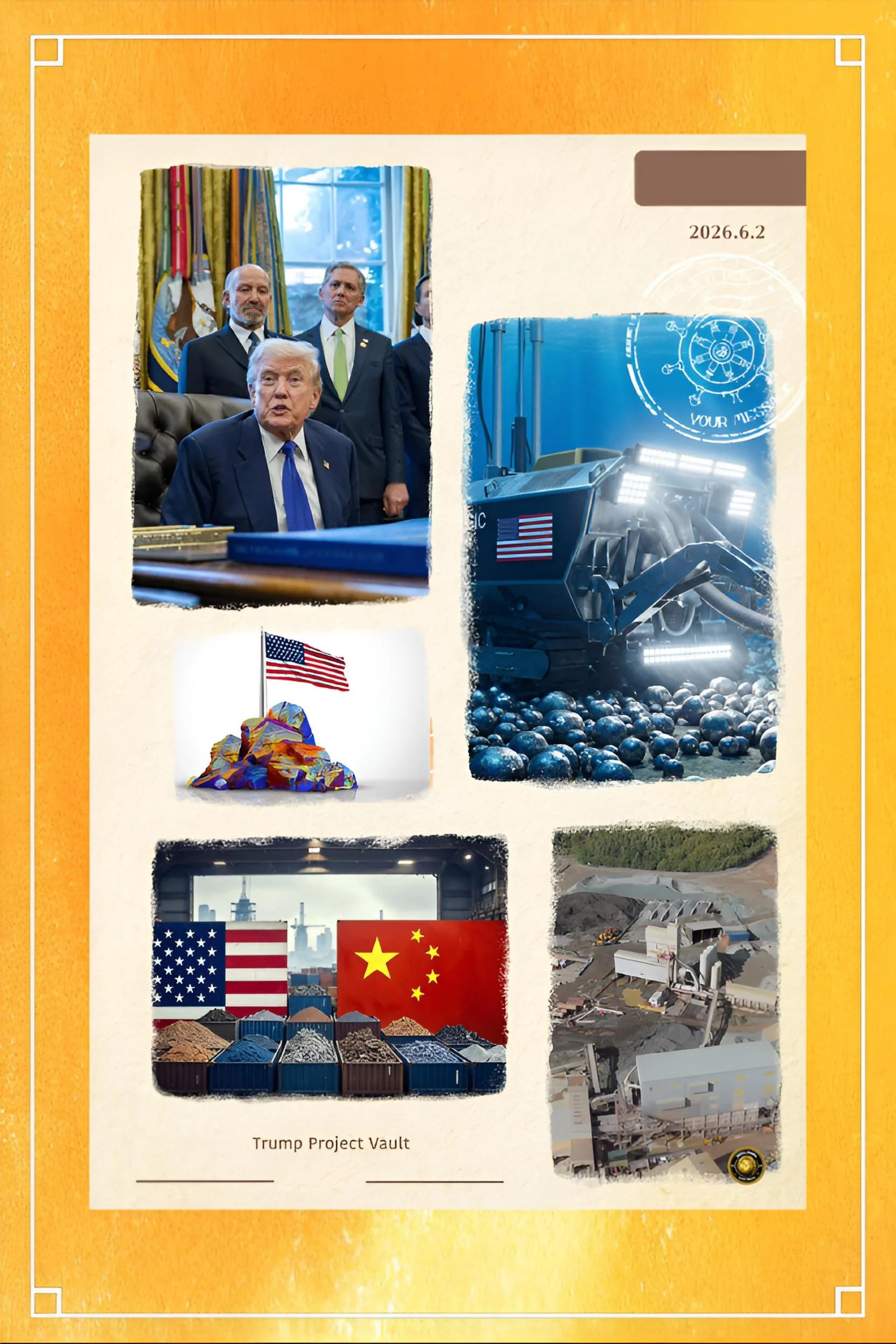

This effort is reinforced by Project Vault, a roughly $12 billion strategic stockpile primarily funded by a $10 billion Export-Import Bank loan and over $1.5 billion in private capital, as well as growing US equity stakes in mining and processing firms.

Behind the new "critical minerals club" lies a stark structural problem: China controls about 70% of global rare-earth mining and around 90% of processing capacity, and has repeatedly signaled its willingness to weaponize this leverage through export restrictions.

The proposed club represents both continuity and rupture: it builds on earlier initiatives such as the Mineral Security Partnership and EU–US critical raw materials dialogues, yet it is far more interventionist in its use of price floors, stockpiles, and equity stakes, and more explicitly bound up with Trump's broader "America First" tariffs and industrial nationalism.

This duality explains why the club has attracted enthusiastic participation from some partners that Washington has previously antagonized, even as many remain ambivalent about subordinating their own development strategies to a US-led scheme.

The initiative carries significant risks. Coordinated price floors and stockpiles could fragment the global minerals market into rival blocs, invite legal challenges, and incentivize cheating by both states and firms.

Producer countries in Africa and Latin America worry about repeating an extractive "resource curse" under new branding, especially when environmental and governance safeguards lag behind demand for investment.

Yet the structural urgency of decarbonization, digitalization, and defense rearmament means that some form of minerals coordination club is likely to persist, even if the exact shape of Trump's scheme evolves under domestic and international pressure over the next decade.

Introduction

Trump’s Minerals Revolution Recruits 50 Countries Against Beijing Grip

The term "critical minerals" refers to roughly 60 metals and minerals that governments deem essential to economic security and national defense, and whose supply is vulnerable to disruption.

These include rare earth elements used in permanent magnets, lithium and nickel for batteries, cobalt and manganese for high-performance alloys, and a range of inputs for chips, sensors, and precision-guided weapons.

Over the last two decades, the demand curve for these materials has steepened as electric vehicles, renewable energy systems, quantum computing, and artificial intelligence have moved from niche technologies into the backbone of industrial policy.

For Washington, the uncomfortable reality is that this green-digital-military convergence runs straight through supply chains dominated at multiple stages by China.

Beijing's earlier decision to invest massively in mining, processing, and midstream conversion has created an entrenched "mine-to-magnet" and "mine-to-battery" ecosystem that the United States and its allies now struggle to match.

A series of export controls, informal restrictions, and signaling from Beijing during trade tensions has reinforced fears in US policy circles that critical minerals are no longer merely commodities, but instruments of state power.

Trump's return to office has accelerated the securitization of this issue.

Where the previous administration sought mainly to de-risk supply chains via subsidies, permitting reform, and soft coordination clubs, the current White House is openly experimenting with a harder-edged toolkit: price floors enforced with tariffs, preferential trade zones conditioned on club membership, and large public equity stakes in private firms.

The Critical Minerals Ministerial and the proposed trade bloc are the most explicit expressions of this shift.

History and current status

The roots of today's critical minerals club predate Trump's second term.

During the 2010s, rare-earth export disputes between China and Japan, as well as supply scares over cobalt and lithium, sparked broader concern among OECD governments and defense planners.

The Biden administration responded by commissioning major supply chain reviews, launching the Mineral Security Partnership with like-minded allies, and embedding language on critical minerals into infrastructure and climate legislation.

These moves emphasized investment mobilization, standards, and modest stockpiling, but stopped short of pricing cartels or explicit trade blocs.

Trump's first term had already introduced a more confrontational tone, with escalating tariffs on Chinese goods and periodic threats to restrict the export of US technology inputs.

But the minerals agenda remained relatively underdeveloped, aside from episodic interest in Greenland's resources and rhetorical pledges to revive domestic mining.

The decisive turn came after China tightened its control over rare earth exports during the renewed US–China trade confrontation, causing production delays for automakers and defense contractors and exposing the thin resilience of Western supply chains.

In response, Trump's second-term administration has rolled out a sequenced set of initiatives.

First, it announced equity investments and grants in US and allied mining and processing firms, with the Pentagon spending nearly $5 billion over the last year to secure access to key materials.

Second, it unveiled Project Vault, a strategic stockpile valued at close to $12 billion, mainly financed through a $10 billion loan from the Export-Import Bank and over $1.5 billion in private capital, aimed at cushioning US manufacturers from future supply shocks.

Third, and most politically consequential, the State Department convened the Critical Minerals Ministerial in Washington, drawing officials from roughly 50–55 countries across Europe, Asia, Africa, and Latin America.

At this gathering, Vice President Vance formally pitched a preferential trade zone for critical minerals with coordinated price floors enforced through adjustable tariffs.

At the same time, Secretary of State Marco Rubio and other officials announced or previewed bilateral memoranda with partners, including Mexico, Japan, the European Union, and the United Kingdom.

Key developments

The signature development is the concept of a global "minerals club" in which members agree to: align tariff schedules and non-tariff measures for a defined list of critical minerals; respect everyday reference prices that operate as floors, below which imports would trigger compensating tariffs; and grant one another preferential access to export finance, stockpiles, and joint investment vehicles.

US officials frame this as a corrective to a "failing" international market in which state-subsidized Chinese producers can dump cheap material, undercutting competitors and deterring investment in alternative supply.

A second development is the integration of minerals policy with a broader turn toward state capitalism.

The White House has taken equity stakes in several mining and processing companies, extended similar arrangements to segments of the chip and defense supply chain, and tied loan guarantees to specific locations and offtake conditions.

Public officials openly argue that matching China's 30+ years of subsidies and industrial planning requires comparably activist measures, albeit within a nominally market-based framework.

Third, the club has rapidly acquired a global South dimension.

Resource-rich states such as Guinea, Nigeria, Argentina, and Brazil see the ministerial and proposed bloc as opportunities to extract financing, infrastructure, and political support, even as they maintain or expand ties with Beijing.

For some, engagement with the US club is a hedging strategy rather than an alignment choice; for others, it is a hard-nosed attempt to monetize their deposits while playing competing great powers against each other.

Latest facts and concerns

Recent reporting indicates that Washington has already concluded or is close to concluding more than 20 bilateral critical minerals agreements, with another tranche under negotiation following the ministerial.

The bloc's notional membership spans established industrial allies such as Japan, Germany, and South Korea; emerging processing hubs in Southeast Asia; and major mining jurisdictions in Africa and Latin America, including the Democratic Republic of Congo and key lithium producers.

Yet this apparent momentum sits atop considerable unease.

Economists warn that creating enforceable price floors across a club of heterogeneous producers and consumers risks both economic inefficiency and widespread evasion.

Firms and countries outside the club could free-ride by buying cut-price Chinese materials, blending them into supply chains, and selling finished products back into club markets, unless monitoring is highly intrusive.

Even within the bloc, companies will face strong incentives to arbitrage differences between posted reference prices and spot-market realities.

Producer-country advocates also fear that the minerals club could replicate features of historical commodity cartels while offering limited protection for labor, the environment, or local value-addition.

In regions such as the African Copperbelt or the Andean lithium triangle, communities are already grappling with water stress, governance deficits, and land conflicts; adding a geopolitical premium to demand could exacerbate these tensions if governance reforms lag behind capital inflows.

Finally, the initiative opens a new front with China.

Beijing has criticized the ministerial and trade bloc as an attempt to politicize supply chains and fragment markets, while signaling that it remains willing to use its control over intermediate processing to gain leverage in broader trade talks.

The risk of tit-for-tat export controls targeting complementary inputs—such as processing reagents, specialized equipment, or downstream components—adds another layer of uncertainty for global industry.

Cause-and-effect analysis

The minerals club can be understood as the product of interlocking causal chains operating at strategic, economic, and domestic political levels.

Strategically, the US–China rivalry over technology has elevated supply chain security from a technical concern to a central axis of great-power competition.

Washington's efforts to restrict Chinese access to advanced chips and manufacturing tools have been mirrored by Beijing's readiness to squeeze exports of inputs such as rare earths and battery materials.

This action–reaction cycle makes a coordinated response among US partners appear not merely desirable but necessary to US policymakers.

Economically, China's enduring cost advantages create a structural barrier to organic diversification. Even when Western or allied firms launch new mining and processing projects, they struggle to achieve bankable returns amid periodic Chinese price suppression.

This has led US officials and some industry actors to conclude that only a public–private architecture combining price floors, stockpiles, and long-term offtake agreements can provide the revenue-certainty needed to finance alternative supply at scale. In other words, the very market failures generated by decades of asymmetric state support have become the justification for Trump's more interventionist approach.

Domestically, Trump's political project of industrial nationalism reinforces this trajectory. The administration's willingness to break with traditional Republican skepticism toward state intervention—seen in equity stakes, targeted subsidies, and tariff-managed prices—reflects a fusion of economic populism with national security rhetoric.

The minerals club serves this agenda by offering both a narrative of regained sovereignty and a concrete tool to channel investment and jobs into favored constituencies.

For partners, the calculus is more ambivalent. Many have been targets of Trump's earlier tariff waves, rhetorical broadsides, or punitive diplomacy. Yet, they also face acute exposure to Chinese market power and a strong desire to access US capital and technology.

The result is a form of pragmatic bandwagoning: governments set aside resentments over past slights to explore club membership, while simultaneously hedging by continuing to engage with Beijing.

This dynamic vindicates the Foreign Policy framing of a club that brings in countries Washington has otherwise scorned.

Still, it also underscores how contingent and transactional much of this cooperation remains.

Future steps

In the near term, the minerals club will move from a rhetorical outline to a legal and institutional design.

Negotiators must clarify which materials are covered, how reference prices are determined, how tariffs are adjusted when market prices fall below those floors, and how exemptions are handled for strategic or humanitarian reasons.

Parallel technical working groups will likely focus on traceability systems, certification schemes to distinguish "club-compliant" material, and mechanisms to prevent blatant double-counting of stockpiled volumes.

Over the medium term, implementation will hinge on three hard constraints.

First, the geology and project pipeline: even with abundant financing, bringing new mines and processing plants online typically takes 10–15 years, given permitting, infrastructure, and community processes.

This means that any material diversification achieved during Trump's current term will be modest relative to China's entrenched base, and that expectations must be managed accordingly.

Second, domestic politics in both the US and partner states will shape the club's longevity.

A future US administration, more skeptical of tariffs or price management, might seek to dilute or repurpose the scheme.

At the same time, European and Asian partners face their own green transition constituencies, industrial lobbies, and fiscal constraints. Frictions over burden sharing, environmental standards, and local content rules are virtually guaranteed.

Third, China's counter-strategy will evolve. Beijing can respond by deepening its own web of long-term offtake contracts, accelerating Belt and Road investments in mining regions, innovating in material substitution and recycling, and selectively weaponizing export controls for maximum political effect.

The resulting equilibrium may resemble a competitive duopoly of overlapping, imperfectly enforced mineral spheres rather than a clean triumph of one model over the other.

Conclusion

Hot New US Minerals Alliance Challenges China’s Resource Monopoly

Trump's "hot new critical minerals club" is less a curiosity of Washington fashion than a signpost of a structural shift.

It crystallizes the fusion of climate, technology, and security agendas into a single supply-chain contest. It shows how far the United States is now prepared to go in contesting China's resource dominance.

The ministerial, Project Vault, and the proposed trade bloc together constitute an experiment in managed globalization for a narrow but strategically vital set of commodities, with Washington attempting to set the rules for a semi-closed economic space.

Whether this experiment succeeds will depend not only on US resolve but also on the agency of the many partners who have flocked to the ministerial despite prior grievances with Trump's approach.

Their willingness to accept price discipline, environmental safeguards, and political conditionality will determine whether the club becomes a durable institution or a short-lived bargaining chip.

At the same time, communities in producer countries will judge the club by tangible outcomes: jobs, infrastructure, environmental protection, and a fairer share of value, rather than by high-level communiqués.

In that sense, the critical minerals club is both an arena and a test. It is an arena where great-power rivalry, industrial strategy, and green-transition imperatives collide.

Still, it is also a test of whether a more politicized, club-based order can deliver resilient supply without simply reproducing past patterns of extraction and dependency under a new flag.

The answer will emerge not in conference halls in Washington, but in the mines, refineries, and industrial districts that this new order seeks to reshape over the coming decade.